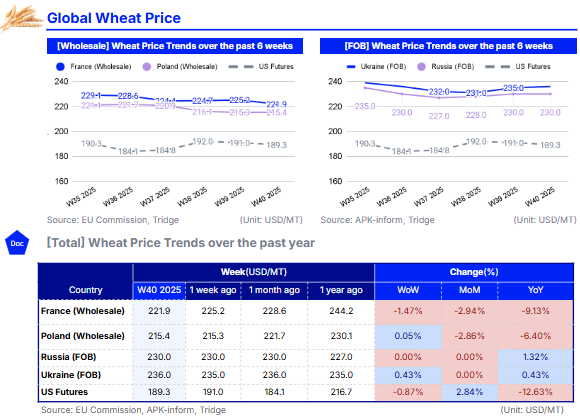

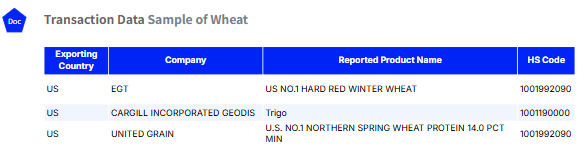

In W40, global wheat prices diverged, with US and French markets falling while the Black Sea held firm. US Futures (USD 189.3/mt) and French wholesale (USD 221.9/mt) prices declined due to bearish sentiment from ample global supplies. This is driven by a massive US harvest, the largest since 2016, which has pushed US prices down 12.63% year-on-year (YoY). Conversely, Black Sea prices remained stable to firm, with Russian (USD 230.0/mt) and Ukrainian (USD 236.0/mt) prices showing slight YoY gains. This resilience is supported by regional factors, including a federal emergency in Russia's Rostov region and tight near-term supply in Ukraine. Given this clear price advantage and the record-high yields in the US, buyers are advised to capitalize on the depressed US market to secure wheat at globally competitive prices. Key suppliers to consider include EGT, Cargill Incorporated Geodis, and United Grain.

1. Weekly Price Overview

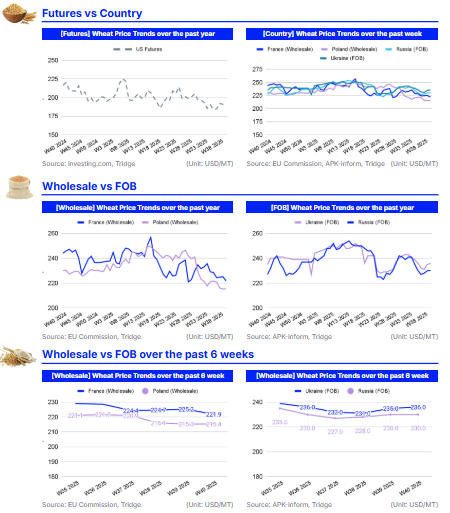

Black Sea Prices Diverge from West Amidst Global Supply Pressure

In W40, French and US wheat prices fell under the weight of ample supply, while Black Sea prices held firm due to regional factors. In France, the wholesale wheat price was USD 221.9/mt, a decline of 1.47% week-on-week (WoW). This decrease is directly linked to expectations of French wheat reserves hitting a 20-year high, caused by a slump in exports to key markets like Algeria and China. This supply glut is pushing domestic prices to five-year lows. Similarly, US Wheat Futures decreased by 0.87% WoW to USD 189.3/mt, reflecting a broader market sentiment weighed down by the Northern Hemisphere harvest concluding and positive outlooks for Southern Hemisphere producers.

In contrast, Black Sea markets showed resilience. Ukraine's Free on Board (FOB) price increased by 0.43% WoW to USD 236.0/mt. This strength is attributed to a combination of rising weekly exports and a tight immediate domestic supply, which is supporting prices against the global downward trend. Russian FOB prices remained unchanged at USD 230.0/mt, reflecting a market in equilibrium; a strong harvest is being balanced by regional crop loss concerns and a recent lowering of the national export forecast. Meanwhile, Poland’s price was nearly flat, rising just 0.05% WoW to USD 215.4/mt.

2. Price Analysis

Fundamental Split Deepens as Western Glut Contrasts with Black Sea Constraints

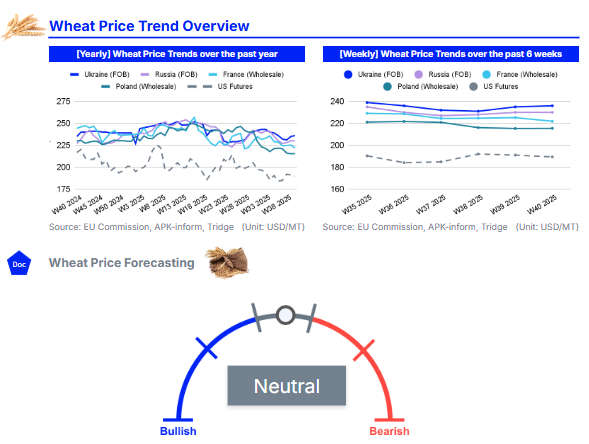

Longer-term price trends show a clear divergence, with Western markets under severe pressure while Black Sea prices remain firm. US Futures, at USD 189.3/mt, are down a significant 12.63% YoY, despite a recent 2.84% month-on-month (MoM) gain. This bearish YoY sentiment is mirrored in Europe, where French wholesale prices (USD 221.9/mt) fell 2.94% MoM and 9.13% YoY. Poland’s price of USD 215.4/mt followed a similar trajectory, declining 2.86% MoM and 6.40% YoY. In sharp contrast, Black Sea markets held their value. Russia's FOB price (USD 230.0/mt) was flat MoM but posted a 1.32% gain YoY. Ukraine's FOB price (USD 236.0/mt) was also stable MoM and edged up 0.43% YoY.

The pronounced YoY declines in France and the US are driven by a persistent global supply glut. France, in particular, is grappling with wheat reserves forecast to hit a 20-year high due to the structural loss of key export markets in Algeria and China, which has pushed prices to five-year lows. Conversely, the Black Sea's resilience is supported by strong fundamentals. Ukraine’s YoY increase is largely driven by decrease in its 2025 wheat production forecast to 21.8 mmt, down from 22.7 mmt in 2024. In Russia, despite a large national harvest of 87.2 mmt, prices are being supported by significant regional crop loss, with a federal emergency declared in the key Rostov region. This, combined with a recent downgrade of the near-term export forecast by SovEcon, has tightened the market and kept prices firm.

3. Strategic Recommendations

Capitalize on Record US Yields and Depressed Prices for Wheat Sourcing

Global wheat buyers should capitalize on the current significant price weakness in the US. As of W40, US futures are trading at levels markedly lower than European and Black Sea offers. This price advantage provides a stark contrast to the relative firmness seen in Russia and Ukraine, where prices are being supported by regional production issues and tight near-term supply.

This price depression in the US is fundamentally driven by a massive supply glut, which has been confirmed by the USDA’s latest projection. The 2025 US crop is estimated at 54 mmt, the largest national harvest since 2016. This immense supply is the result of a record-high average yield of 3.58 mt per hectare (ha) (53.3 bu/acre). This includes a particularly large hard red winter wheat outturn of approximately 21.9 mmt. This bearish supply situation in the US is the inverse of the Black Sea market dynamics. Therefore, importers currently reliant on other regions should see this as a key procurement opportunity. Securing US wheat contracts now allows buyers to lock in globally competitive prices. For buyers looking to source from the US, key suppliers include EGT, Cargill Incorporated Geodis, and United Grain based on transaction data from Tridge Eye.

4. Price Indicators