.jpg)

In W37 in the soybean landscape, some of the most relevant trends included:

- The US is being effectively shut out of the Chinese market during its peak export season, with South American suppliers fulfilling nearly all of China's near-term demand. This has led to forecasts of significantly higher domestic ending stocks and has kept US soybean prices suppressed, even as global stockpiles are projected to tighten.

- China is actively diversifying its soybean procurement by increasing purchases from Argentina and Uruguay, a strategic move to reduce its dependency on any single supplier. This has provided a significant price boost for Argentina, which saw prices rise 2.44% WoW, while creating long-term market share risk for Brazil.

- Argentina is poised for a significant shift in its agricultural landscape, with farmers planning to reduce soybean acreage by up to 7% in favor of more profitable corn for the 2025/26 season. This projected decrease in future supply, combined with new Chinese demand, has created a bullish outlook for current Argentine soybean prices.

- Canadian soybean producers face a mixed outlook, with a major infrastructure expansion by ADM in Ontario boosting export capacity for the long term. However, the current 2025 Ontario crop forecast has been significantly reduced due to poor weather, while the Manitoba crop has proven resilient after navigating both pest and frost threats.

1. Weekly News

Global

USDA Lowers Global Soybean Stockpile Forecast Amid Shifting Trade Dynamics

The United States Department of Agriculture's (USDA) Sep-25 World Agricultural Supply and Demand Estimates (WASDE) report projects a tighter global soybean outlook for the 2025/26 season, forecasting reduced global ending stocks despite higher production in the United States (US). Global soybean ending stocks are lowered by 0.9 million metric tons (mmt) to 124.0 mmt, driven by lower beginning stocks and a 0.5 mmt reduction in the global production forecast to 425.9 mmt. This production decrease is primarily due to smaller anticipated harvests in India, the European Union (EU), and Serbia, which more than offset minor increases in Russia and the US. The report also highlights a shift in global trade dynamics. The forecast for global exports has been increased, with higher shipments expected from Argentina, Russia, and Canada. This contrasts with a 0.54 mmt (20 million bushels) reduction in the US export forecast, attributed to intensified competition from South America and reduced purchasing from China. Consequently, while the global picture is tightening, the US outlook shows higher ending stocks, projected to rise to 8.16 mmt (300 million bushels). This is a result of slightly higher US production of 117.0 mmt (4.3 billion bushels) combined with weaker export demand.

Argentina

Argentine Farmers to Reduce Soybean Acreage in Favor of Record Corn Crop

Argentine farmers are projected to significantly reduce their soybean planted area for the upcoming 2025/26 season, pivoting towards what is expected to be a record-breaking corn crop. The country's two leading grain exchanges have both forecast a decline in soybean acreage, citing low to negative profitability for the oilseed, which is prompting producers to favor more financially viable alternatives like corn and sunflowers. The Rosario Grains Exchange forecasts a 7% year-on-year (YoY) decline in soybean plantings to 16.4 million hectares (ha), which would yield a potential harvest of 47 mmt. The Buenos Aires Grain Exchange projects a more moderate, yet still significant, 4.3% drop in soybean area to 17.6 million ha. This strategic shift away from soybeans is occurring under a favorable weather outlook, with neutral conditions expected to support the development of other crops.

Brazil

Conab Confirms Record 2024/25 Brazilian Soybean Harvest and Raises Export Forecast

Brazil's national crop agency, Conab, has released its final report for the 2024/25 season, officially confirming a record soybean harvest of 171.47 mmt. This final figure represents a significant increase of 1.82 mmt compared to the agency's Aug-25 forecast. In line with the larger crop, Conab also raised its 2024/25 soybean export forecast to 106.65 mmt. The report highlighted Brazil's continued success in selling to China, capitalizing on the stalled trade negotiations between the US and its primary buyer. Notably, Conab also conducted a broad revision of historical data from the 2020/21 to 2024/25 seasons, resulting in a cumulative production increase of 13.12 mmt over the five-year period. Looking ahead, the agency confirmed that planting for the 2025/26 soybean crop has already commenced in Parana state. Initial forecasts from Safras & Mercado for this new season are highly optimistic, suggesting a potential harvest that could surpass 180 mmt, further cementing Brazil's position as the world's foremost soybean supplier.

China's Diversification to Argentina and Uruguay Poses Strategic Risk to Brazilian Soybean Dominance

China is strategically increasing its soybean purchases from Argentina and Uruguay, a move that directly challenges Brazil's long-held position as the primary supplier to the world's largest importer. While this diversification is partly driven by ongoing trade friction with the US, it also signals a broader strategy by Beijing to avoid over-reliance on any single source. This shift puts Brazil, which sends over 70% of its soybean exports to China in a trade relationship worth over USD 50 billion annually, on high alert. From Sep-24 to Jul-25, China imported 5 mmt of soybeans from Argentina and Uruguay, with initial estimates indicating that these purchases could increase to 10 mmt during the 2025/26 marketing year. The re-emergence of Argentina as a major supplier following its harvest recovery, combined with the rapid growth of Uruguay as an alternative source, provides China with greater negotiating leverage. For Brazil's agribusiness sector, this development poses significant risks, including a potential reduction in future sales contracts, downward pressure on prices, and a long-term erosion of its market share in a destination critical to its national trade balance. The move serves as a clear warning that no supplier is considered irreplaceable, compelling Brazil to reassess its market strategy and dependence on a single major buyer.

Canada

ADM Completes Major Expansion of Ontario Grain Terminal, Boosting Export Capacity

ADM Agri-Industries has completed a significant expansion of its grain terminal at Port Windsor, Ontario, a move designed to enhance export capabilities for agricultural products from southwestern Ontario. The USD 76 million project, which began in early 2024, includes substantial infrastructure upgrades such as new grain dryers, silos, conveyance systems, and specialized loading facilities for soybean and canola meal. This investment significantly increases the terminal's capacity to handle and export key commodities, including soybeans, canola, and corn. The expansion is poised to strengthen market access for regional farmers, improving the flow of agricultural goods to key destinations in Europe, the US, and Latin America. The project was supported by a USD 26.3 million investment from Transport Canada's National Trade Corridors Fund, highlighting a strategic public-private partnership aimed at bolstering Canada's agricultural logistics. This development strengthens a critical export hub, increases demand for locally grown products, and improves the overall competitiveness of the region's farmers in the global marketplace.

Ontario Soybean Crop Forecast Cut Amid Low Precipitation and High Temperatures

The outlook for Ontario's 2025 soybean crop has been downgraded due to adverse growing conditions, with production now estimated at 3.7 mmt, a notable decline from the 4.3 mmt harvested in 2024. Below-average precipitation and above-average temperatures across the main growing region in Aug-25 resulted in a significant yield loss. This domestic supply concern is unfolding against a backdrop of global market uncertainty dominated by the ongoing trade dispute between the US and China. While Ontario soybeans are competitively priced on the global market at USD 405/mt free on board (FOB), below both US and Brazilian offers, the lack of a trade resolution is suppressing the entire North American price complex. The market is in a holding pattern, as a potential US-China deal would likely lift prices, while a continued impasse would pressure them further. This uncertainty has prompted many Ontario farmers to pause sales, waiting for either a potential price rally or a clearer assessment of their own diminished harvest volumes.

Manitoba Soybean Crop Navigates Pest Pressure and Frost Scare

Manitoba's 2025 soybean crop has navigated a season of contrasting weather-related challenges, facing both pest pressure from heat and a subsequent frost scare. Earlier in the season, hot and dry conditions led to significant two-spotted spider mite infestations, particularly in the eastern and Interlake regions, which threatened yields during the critical R4 and R5 pod-filling stages. More recently, a widespread frost event in early Sep-25 brought below-freezing temperatures to many of the province's agricultural areas, raising new concerns about crop damage. However, the soybean crop appears to have largely dodged significant frost damage. According to provincial specialists, the frost was not severe or prolonged enough to cause major yield losses. This was primarily because most of the crop had already advanced to the more resilient R6 (full pod) and R7 (beginning maturity) growth stages. While the frost caused some leaf discoloration and raised minor concerns about green seed counts for grading, widespread damage was avoided. The crop has proven resilient, having now weathered both significant insect pressure and a late-season cold snap.

United States

US Soybean Exports Sidelined as China Secures South American Supply for Peak Season

US soybean producers are facing significant economic losses as the ongoing trade dispute with China effectively blocks them from their largest market midway through the peak export season. Chinese importers have already secured approximately 7.4 mmt of soybeans, primarily from South America, covering 95% of their projected demand for Oct-25 shipments. This stands in stark contrast to the previous year when China had booked 12 to 13 mmt of US soybeans for the September-to-November period, highlighting a dramatic shift in trade flows. Although US soybeans are currently priced lower than their Brazilian counterparts, a 23% retaliatory tariff imposed by China makes them economically unviable for Chinese buyers. Analysts project that if the trade standoff continues through mid-November, the total volume of lost US sales to China could reach between 14 and 16 mmt. The prolonged absence of Chinese demand is exerting considerable downward pressure on Chicago soybean futures and is expected to lead the USDA to revise its 2025/26 export forecast downward.

2. Weekly Pricing

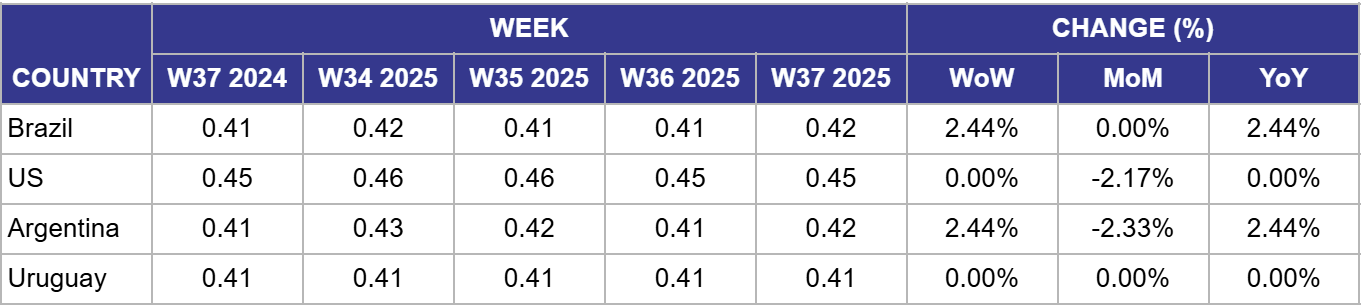

Weekly Soybean Pricing Important Exporters (USD/kg)

Yearly Change in Soybean Pricing Important Exporters (W37 2024 to W37 2025)

Brazil

In Brazil, the price of soybeans was USD 0.42/kg in W37, up 2.44% week-on-week (WoW) and YoY, while remaining stable month-on-month (MoM). The price increase WoW and YoY is supported by the final confirmation from Conab of a record 2024/25 harvest and an increased export forecast, especially to China, which solidifies the country's strong performance in the global market. Strong ongoing demand continues to provide a firm price floor. However, the flat MoM performance suggests the market is balancing this strength with emerging concerns. Recent reports that China is strategically increasing purchases from neighboring Argentina and Uruguay as part of a diversification strategy are creating a new headwind. This move by the world's largest buyer poses a long-term risk to Brazil's dominant market share and is likely tempering what could have been a stronger price rally.

United States

In the US, the price of soybeans was USD 0.45/kg in W37, stable WoW, but down 2.17% MoM and flat YoY. The WoW price stability suggests the market has found a temporary floor after recent declines, but this is occurring under significant bearish pressure. The market has now fully priced in the reality that China has covered 95% of its October demand from South America, effectively shutting the US out of its peak export season. The MoM decline reflects this harsh new reality, with reports confirming that potential lost sales could reach 16 mmt. The USDA's latest WASDE report corroborated this trend by raising US ending stock projections due to reduced export forecasts, confirming the challenge of a growing domestic stockpile with diminished international demand.

Argentina

In Argentina, the price of soybeans was USD 0.42/kg in W37, showing a strong increase of 2.44% WoW and YoY, though it remained down 2.33% MoM. The sharp WoW and YoY price increase is a direct result of significant positive news on the demand front. Reports confirmed that China is strategically increasing its soybean purchases from Argentina as part of a supplier diversification strategy, providing a lift to local prices. The lingering MoM decline is a remnant of previous weeks' weakness, but the current WoW spike signals a clear change in market sentiment. Furthermore, forecasts of a 4-7% reduction in soybean planted area for the 2025/26 season in favor of corn are adding a layer of supply-side support, suggesting a tighter domestic balance sheet ahead.

Uruguay

In Uruguay, the price of soybeans was USD 0.41/kg in W37, holding stable across WoW, MoM, and YoY comparisons. This stability reflects a market that has fully absorbed recent positive news without significant volatility. While reports confirmed that Uruguay, like Argentina, is a beneficiary of China's strategic diversification of suppliers, its market is much smaller, and the impact is more about long-term potential than an immediate price shock. The market appears to be in a state of equilibrium, supported by the prospect of increased Chinese demand but anchored by the large regional supply from Brazil and the broader global price environment. This stability suggests that while the long-term demand outlook has improved, current prices are considered balanced.

3. Actionable Recommendations

Adapt Marketing Strategies and Lobby for a Trade Resolution

For US producers and exporters, the structural shift in global trade requires a dual strategy. First, they must adapt to the new reality of a compressed export window by aggressively expanding into non-Chinese markets, leveraging recent agreements like the US-Japan trade deal to secure long-term contracts. At the same time, producers and their associations must intensify lobbying efforts, urging authorities to resolve the trade dispute with China swiftly. This political pressure is critical to prevent the current disruption from becoming a permanent realignment of global supply chains, which could lock the US out of its most significant market in the medium term, in favour of South American supplies. A proactive approach combining commercial diversification with political advocacy is essential to navigate current pressures and preserve long-term market access.

Capitalize on Chinese Demand While Mitigating Over-Reliance Risks

For South American producers and exporters, the current trade environment presents a historic opportunity to solidify their position in the Chinese market. They should capitalize on the absence of US competition by not only increasing sales volume but also by focusing on establishing strong, long-term supply relationships with Chinese buyers. However, it is crucial to avoid creating an over-reliance on this single market. The US-China trade situation could change rapidly, and the US has the capacity to return as a major supplier at any moment. Therefore, a balanced strategy is essential. While maximizing the current opportunity in China, South American exporters must concurrently pursue and develop other export destinations to ensure long-term stability and hedge against the risk of a sudden shift in global trade dynamics.

Sources: Tridge, Reuters, Manitoba Co-operator, Farmtario, UkrAgroConsult, The Poultry Site, USDA