1. Weekly News

South America

South America's Role Amidst Supply Challenges and Biofuel Demand

South America, particularly Argentina and Brazil, is pivotal in shaping the global soybean oil trade. Argentina has strengthened its position as the leading soybean oil and meal exporter, recovering from previous drought-induced disruptions. Meanwhile, Brazil, the largest soybean producer, focuses on energy transition and expanding biofuel policies, reducing soybean oil exports to meet domestic needs. Coupled with declining agricultural prices, this delayed planting due to warmer conditions and new regulations present challenges for the 2024/25 season. Despite these factors, the global demand for biofuels, particularly sustainable aviation fuel (SAF), intensifies competition for soybean oil feedstocks.

Bangladesh

Soybean Oil Shortage Disrupts Bangladesh Market, Leading to Price Hike and VAT Reduction

A major shortage of bottled soybean oil has disrupted Bangladesh's market as edible oil refining companies halted sales to dealers for a week, causing significant inconvenience to consumers. In response, a meeting was held with traders, resulting in a decision to reduce the value-added tax (VAT) on edible oil imports from 10% to 5% to increase supply. Following this, companies agreed to increase the availability of bottled soybean oil. Despite these efforts, many markets, including Shewrapara and Kathal Bagan, reported low soybean oil stocks. Prices of open soybean oil have risen by 11% over the past month, with the retail price at 1.42 to 1.44 per liter (L). The price rise reflects both domestic shortages and increased international edible oil prices.

Brazil

Brazilian Soybean Oil Exports Surge in Oct-24, Defying Seasonal Trends

Brazilian soybean oil exports rebounded in Oct-24, with shipments reaching 103.3 thousand metric tons (mt), according to the Ministry of Development, Industry, Commerce, and Services (MDIC). This marked a 16.4% increase from Sep-24’s 88.8 thousand mt and a 25% rise year-on-year (YoY) when exports totaled 82.5 thousand mt. This growth contrasts with the usual seasonal pattern, where exports typically peak in June and decline steadily until stabilizing in October. The recent uptick suggests a recovery in external demand following a slowdown in the previous two months.

Paraguay

Paraguay's Soybean Oil Exports Rise 6.5% YoY in Volume Despite Revenue Decline in 2024

From Jan-24 to Oct-24, Paraguay's soybean oil exports reached 464,000 mt, a 6.5% increase in volume compared to 2023. This generated USD 377.4 million in revenue—a 13.4% decline due to lower global oilseed prices. This aligns with broader trends in Paraguay's soybean sector, which achieved record exports of 7.7 million metric tons (mmt), up 35% YoY but with minimal revenue growth.

Argentina remained the primary buyer of Paraguayan soybeans, receiving 85% of shipments, followed by Brazil with nearly 10%. Other buyers included Russia, the United States (US), and several Asian and European nations. According to the Union of Production Guilds (UGP), the sector is expected to sustain positive momentum contingent on favorable weather and pricing conditions.

United States

Impact of Proposed Tariffs on US Soybean Farmers and Oilseed Processing Industry

US soybean farmers are concerned that proposed tariffs could limit access to China, the largest soybean buyer. However, these tariffs may also stimulate the construction of more domestic crushing plants, potentially boosting the soybean oil supply. Expansion of US crushing plants has slowed in recent years due to cheaper global feedstock imports. With tightening global vegetable oil supplies, US soybean oil futures recently surged. While tariffs benefit the domestic crushing industry, they may also reduce soybean exports and intensify competition. Rising construction costs and interest rates have delayed new processing plants, with some projects still under review. The outcome of these policy changes will significantly impact the US soybean market and oilseed processing industry.

2. Weekly Pricing

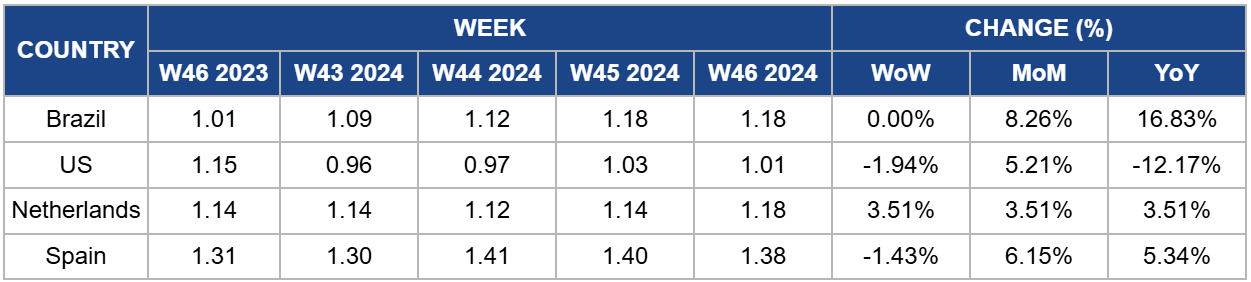

Weekly Soybean Oil Pricing Important Exporters (USD/kg)

Yearly Change in Soybean Oil Pricing Important Exporters (W46 2023 to W46 2024)

.png)

Brazil

Brazil's soybean oil prices remained steady at USD 1.18 per kilogram (kg) in W46, showing a notable month-on-month (MoM) increase of 8.26% and a 16.83% rise YoY. Despite this stability, the recent uptick in exports, which reached 103.3 thousand mt in Oct-24, signals a recovery in external demand after a seasonal slowdown. This rebound in exports, particularly following the usual decline in the months leading up to Oct-24, indicates stronger global interest in Brazilian soybean oil. The growth in both domestic prices and export volumes suggests a potential tightening of supply, which could lead to further price increases if the demand trend continues. Conversely, prices may stabilize or decline if export growth slows or global competition intensifies.

United States

US soybean oil prices decreased to USD 1.01/kg, marking a decrease of 1.94% week-on-week (WoW) following the appointment of a new Environmental Protection Agency (EPA) leader under the incoming administration. Plans to roll back climate regulations and prioritize US energy production raised concerns over reduced biofuel demand, exerting downward pressure on prices. Despite the decline, soybean oil prices remain 5.21% higher MoM, supported by reduced US soybean production forecasts.

Netherlands

In W46, soybean oil prices in the Netherlands rose to USD 1.18/kg, reflecting a 13.51% increase in both WoW and YoY from USD 1.14/kg. This price rise can be due to tightening global supply and recovering demand, particularly from export markets. Despite a recent slowdown in industry revenues, with significant drops in net income and tighter margins reported across the sector, the demand for agricultural commodities, including soybean oil, remains strong.

Spain

In W46, Spain's soybean oil prices fell to USD 1.38/kg, a 1.43% decrease from the previous week but reflecting a 6.15% increase MoM. While Spain faces challenges in expanding domestic soybean cultivation, particularly in regions like Castilla y León, its limited production capacity makes it reliant on imports. Low yields, agronomic issues, and competition from larger global producers have constrained soybean farming in Spain. Despite some local demand for non-Genetically Modified Organism (non-GMO) soybeans, the broader adoption of soybean farming in Spain remains uncertain, given its limited economic viability. This dynamic underscores the dependence on international markets for soybean oil supply, which may influence future price trends.

3. Actionable Recommendations

Diversify Soybean Oil Sourcing and Trade Routes

With increasing global competition for soybean oil, mainly driven by rising biofuel demand, businesses should diversify their sourcing strategies to secure stable supply chains. Importers should look to emerging soybean oil exporters such as Paraguay, Argentina, and Brazil while considering alternative feedstock sources. While Brazil's biofuel policies may limit soybean oil exports, Argentina and Paraguay, which have shown export growth, can provide more reliable options. Establishing partnerships with these countries and securing long-term contracts will help mitigate supply risks associated with changing domestic policies and environmental factors affecting production in major exporters.

Increase Domestic Soybean Oil Production Capacity

In response to the tightening global soybean oil supply and fluctuating international prices, businesses in the US and European Union (EU) should focus on enhancing domestic crushing capacity. Despite recent price declines in the US, expanding crushing plants can increase local soybean oil production and mitigate reliance on imports. With the US soybean oil futures surging, constructing new crushing plants or expanding existing facilities should be prioritized, even as global competition and rising construction costs pose challenges. Governments and businesses can work together to incentivize investment in processing infrastructure, ensuring better market access and price stability.

Monitor Policy Shifts and Adjust Pricing Strategies

Given the potential impact of shifting regulations on global biofuel policies and soybean oil production, it is essential for businesses to stay informed of policy changes, particularly in the US and Brazil. Companies should prepare for possible supply disruptions by adjusting their pricing strategies to reflect both regulatory changes and market demand fluctuations. For example, the US soybean oil market may face supply increases due to domestic crushing, while reduced Brazilian exports might limit supply, driving up prices. Implementing flexible pricing models and maintaining strong relationships with local and international suppliers will help companies better navigate the evolving market landscape.

Sources: Tridge, Grain Trade, Biodiesel BR, Bichos de Campo, Fast Markets, Prothom Alo, Reuters, Brownfields AG News, World Grain