In W43, the global cheese market remained under pressure as strong milk production continued to exceed demand across key regions. In the EU, prices were steady in local terms but faced external downward pressure due to ample supply and limited export demand. Oceania saw downward trend, with record milk solids output in New Zealand sustaining strong supply levels, while the US market continued to grapple with high inventories and weak export competitiveness despite improving retail demand ahead of the holiday season. The October 21 GDT auction also reflected a soft market tone, driven by abundant milk output and subdued buying interest. On the demand side, China’s cheese imports increased in Sep-25, signaling growing consumer interest in value-added dairy products even amid broader market weakness. To adapt, processors are recommended to enhance export competitiveness, channel excess milk into higher-margin cheese and dairy categories, and expand into emerging markets in Asia and the Middle East to support global market balance.

1. Weekly Price Overview

Global Cheddar Prices Ease Due to Ample Supply and Seasonal Milk Surge

In W43, European Union (EU) cheddar prices averaged USD 5.09 per kilogram (kg), marking a 0.28% week-on-week (WoW) decline but a 13.37% year-on-year (YoY) increase. Despite the drop in USD terms, prices remained stable in local currency at EUR 4.38/kg, highlighting the influence of exchange rate fluctuations. The downward trend observed over the past month is largely attributed to ample supply outpacing demand across both domestic and export markets.

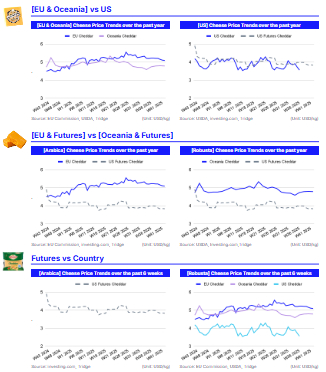

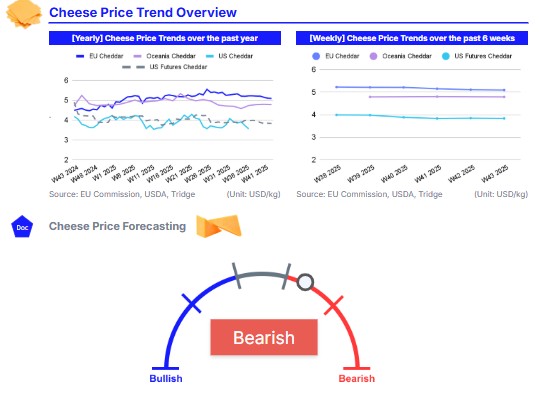

In Oceania, cheddar prices edged down 0.26% WoW to USD 4.79/kg, as the region enters peak milk production season. Milkfat availability remains high, with New Zealand recording its fifth consecutive month of record milk solids output, further contributing to downward price pressure.

Meanwhile, United States (US) cheddar futures averaged USD 3.883/kg, down 0.29% WoW and a significant 21.91% YoY decline. The US market continues to face elevated stock levels and weak spot competition, as processors prioritize clearing existing inventories over fresh procurement. Nonetheless, retail cheese demand is strengthening ahead of the holiday season, offering some support.

2. Price Analysis

Oceania’s Strong Milk Production Drives Down Global Dairy Trade Prices

In the Global Dairy Trade (GDT) auction held on October 21, the overall dairy price index declined by 1.4%, bringing the average winning price to USD 3,881 per metric ton (mt). Among the key products, cheddar prices fell by 1.9% to USD 4,758/mt, while mozzarella dropped by 5.3% to USD 3,230/mt. The decline reflects the impact of ample supply and seasonally high milk production, particularly from Oceania.

In New Zealand, milk production in Sep-25 reached 2.67 million metric tons (mmt), up 2.5% YoY, while milk solids output increased 3.4% YoY to 228.8 thousand mt, marking the fifth consecutive month of record-breaking production. For the 2025/26 season, cumulative milk output from Jun-25 to Sep-25 has grown 2.8% YoY, and milk solids are up 3.8% YoY, underscoring sustained supply strength. Similar trends of elevated milk production have also been observed in Argentina and Europe, contributing to the global supply pressure.

On the demand side, North Asia emerged as the leading buyer of cheddar during the GDT auction, followed by Southeast Asia/Oceania and the Middle East. Notably, China’s cheese imports rose 13.5% YoY in Sep-25, outperforming other dairy categories such as skimmed milk powder (SMP) and whole milk powder (WMP). This signals rising consumer interest in value-added dairy products, despite broader market weakness. In contrast, US cheese exports have become less competitive, as domestic prices remain elevated compared to other global suppliers.

3. Strategic Recommendations

Strategic Measures to Stabilize the Global Cheese Market During Supply Pressure

Given the current cheese market dynamics, EU processors, where prices remain stable in euro terms but under external downward pressure, should focus on enhancing export competitiveness through strategic exchange rate hedging and by expanding into price-sensitive emerging markets across Asia and the Middle East. In Oceania, where record milk solids and abundant supply continue to weigh on prices, processors can cushion further declines by channeling excess milk into higher-margin, value-added categories such as processed cheese, cream-based products, and long-shelf-life dairy powders. Meanwhile, US processors, contending with elevated inventories and weaker export competitiveness, should prioritize stock clearance through targeted retail promotions ahead of the holiday season, while pursuing strategic export partnerships in developing markets with growing demand for affordable dairy products.

On a global scale, exporters should leverage China’s strengthening demand for cheese and other value-added dairy products by adapting product profiles to local consumer preferences and building e-commerce and foodservice collaborations to sustain growth momentum. Simultaneously, producers across all regions are encouraged to invest in product innovation, operational efficiency, and market intelligence systems to anticipate demand fluctuations and manage price volatility more effectively.