W39 2025: Milk Weekly Update

In W39 in the milk landscape, some of the most relevant trends included:

- Global milk production is surging across key export regions like the EU, New Zealand, and the US, creating a significant supply glut that is outpacing current market demand. This widespread increase has fostered a bearish sentiment and is expected to exert sustained downward pressure on dairy commodity prices well into the next quarter.

- In Great Britain, record-high milk production is directly translating into a severe price correction, with wholesale commodity values slumping and processors announcing sharp cuts to farmgate prices. This downturn is driven by the domestic supply glut converging with a recovering European supply, leaving the market fundamentally imbalanced. In stark contrast, the UK organic milk sector continues to post double-digit YoY growth.

- A newly concluded trade agreement between the EU and Indonesia is set to create significant new export avenues for European dairy producers. The deal will remove tariffs on key products like milk powders and cheese, offering preferential access to a large and growing market of 285 million consumers.

1. Weekly News

Global

Global Milk Production Surge Outpaces Demand, Signaling Prolonged Price Pressure

A widespread increase in milk production across major exporting regions is creating a global supply surplus that current demand levels cannot absorb, pointing to a period of sustained downward pressure on prices. In the first seven months of the year, output from the top five exporters rose by approximately 1% year-on-year (YoY), adding an estimated 1.67 billion kilograms (kg) of additional milk to the global market. This production swell is broad-based, with the European Union (EU) now posting positive YoY growth, New Zealand starting its new season with a 4.25% increase in milk solids, and Argentina reporting a significant 11% rise in output through Aug-25. Analysts predict this supply growth will likely continue to build through the end of 2025 before a market correction is triggered by factors such as regulatory pressures in Europe or falling profitability leading to increased herd culling in other regions.

Europe

EU Milk Production Rises Amid Muted Demand and Price Premiums

Milk collections across the EU rose by 0.8% YoY in Jul-25, with a further increase of approximately 1.5% forecast for Aug-25, signaling a recovery in regional supply. According to a new market report from Ornua, this recovery contributes to an improved global supply outlook, with annual worldwide output now expected to expand by 1.5%, led by strong growth in the United States (US) and South America. However, this rising supply is meeting a market characterized by bearish sentiment and muted demand. With most European commodities trading at a significant premium to global levels, further price weakness is anticipated for Q4 2025 as a downward convergence of prices is expected. While EU cheese markets may find some stability, significant price firming is considered unlikely, reflecting a broader environment where increased milk flows are outpacing current trade and consumption levels.

European Dairy Sector Set to Benefit from New EU-Indonesia Trade Agreement

The conclusion of a Comprehensive Economic Partnership Agreement (CEPA) between the EU and Indonesia is poised to create significant new export opportunities for the European dairy industry. A central feature of the agreement is the removal of tariffs on a majority of EU agri-food exports to Indonesia, a growing market of 285 million consumers. The European Commission has explicitly identified dairy products, including milk powders, cheeses, and infant formula, as key categories that will gain preferential market access under the new terms. This development is expected to build upon the EU's existing agri-food exports to Indonesia, which were valued at approximately USD 1.2 billion (EUR 1 billion) last year. The agreement is structured to protect sensitive EU sectors while capitalizing on complementary trade, where Europe’s strength in high-value animal products, particularly dairy, aligns well with Indonesian import demand, promising a positive outcome for EU producers seeking new growth markets.

Netherlands

Nourish Ingredients Establishes Dutch Hub to Scale Animal-Free Fats for Dairy and Meat Alternatives

Australian food-tech company Nourish Ingredients has announced the establishment of a global commercial hub in Leiden, Netherlands, to scale up the development and commercialization of its precision-fermented animal-free fats. This strategic move is designed to integrate the company into Europe's advanced food innovation ecosystem, bringing it closer to global partners, a deep talent pool, and potential public funding for sustainable ingredients. Of particular relevance to the dairy industry is the company's Creamilux ingredient, a fat alternative developed for non-dairy applications. Nourish Ingredients is already collaborating with New Zealand dairy cooperative Fonterra to incorporate this technology into both plant-based and hybrid dairy products, demonstrating a clear pathway for innovation within the traditional sector. Using precision fermentation, the company creates lipids that replicate the functional and sensory properties of animal fats. The establishment of this European hub, set to be fully operational by 2026, signals a significant step towards commercializing these ingredients for the global market. This technology offers a complimentary pathway for dairy companies to innovate through hybrid products, potentially lowering costs and appealing to flexitarian consumers. Simultaneously, it represents a direct long-term threat, as scalable, high-performance fat alternatives could ultimately substitute traditional milk fat and erode demand for core dairy ingredients.

New Zealand

Record Aug-25 Milk Flow in New Zealand Driven by Favorable Farmer Margins

New Zealand's milk production continued its record-setting trend in Aug-25, with collections rising 2.5% YoY to nearly 127 million kilograms of milksolids (kgMS). This marks the fourth consecutive monthly record and brings production for the 2025/26 season to date to 4.2% ahead of the previous year, driven by strong pasture growth and affordable feed. This surge in output is underpinned by a highly profitable environment for farmers. Despite rising on-farm costs, major processors like Fonterra are forecasting farmgate milk prices around USD 6.10/kgMS (NZD 10.00/kgMS), well above the updated industry breakeven estimate of USD 5.28/kgMS (NZD 8.66/kgMS). The combination of high payout forecasts and reduced interest expenses is offsetting increases in other input costs, incentivizing producers to maximize output. This sustained production growth from a key global exporter is a significant factor contributing to the increasing supply on the world market, which is already facing absorption challenges.

United Kingdom

Forecast Shows Great Britain’s Milk Output Reaching New Peak Before Price Slump Signals Slowdown

A new forecast from the Agriculture and Horticulture Development Board (AHDB) for Great Britain projects that milk production will reach a record 12.89 billion litres for the 2025/26 season, an increase of 3.6% YoY. This continued momentum is primarily driven by increased yields per cow, as farmers have been incentivized to maximize output by a nearly 20-year high in the milk-to-feed price ratio and declining concentrate costs. However, the forecast indicates this production peak is temporary, with a slowdown anticipated in early 2026. The record volumes have begun to saturate the market, contributing to a significant slump in domestic butter and cheese commodity prices, which in turn is prompting processors to announce sharp cuts to farmgate milk prices. Looking ahead, falling farmer confidence is expected to combine with other pressures, such as a shrinking national milking herd and high costs for non-feed inputs like labor. Strong beef prices may also encourage increased culling over the winter, further constraining future production capacity and signaling a clear market transition from expansion to contraction.

Great Britain's Milk Market Braces for Sharp Price Drop Amid Record Production and Tumbling Commodity Values

The milk market in Great Britain is poised for a significant price correction as record-high domestic production converges with weakening global commodity markets. For the milk year to date, Great Britain’s production has surged to 5.53 billion litres, a decade high, running 217 million litres (5.2%) ahead of the previous year and 4.1% ahead of the 5-year average. This boom, fueled by a favorable milk-to-feed price ratio, has created a substantial surplus that the market is now struggling to absorb. While earlier in the year strong export demand and EU supply issues provided a temporary buffer, the situation has reversed. Key global producers, including the US and New Zealand, are now reporting increased milk volumes, while the EU market has stabilized, contributing to a global supply build-up. This shift has exposed a significant price premium for European dairy products, leading to a sharp downturn in United Kingdom (UK) wholesale prices for butter and cheese in Sep-25. Consequently, market indicators have plummeted, and processors have begun announcing severe cuts to farmgate milk prices for Nov-25, signaling a period of tightening margins for producers.

United Kingdom’s Milk Flow Continues Strong YoY Growth, Reinforcing Supply Pressure

Milk production in Great Britain continues to exhibit strong YoY growth, with daily deliveries for the week ending September 27 running 5.6% higher than the same period in 2024. According to the latest data from the AHDB, deliveries also posted a 1.0% increase week-on-week (WoW), confirming that production volumes remain robust as the autumn season advances. This sustained high output builds upon a trend of consistent growth, with the latest estimates for Aug-25 showing UK production at 1,263 million litres. The persistent and significant increase in milk flow adds further weight to the domestic supply glut. This oversupply is a key factor contributing to the build-up of dairy stocks and is directly translating into the severe downward pressure currently being observed on UK wholesale commodity and farmgate milk prices.

Great Britain’s Organic Milk Sector Maintains Impressive Double-Digit YoY Growth

Great Britain's organic milk sector continues to display exceptional growth, with daily deliveries for the week ending September 27 running 12.4% above the levels recorded in the same week last year. This strong YoY performance is further underscored by a 2.6% increase in volumes compared to the previous week, indicating robust and accelerating production. According to data from the AHDB, this weekly trend is consistent with the financial year to date (since Apr-25), which has seen a remarkable 12.2% expansion in organic milk volumes. The sustained and substantial growth in the organic milk pool points to resilient consumer demand, setting it apart from the oversupplied conventional market. This dynamic confirms the sector remains largely insulated from the price pressures affecting standard milk, presenting a clear growth avenue for processors seeking to capitalize on a reliable supply of high-value raw material.

2. Weekly Pricing

Weekly Powdered Milk Pricing Important Exporters (USD/kg)

* Varieties: Skim Milk Powder (SMP)

Yearly Change in Powdered Milk Pricing Important Exporters (W39 2024 to W39 2025)

* Varieties: SMP

* Blank spaces on the graph signify data unavailability stemming from factors like missing data, supply unavailability, or seasonality

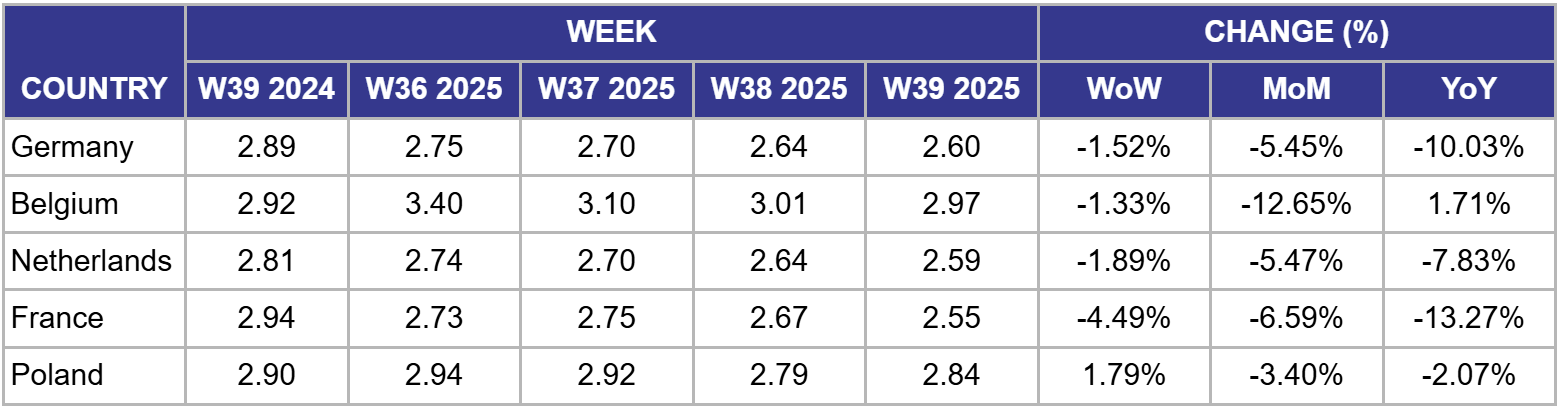

Germany

In Germany, the price of Skimmed Milk Powder (SMP) was USD 2.60/kg in W39, down 1.52% WoW, 5.45% month-on-month (MoM), and 10.03% YoY. The German market, a key European export hub, continues its steep descent under the weight of overwhelming bearish factors. The sustained price drop across all timeframes is a direct reflection of the market fundamentals highlighted this week, including the ongoing recovery in EU milk collections and a global supply glut. With European commodities trading at a premium to world markets, this downward trend signals an ongoing price correction. The deepening YoY decline to over 10% underscores the severity of the current oversupply situation and the impact of muted global demand on German exporters, who remain highly exposed to the weak international sentiment.

Belgium

In Belgium, the price of SMP was USD 2.97/kg in W39, declining 1.33% WoW and a substantial 12.65% MoM, which has nearly erased the YoY gain, now at just 1.71%. The Belgian market is undergoing a rapid and severe price correction, as evidenced by the dramatic MoM drop. This acceleration confirms that the premium for Belgian SMP is eroding quickly as it is forced to realign with lower prices across the continent. The market is being dictated by the broader European supply glut and the urgent need for regional prices to converge with weaker global benchmarks. Any supportive local factors are being completely overshadowed by the powerful bearish sentiment stemming from high milk flows and subdued demand across the EU.

Netherlands

In the Netherlands, the price of SMP was USD 2.59/kg in W39, falling 1.89% WoW, 5.47% MoM, and 7.83% YoY. The Dutch market continues to track the broader negative trend affecting Northwestern Europe, with prices remaining under significant pressure. The decline across all measured periods is a clear result of the structural oversupply dominating the continent, as confirmed by reports of recovering EU milk production and a bearish market outlook. The consistent price weakness demonstrates that strong regional milk flows and muted buyer interest are the primary forces driving the market. The negative WoW, MoM, and YoY figures all point towards a market that is fundamentally oversupplied, with little prospect of short-term price support.

France

In France, the price of SMP was USD 2.55/kg in W39, experiencing a sharp 4.49% drop WoW, which contributed to a 6.59% fall MoM and deepened the YoY decline to 13.27%. The French market saw one of the most significant weekly price drops, highlighting its role in the current market imbalance. This weakness is directly linked to news that France was a key contributor to the EU's milk supply recovery in the second quarter, meaning higher domestic production is amplifying the continental glut. The severe WoW fall and the substantial YoY deficit of over 13% illustrate how dramatically the market has shifted. The price is being driven squarely by the bearish fundamentals of oversupply and weak demand that are prevalent across Europe.

Poland

In Poland, the price of SMP was USD 2.84/kg in W39, showing a surprising 1.79% rebound WoW, though it remained down 3.40% MoM and 2.07% YoY. After a major downward reversal last week, the Polish market registered a minor WoW bounce. This uptick is likely a temporary technical correction or a reaction to short-term local demand rather than a change in the fundamental outlook. The negative MoM and YoY figures confirm that the broader bearish trend remains firmly in place. As a contributor to the EU's recovering milk supply, Poland is still fully exposed to the pressures of continental oversupply, weak demand, and the need for prices to align with lower global benchmarks, making this small gain appear fragile.

3. Actionable Recommendations

Producers Should Brace for Margin Compression and Re-evaluate Herd Strategy

The market signals for producers across all major producing and export regions are unequivocally bearish. The combination of record domestic milk flows and a deepening global supply glut is forcing a rapid and severe downward correction in farmgate prices, a trend that forecasts suggest will continue. Dairy farmers must prepare for a period of significant margin compression over the coming months by rigorously reviewing all operational costs. Now is the critical time to lock in favorable prices for inputs like feed where possible and to critically assess herd productivity. The strategic culling of less productive animals should be considered. This action can simultaneously improve herd efficiency, manage cash flow, and contribute to a marginal reduction in surplus milk output in a saturated market, thereby helping to mitigate the worst financial impacts of the downturn.

Engage with Food-Tech to Develop Hybrid Products and Future-Proof Portfolios

The establishment of a European hub by Nourish Ingredients, a producer of precision-fermented dairy fats, is a market signal that cannot be ignored. The partnership between this innovator and dairy giant Fonterra demonstrates that this technology represents not only a competitive threat but also a vital collaborative opportunity. Dairy companies should proactively engage with the food-tech sector to explore the development of novel hybrid products that blend traditional dairy with these emerging ingredients. Such products are well-positioned to appeal to the growing flexitarian consumer base, enhance sustainability credentials, and create new revenue streams that are not directly tied to volatile commodity cycles. Investing in or partnering with food-tech innovators is a crucial long-term strategy to ensure product portfolios remain relevant and competitive in a rapidly evolving food landscape.

Sources: Tridge, AHDB, RNZ, Green Queen, Feed Strategy, Agriland, Dairy Herd