.jpg)

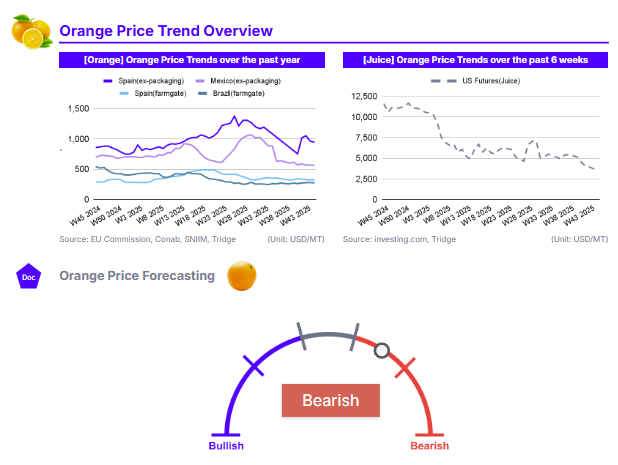

In W45 2025, the global orange market displayed a divergence between futures speculation and physical pricing. US Futures rose 4.26% WoW driven by concerns over heavy rains delaying the harvest in Mexico combined with good harvest expectations in the US. In contrast, physical prices softened across the board. Brazil fell 2.46% WoW to USD 273.3/mt, and Spain dropped 0.31% WoW to USD 322.5/mt. Long-term trends show a major market correction, with US Futures (-66.66% YoY) and Brazilian prices (-49.61% YoY) collapsing due to substantial supply recovery in the Americas, including a positive outlook for the US California Navel season. Spain remains the bullish exception (up 10.15% YoY) due to a forecast 16-year low harvest. Given the supply delays in Mexico and abundant availability in Brazil, buyers are strongly advised to source from Brazil to leverage its competitive pricing and recovered volumes.

1. Weekly Price Overview

US Futures Rebound on Mexican Delays While Physical Prices in Brazil and Spain Soften

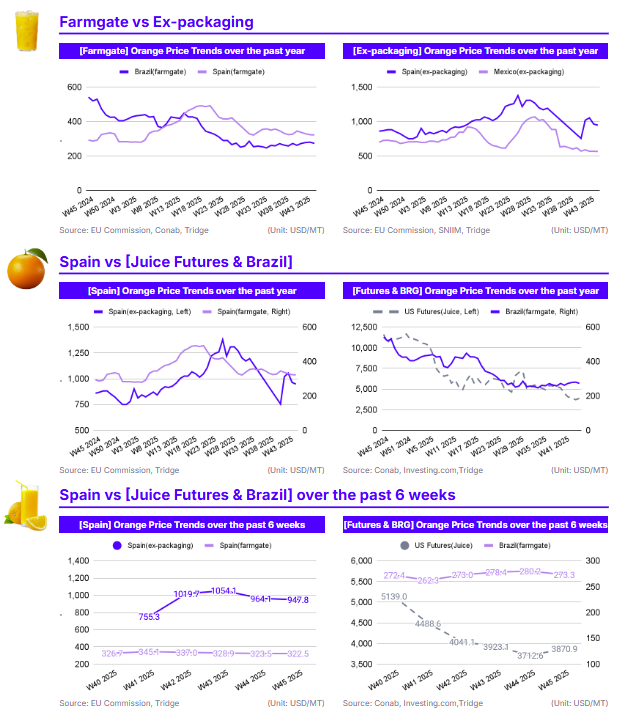

In Brazil, the farmgate price for oranges was USD 273.3/metric ton (mt) in W45, down 2.46% week-on-week (WoW). Mexico’s ex-packaging price saw a slight decline of 0.53% WoW to USD 565.5/mt. In Spain, both farmgate and ex-packaging prices declined, dropping 0.31% WoW to USD 322.5/mt and 1.69% WoW to USD 947.8/mt, respectively. Conversely, US Orange Juice Futures staged a recovery, rising 4.26% WoW to USD 3,870.9/mt.

The weekly trends highlight a disconnect between physical market availability and futures speculation. The rise in US Futures (+4.26%) is likely a reaction to supply delays in Mexico, a key supplier to the US market. Reports indicate that heavy rains have limited access to Mexican groves, causing a slow start to the 2025/26 harvest for early and mid-season fruit. In contrast, physical prices in Brazil (-2.46%) fell due to slower external demand and an ample supply of fruit for processing. Similarly, Spain’s prices softened as the market adjusts to higher harvest volumes as the season progresses while significant quantities of foreign fruit, particularly from South Africa, remain available in Europe.

2. Price Analysis

Prices in Americas Correct from 2024 Highs on Supply Recovery But Spain Bucks Trend with Supply Shortage

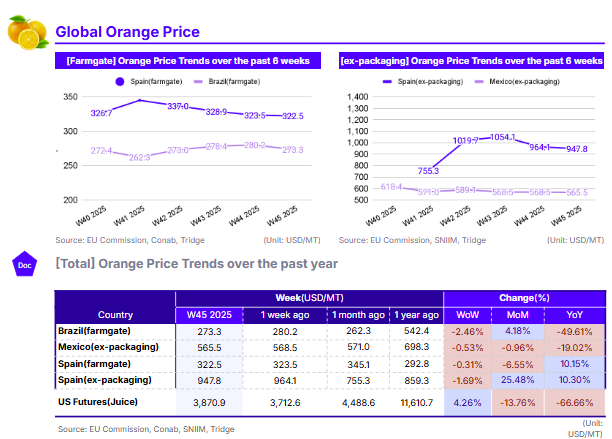

US Orange Juice Futures have plummeted 13.76% month-on-month (MoM) and 66.66% year-on-year (YoY) to USD 3,870.9/mt. Brazil’s farmgate price, despite a 4.18% MoM rise, remains down 49.61% YoY. Mexico follows this bearish long-term trend, dropping 19.02% YoY. Spain remains the outlier. Farmgate prices are up 10.15% YoY, and ex-packaging prices have surged 25.48% MoM and 10.30% YoY.

The massive YoY declines in the US (-66.66%) and Brazil (-49.61%) confirm a broad market correction driven by supply recovery in the Americas. A larger US harvest, particularly positive outlooks for the California Navel season, combined with a harvest recovery and increased processing availability in Brazil, has alleviated the extreme scarcity that drove 2024's high prices. In the US, the California Department of Food and Agriculture (CDFA) estimates that the “utilised” volume during the 2025/26 shipping season for navels should reach 80 million cartons (18 kg) compared to the 76.8 million of last year. The fruit quality is also expected to be high with large-sized fruit. This can largely be attributed to ideal weather conditions, especially the rain that fell during mid-October.

In contrast, Spain’s bullish performance reflects a shift to higher-priced new season fruit amid a severe shortage. According to the Ministry of Agriculture, Fisheries, and Food, Spain’s 2025/26 citrus harvest is expected to weigh in at 5.44 million metric tons (mmt), 10.7% lower than last year and 14.2% down on the five-year average. This is expected to be the lowest harvest volume in 16 years and can largely be attributed to adverse weather conditions. Oranges, which make up around half of the total citrus crop, are expected to reach 2.72 mmt, 11.6% or 356,300 mt less than in 2024/25. This situation is structurally insulating Spanish prices from the global bearish trend.

3. Strategic Recommendations

Leverage Brazilian Cost Advantage as Weather Disrupts Mexican Supply

Global buyers, particularly those in the Americas, should prioritize sourcing from Brazil to capitalize on its structural price advantage and stable availability. In W45, Brazil’s farmgate price of USD 273.3/mt remains a highly competitive option globally, trading at a significant discount compared to Mexico (USD 565.5/mt) and Spain (USD 322.5/mt). While Mexican producers are facing a slow start to the 2025/26 harvest due to heavy rains limiting grove access, Brazil offers readily available volumes with prices down 49.61% YoY.

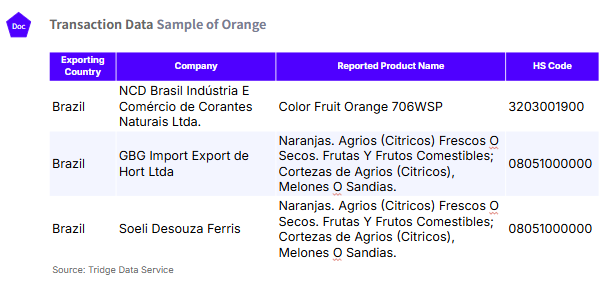

This sourcing shift is supported by strong supply fundamentals in Brazil. Recent reports indicate that domestic offer prices have decreased in recent weeks due to a greater supply of fruit for processing and slower external demand. This creates a favorable buyer's market, allowing importers to negotiate more aggressive terms. By shifting procurement to Brazil, buyers can mitigate the risks associated with the current logistical delays in Mexico and the structural shortages in Spain. Securing Brazilian contracts now ensures volume stability at a price point that reflects the broader market correction from 2024 highs. According to Tridge Eye data, suppliers worth considering in Brazil include NCD Brazil, GBG, and Soeli Desouza Ferris.