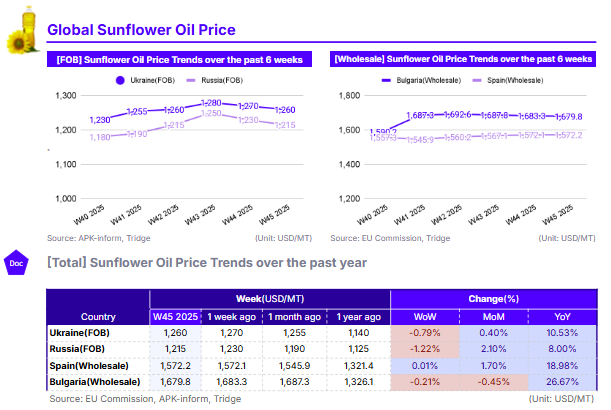

W45 2025: Sunflower Oil

In W45 of 2025, global sunflower oil prices in the Black Sea export prices eased, with Ukraine's FOB price at USD 1,260/mt, down 0.79% WoW, and Russia's FOB price falling 1.22% WoW to USD 1,215/mt. This dip was driven by pressure from cheaper competitor oils, particularly palm oil. In contrast, EU wholesale prices remained firm at elevated levels due to severe domestic supply shortages. Despite the weekly easing, the market remains structurally tight, with prices up significantly YoY across all regions—ranging from 8% in Russia to 26.67% in Bulgaria. This tightness is underpinned by a decade-low harvest in Ukraine and poor EU production, with the bloc's total harvest projected to be 8.86% below the five-year average. Consequently, the short-term outlook is mixed, as bullish supply fundamentals are being challenged by bearish pressure from cheaper substitute oils. Russia remains the most price-competitive sourcing option, but importers must navigate the high geopolitical and logistical risks involved.

1. Weekly Price Overview

Black Sea Prices Ease on Competitor Pressure, but EU Supply Remains Tight

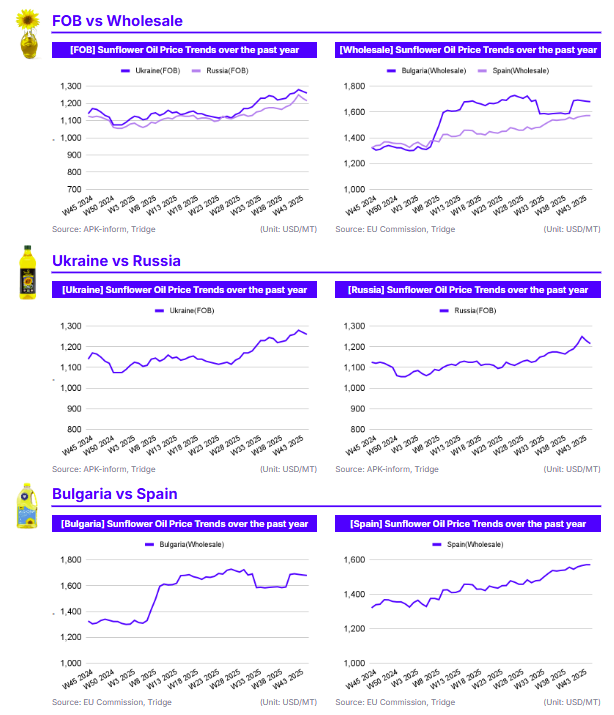

In W45 of 2025, sunflower oil prices showed a divergence between Black Sea and European Union (EU) markets. In the Black Sea, prices eased, with Ukraine's Free on Board (FOB) price at USD 1,260 per metric ton (mt), down 0.79% week-on-week (WoW), and Russia's FOB price down 1.22% WoW to USD 1,215/mt. In contrast, EU wholesale prices remained relatively stable. Spain saw a marginal 0.01% WoW increase to USD 1,572.2/mt, while Bulgaria experienced a slight 0.21% WoW dip to USD 1,679.8/mt.

The downward pressure in the Black Sea is a direct response to a significant drop in prices for competing palm oil, which has lowered the premium for sunflower oil and caused some buyers to pause purchases. This price easing comes despite mounting supply concerns in Ukraine, where the harvest is nearing completion with forecasts pointing to the lowest yield in a decade, potentially as low as 10.6 million metric tons (mmt). EU prices are being supported by their own severe domestic supply shortages. Bulgaria's price remains exceptionally high due to a poor harvest (down 11.73% from the 5-year average), while Spain's firm price is supported by an EU-wide production deficit, with the total EU sunflower seed harvest projected to be 8.86% below the five-year average.

2. Price Analysis

Annual Price Hikes Continue to Reflect Structural Deficits, Despite Minor Short-Term Easing

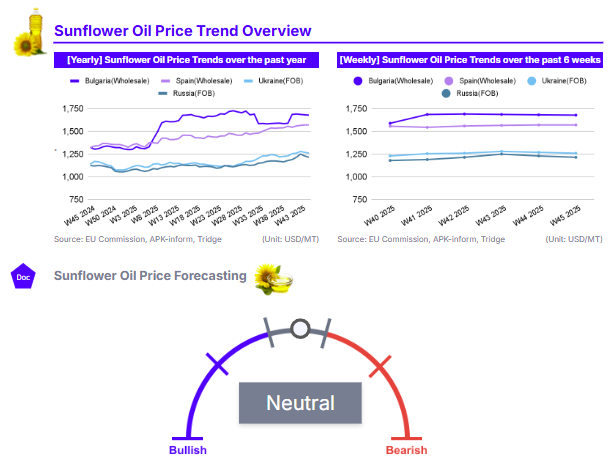

Analyzing the longer-term data for W45, sunflower oil prices show modest month-on-month (MoM) changes but significant year-on-year (YoY) gains, confirming a structurally tight market. Russia’s FOB price increased 2.10% MoM, and Spain’s wholesale price rose 1.70% MoM. Ukraine’s FOB price was nearly flat with a 0.40% MoM gain, while Bulgaria saw a slight 0.45% MoM dip. This relative monthly stability, even as Black Sea prices eased in the immediate week, reflects a market underpinned by tight supply, which was highlighted by the FAO Vegetable Oil Price Index rising in October on limited Black Sea and EU availability.

These monthly movements rest on top of substantial YoY increases across all analyzed regions. EU countries exhibited the largest upward movements, with Bulgarian wholesale prices up 26.67% YoY while prices in Spain increased 18.98% YoY. In the Black Sea, Ukrainian FOB prices are 10.53% higher YoY, and Russian prices are up 8.00% YoY. These strong annual gains are rooted in poor 2025 harvest results across Europe. Bulgaria’s significant 26.67% YoY jump is a clear result of its harvest shortfall, projected to be 11.73% below the five-year average due to drought and heavy rain. Similarly, Spain's 18.98% YoY increase is supported by a tight EU-wide supply and limited volumes from Ukraine. Ukraine’s 10.53% annual gain is driven by its harvest being the smallest in ten years. Russia’s 8% YoY increase, the most subdued of the group, is likely capped by its large harvest, which, while lower than expected, is helping to moderate price increases relative to its supply-strapped neighbors. The short-term outlook is mixed, with bullish supply-side fundamentals being challenged by bearish pressure from cheaper competitor oils.

3. Strategic Recommendations

Russia's Price-Competitive Sunflower Oil Remains a Good Opportunity but Requires Careful Risk Management

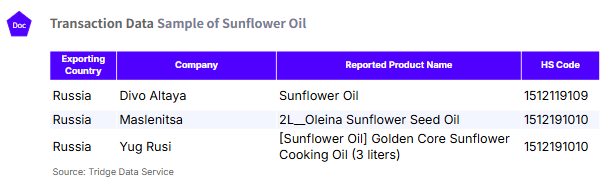

For global buyers seeking to mitigate the high prices seen in the European Union (EU) and the persistent supply uncertainty in Ukraine, Russia remains a key sourcing opportunity. In Week 45, Russia's Free on Board (FOB) price eased to USD 1,215 per metric ton (mt), reinforcing its position as the most competitive major exporter. This price stands significantly below Ukraine's (USD 1,260/mt) and especially EU wholesale levels in Bulgaria (USD 1,679.8/mt) and Spain (USD 1,572.2/mt). This price advantage is supported by strong supply fundamentals. While Ukraine faces its lowest harvest in a decade and Bulgaria suffers an acute raw material shortage, Russia's 2025 harvest, though slightly lower than initial expectations, remains large. This combination of the lowest price and ample volume availability makes it an attractive option for importers.

However, buyers must balance this opportunity with the significant geopolitical and logistical risks involved. Sourcing from a nation engaged in an active war carries inherent uncertainties, including potential disruptions to Black Sea port operations, high insurance premiums, and complex payment channels. Furthermore, the Russian government's active use of export duties to manage domestic prices represents a policy risk that could impact final costs. Therefore, importers considering Russia should conduct thorough due diligence on their logistics partners and secure comprehensive cargo insurance. This strategy is best suited for buyers who have a high-risk tolerance and can implement robust contingency plans to manage supply chain interruptions. Tridge Eyeʼs transaction level data highlights Divo Altaya, Maslenitsa, and Yug Rusi as viable export partners in Russia.