In W45, global milk powder markets remained generally subdued. In the EU, both WMP and SMP showed modest declines, supported by steady production and contract-driven demand, with limited spot market activity. Oceania experienced softer prices for WMP and SMP amid strong milk flows and easing domestic and export markets. In South America, WMP prices rose slightly on stable demand, while SMP declined as producers prioritized WMP drying during the spring flush. The global dairy price trend reflected weaker prices across major commodities, where WMP declined and SMP remained stable. US milk powders faced strong competition from lower-priced New Zealand and European products, while traditional buyers reduced purchases and Southeast Asian markets remained oversupplied. To navigate these conditions, EU and Oceania producers should optimize production schedules and strengthen long-term contracts. South American producers should balance cream and skim outputs to maximize returns. Meanwhile, US stakeholders should focus on product differentiation, exploring alternative markets, and employing currency hedging strategies to protect market share and margins.

1. Weekly Price Overview

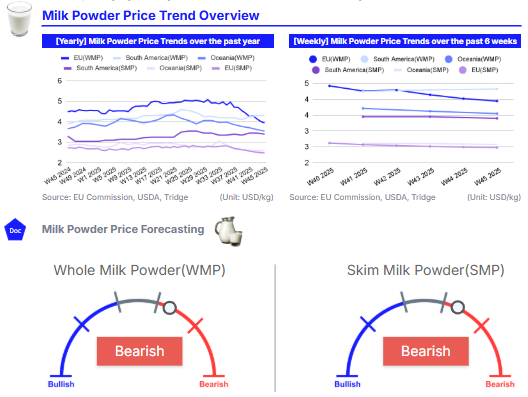

Milk Powder Markets Face Steady Demand but Bearish Pressure Across Regions

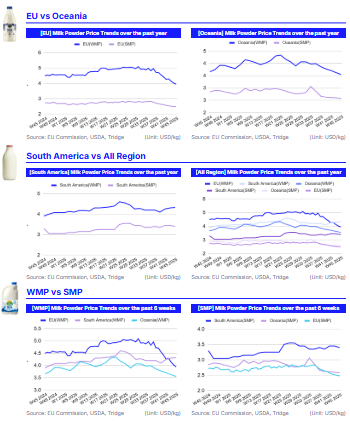

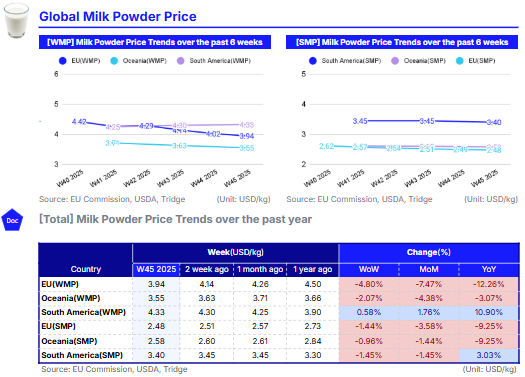

In W45, the European Union (EU) milk powder market remained subdued, with whole milk powder (WMP) averaging USD 3.94 per kilogram (kg), down 4.80% week-on-week (WoW), 7.47% month-on-month (MoM), and 12.26% year-on-year (YoY). Skim milk powder (SMP) stood at USD 2.48/kg, down 1.44% WoW, 3.58% MoM, and 9.25% YoY. The WMP market tone remained stable, supported by balanced production and adequate milk supplies. Demand was steady, with buyers largely maintaining scheduled contracts and limited spot activity. Similarly, the SMP market remained steady, with trading focused on contracted volumes and a cautious approach from buyers, while production schedules stayed consistent.

In Oceania, WMP prices averaged USD 3.55/kg, down 2.07% WoW, 4.38% MoM, and 3.07% YoY. Production remained active, supported by strong milk flows, while both domestic and export prices softened. SMP prices also eased slightly to USD 2.58/kg, down 0.96% WoW, 1.44% MoM, and 9.25% YoY, with production steady due to ample milk availability for drying.

In South America, WMP averaged USD 4.33/kg, rising 0.58% WoW, 1.76% MoM, and 10.90% YoY, reflecting steady demand despite full production schedules and abundant seasonal milk volumes. Conversely, SMP fell to USD 3.40/kg, down 1.45% WoW and MoM but up 3.03% YoY. With the spring flush underway, high milk volumes led producers to prioritize drying WMP over SMP due to concerns over excess cream.

2. Price Analysis

Global Milk Powder Prices Fall on Weak Demand and Strong Export Competition

According to the Food and Agriculture Organization (FAO), the global dairy price index averaged 142.2 points in Oct-25, a 3.42% MoM decline driven by lower prices across major dairy commodities. The WMP price index fell 5.98% MoM to 131.19 points, while the SMP index declined 3.96% MoM to 100.52 points, reflecting subdued demand and strong export competition.

This downward trend was mirrored at the Global Dairy Trade (GDT) auction on November 4, where WMP prices averaged USD 3,503 per metric ton (mt), a 2.7% drop compared to the previous event. SMP prices remained relatively stable at USD 2,559/mt. The primary buyers of WMP at the auction were North Asia, the Middle East, and Southeast Asia/Oceania. For SMP, North Asia was the largest purchaser, followed by Southeast Asia/Oceania and the Middle East.

In the EU, WMP inventories are considered manageable, with steady but quiet export interest, while SMP exports remain limited. In South America, strong WMP production exceeding demand is exerting downward pressure on prices. High farm-level milk output and elevated fat content are encouraging production to focus on WMP, which is constraining SMP availability in spot markets.

Meanwhile, United States (US) milk powders face growing competitive pressure. New Zealand’s WMP and European SMP are priced below US levels, capturing key export markets in Asia and Europe. Traditional buyers, including Mexico, are reducing purchases due to currency fluctuations and stronger domestic production, while Southeast Asian markets are already oversupplied, further limiting US market opportunities.

3. Strategic Recommendations

Optimize Production and Exports in the Global Milk Powder Market

Given the current dynamics across major milk powder markets, EU and Oceania companies should focus on optimizing production schedules to align output with contracted volumes. This will help limit excess spot market exposure that could depress prices further. Strengthening long-term supply contracts with key buyers in North Asia, the Middle East, and Southeast Asia/Oceania can provide predictable cash flow and reduce reliance on volatile spot markets.

In South America, where WMP production is strong but SMP is constrained, producers should consider diversifying processing priorities, balancing cream and skim outputs to maximize revenue from both products while carefully managing seasonal milk surges.

For the US market, which faces intense competition from New Zealand and European milk powders, stakeholders should implement price differentiation strategies. These can include emphasizing product quality or certifications such as organic, non-genetically modified organisms (GMO), or value-added blends, to defend market share in Asia and Europe. Additionally, exploring alternative export markets less impacted by oversupply, such as Africa or emerging Latin American regions, and employing currency hedging strategies can help mitigate exchange rate pressures affecting buyers like Mexico.