.jpg)

1. Weekly News

Global

FAO Raises 2024/25 Wheat Production Forecast but Lowers Trade Expectations

According to the October 4, 2024 forecast of the Food and Agriculture Organization of the United Nations (FAO), global wheat production for the 2024/25 season is slightly higher than the Sep-24 estimate, driven by expected increases in Australia. Production is projected to grow by 0.5% year-on-year (YoY) compared to the 2023/24 level. While the consumption forecast has also risen slightly since Sep-24, it remains 0.6% lower than the previous season due to reduced wheat use for feed and other purposes. Wheat trade for the 2024/25 period (July to June) is expected to decline compared to the earlier forecast, reflecting lower European Union (EU) export projections and reduced purchases by some importing nations. However, wheat stocks are anticipated to be higher than previously estimated at the end of 2025, with slight increases in Australia, the EU, and Ukraine contributing to this rise.

Algeria

Algeria Set to Boost Russian Wheat Imports Amid Diplomatic Tensions with France

Algeria's wheat purchases from Russia could reach 3 million metric tons (mmt) this 2024/25 season. This marks a notable shift in Algeria's wheat sourcing, as the country excluded French companies from the tender amid diplomatic tensions with France. Traditionally, France has been Algeria's largest wheat supplier, but the exclusion signals a growing reliance on Russian wheat. In the first quarter of the current export season (July to September), Algeria purchased 978 thousand mt of Russian wheat. This trade surge reflects the country's ambition to become a leading agricultural exporter, with the Russian President targeting a 50% increase in agricultural exports by 2030. One of the world's largest wheat importers, Algeria now ranks among the top five destinations for Russian wheat, alongside Egypt, Saudi Arabia, Iran, and Turkey. Algeria’s reliance on Russian wheat will deepen if the trend continues, further distancing it from French wheat supplies amid ongoing geopolitical tensions.

Australia

Australian Wheat Exports Decline in 2023/24 Amid Seasonal Trends

According to the Australian Bureau of Statistics (ABS), Australia's 2023/24 season wheat exports are projected at 19.5 mmt, revised down from an earlier estimate of 20 mmt. In Aug-24, Australia exported 1,21 mmt of wheat, including 2,844 mt of durum, reflecting an 18% month-on-month (MoM) decrease from Jul-24's 1.48 mmt. This reduction aligns with the typical seasonal decline, as the Australian shipping year ended on September 30. Containerized exports in August totaled 222,804 mt, with South Africa as the leading destination with 55 thousand mt, followed by Thailand with 35,272 mt, and Malaysia with 33,741 mt. The top markets for overall wheat exports in Aug-24 were the Philippines with 245,012 mt, Indonesia with 222,498 mt, and Yemen with 104,690 mt.

Russia

Russian Wheat Exports Declined Slightly in Sep-24

Russia exported 5.26 mmt of wheat in Sep-24, slightly down from 5.48 mmt during the same month in 2023. From Jul-24 to Sep-24, wheat exports reached 14.73 mmt, compared to 15 mmt in the same period last year. Despite this slight decline, exports to Egypt, Russia's largest wheat buyer, increased by 0.8 mmt, totaling nearly 2.9 mmt. This rise offset a 0.69 mmt drop in exports to Turkey, where imports were affected by a ban. However, wheat deliveries to Turkey continued via port warehouses and will likely resume post-October 15. Exports to Algeria remained steady at 0.98 mmt, while shipments to Bangladesh grew to 0.9 mmt. Saudi Arabia saw a reduction in imports to 0.5 mmt due to lower overall purchases by the General Authority for Food Security. Additionally, Russian wheat was exported to 62 countries in 2024, up from 58 last year.

2. Weekly Pricing

Weekly Wheat Pricing Important Exporters (USD/kg)

Yearly Change in Wheat Pricing Important Exporters (W41 2023 to W41 2024)

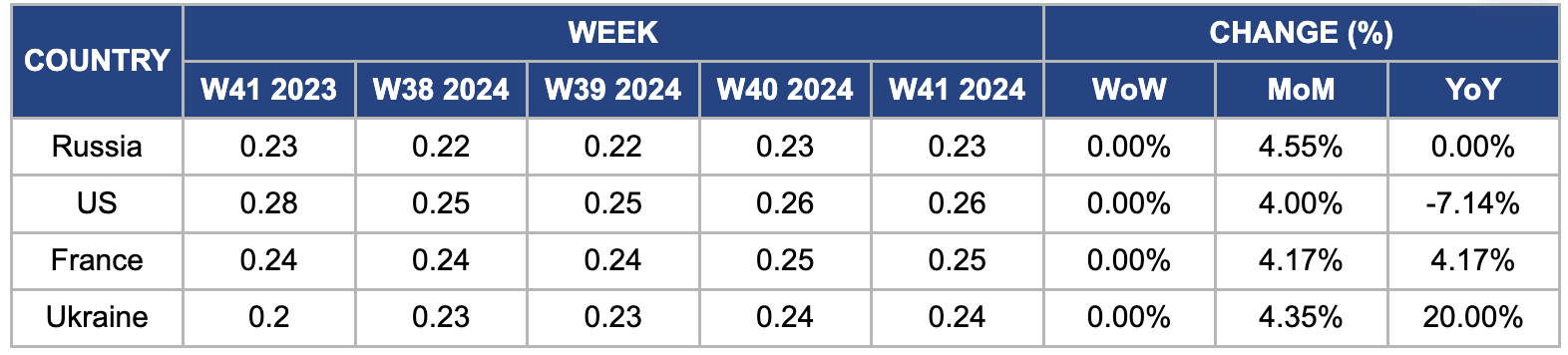

Russia

Russian wheat prices held steady at USD 0.23 per kilogram (kg) in W41. This stability comes despite a 4.55% MoM increase, driven by severe drought conditions impacting several regions, including Oryol, which has declared a state of emergency. These extreme weather events and earlier frosts have significantly impacted the 2024/25 wheat production forecast and created challenges for farmers regarding wheat sales, leading to reduced market liquidity. Concerns about winter planting for the 2025/26 crop have emerged, prompting calls for export restrictions from the Russian Grain Union, which urges the agriculture ministry to reassess the export quota methodology to align with global demand and seasonal potential.

United States

In W41, United States (US) wheat prices remained steady at USD 0.26/kg, reflecting a 4% MoM increase despite ongoing drought conditions affecting 50% of winter wheat areas. The United States Department of Agriculture (USDA) made minor adjustments to production forecasts, reducing estimates for soft red winter wheat while increasing those for other spring wheat varieties. However, prices are still down 7.14% YoY due to weak demand, stiff competition from Black Sea suppliers, and disappointing US export sales, which totaled only 168.90 thousand mt in W39, falling short of expectations. Despite improvements in winter wheat planting conditions, the Federal Reserve's interest rate cut has yet to lead to an ignited recovery in demand.

France

In W41, French wheat prices rose 4.17% MoM and YoY to USD 0.25/kg, reflecting the International Grains Council’s (IGC) revised global wheat production forecast for the 2024/25 season. This adjustment is due to poor harvest conditions in France, where heavy rainfall severely damages crops. Consequently, French soft wheat exports outside the EU have plummeted by 60% YoY to just 4.1 mmt, marking the lowest export levels in 23 seasons. This decline is pronounced particularly in exports to crucial markets such as Morocco, Algeria, and Tunisia, which have historically been critical destinations for French wheat.

Ukraine

In W41, Ukrainian FOB wheat prices remained stable week-on-week (WoW) but increased 4.35% MoM and 20% YoY, reaching USD 0.24/kg. This price rise is mainly due to concerns over drought conditions threatening winter wheat planting for the 2025 harvest. Compounded by the ongoing war, adverse weather has reduced the area sown with winter wheat to approximately 4.2 million hectares (ha) in 2024, down from 4.4 million ha last year. The anticipated smaller harvest and lower carryover stocks have further decreased the exportable surplus, contributing to the upward pressure on prices.

3. Actionable Recommendations

Diversify Supply Sources

Egypt should actively diversify its wheat sourcing to reduce dependence on traditional suppliers like France. This can be achieved by forging partnerships with emerging suppliers, mainly from Russia and Ukraine, which have been increasing their wheat production capacities. Egypt can enhance its negotiating power by establishing contracts with multiple suppliers, ensuring a more stable and resilient supply chain, especially in light of geopolitical tensions that may affect trade routes and pricing. Engaging in long-term contracts with Russian and Ukrainian exporters can help secure favorable pricing while mitigating the risks of price volatility associated with relying on a single source. Furthermore, exploring collaborations with countries with a surplus of wheat can open up new avenues for trade and reduce vulnerabilities in the face of global supply chain disruptions.

Targeted Marketing Campaigns

A comprehensive marketing strategy should be implemented to effectively promote the high quality and competitive pricing of Egyptian wheat, targeting emerging markets, particularly in Southeast Asia and Africa. This could involve collaborating with trade associations and agricultural bodies to organize promotional events highlighting Egyptian wheat's benefits, such as its quality and adaptability to various culinary uses. Participation in international trade fairs and food expos can increase visibility and facilitate direct connections with potential buyers and importers. Additionally, leveraging digital marketing tools, including social media platforms and online trade portals, can help reach a broader audience and create brand awareness for Egyptian wheat in new markets. By emphasizing Egyptian wheat's unique qualities and advantages, such as its suitability for diverse food applications, Egypt can stimulate demand and ultimately increase export volumes.

Invest in Infrastructure and Risk Management

Egypt should prioritize investments in transportation and storage infrastructure to enhance its export capabilities. Improving logistics networks, such as ports and road systems, will facilitate smoother and more efficient wheat exports, reducing delays and costs associated with transportation. Moreover, expanding storage facilities will help mitigate risks related to supply chain disruptions, allowing Egypt to maintain a buffer stock and respond promptly to market demands. Alongside infrastructure improvements, developing robust risk management strategies is essential to address the impacts of adverse weather on wheat production. Collaborating with agricultural experts to establish best practices for wheat cultivation can lead to higher yields and better crop resilience. Implementing advanced technologies, such as precision agriculture and data analytics for yield forecasting, will enhance market analysis capabilities, allowing Egyptian exporters to make informed decisions based on market trends and fluctuations. By investing in infrastructure and risk management, Egypt can ensure a more resilient and competitive position in the global wheat market.

Sources: Elevatorist, Zol, Vinanet, Interfax, NoticiasAgricolas, Chemanalyst