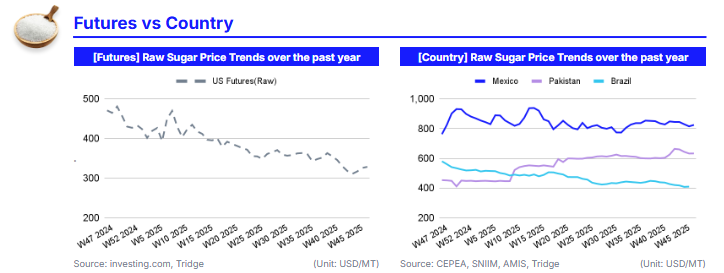

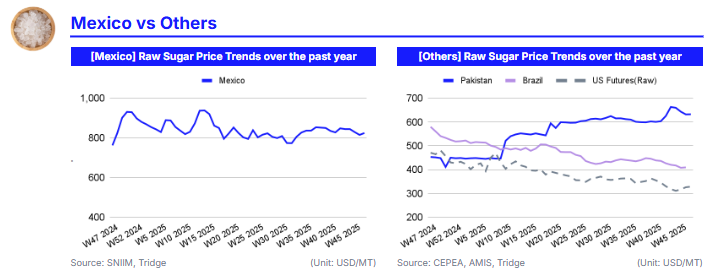

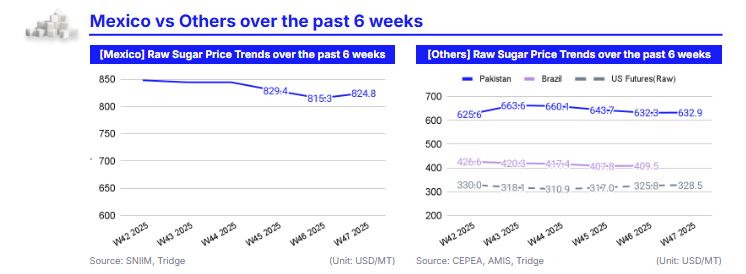

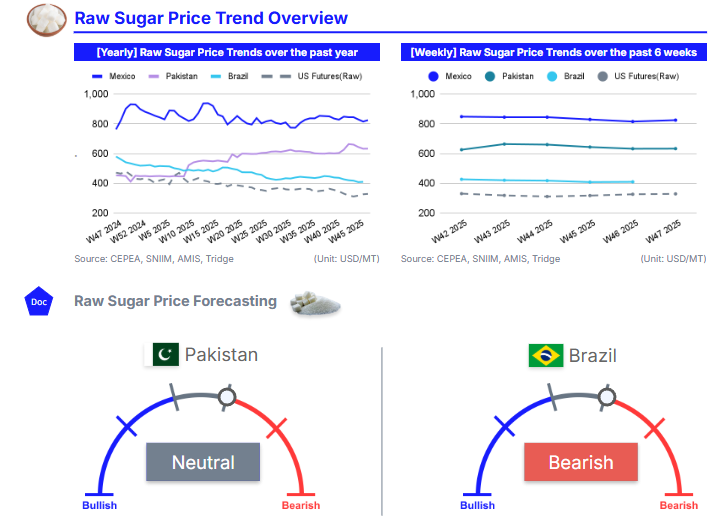

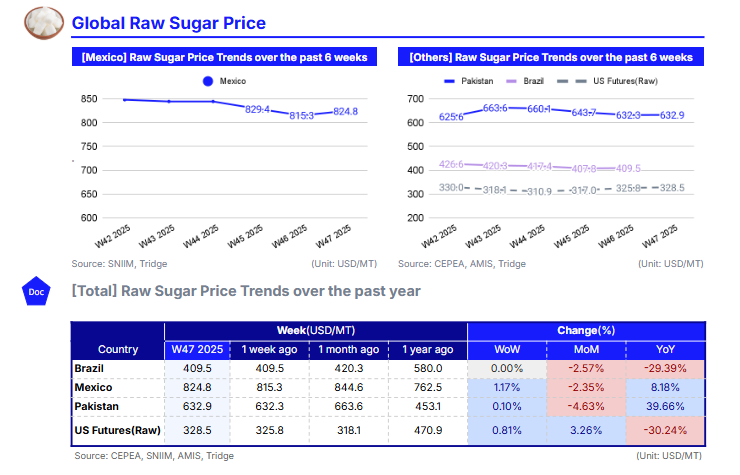

As of W47 2025, global sugar prices remained under bearish pressure as surplus expectations for 2025/26 intensified. Brazil’s sugar price held stable WoW at USD 409.5/mt but was down 29.39% YoY on heavy Centre-South output near 40.9 mmt. US raw sugar futures rose 0.81% WoW to USD 328.5/mt but remained sharply lower YoY, while Mexico’s prices increased 1.17% WoW to USD 824.8/mt on steep import tariffs. Pakistan’s prices edged up 0.10% WoW to USD 632.9/mt on forced early crushing, though deregulation plans continue to cap its structural upside.

For a global food manufacturer sourcing Brazilian sugar, the core strategy is to lock in forward Brazilian supply while prices remain compressed under the current surplus. Brazil offers the most cost-effective and stable origin into early 2026, while Mexico should remain a secondary, tariff-protected option for refined needs, and Pakistan a tactical, policy-driven market rather than a core sourcing origin.

1. Weekly Price Overview

Global Sugar Prices Stay Bearish as Brazil’s Heavy Output and Surplus Outlook Offset Mexico’s Tariff-Led Rally

In W47 2025, global sugar markets remained under broad bearish pressure, led by strong Brazilian output and surplus expectations for the 2025/26 season, although macro factors provided brief short-term support. Brazil’s sugar prices remained stable week-on-week (WoW) at USD 409.5 per metric ton (mt) but remained sharply lower by 29.39% year-on-year (YoY), reflecting heavy Centre-South production of 38.09 million metric tons (mmt) as of early Nov-25 and expectations of total output near 40.9 mmt. International futures hit multi-year lows, with the Mar-26 raw contract falling to 14.04 c/lb and the Dec-25 white contract to USD 406/mt, before a modest rebound driven by improved market sentiment following the end of the US government shutdown. Fundamentally, prices remain pressured by strong supply from Brazil (near 10 mmt), Thailand (30.95 mmt), and India, with 1.5 mmt of exports authorised, reinforcing consensus expectations of a surplus in 2025/26. In Mexico, sugar prices rose 1.17% WoW to USD 824.8/mt and were up 8.18% YoY after the government imposed steep import tariffs of up to 210.44% on liquid and refined sugars, sharply tightening import availability and pushing domestic prices higher. Pakistan’s sugar prices edged up 0.10% WoW to USD 632.9/mt as provincial authorities forced mills to begin crushing to ease supply tightness, while the federal government advanced plans for full sector deregulation, which could structurally lower prices over time through higher competition and exports. US raw sugar futures increased 0.81% WoW to USD 328.5/mt but were down 30.24% YoY, supported domestically by steep tariffs on Brazilian cane sugar and stable United States Department of Agriculture (USDA) stock estimates, even as weak global benchmarks and surplus production continued to cap upside across the broader market.

2. Price Analysis

Brazil Output Resilience and Rising Asian Supply Keep Global Sugar Prices Under Bearish Pressure

Brazil’s sugar prices declined 2.57% month-on-month (MoM) to USD 420.3/mt, extending the downward trend that has persisted since Oct-25 as global supply expectations continue to outweigh regional production setbacks. In São Paulo, sugarcane output for the 2025/26 harvest is projected to fall 5.2% YoY due to water stress and winter frosts, while average Total Recoverable Sugars (ATR) is estimated 3% lower at 134.9 kilograms (kg) per mt, and field productivity is down 5.4%. Despite these losses, a slightly larger harvested area and a sugar-heavy production mix have lifted state sugar output by 2.6% to 26.7 mmt. At the national level, Brazil’s cane crop is forecast at 666.4 mmt, only 1.6% lower YoY, while total sugar production is expected to rise 2% to 45mmt, with São Paulo contributing nearly 60% of the total. This resilience in output has kept physical availability high and limited any weather-driven price recovery.

The bearish price effect has been reinforced by record global supply prospects. India’s 2025/26 sugar production is projected at 30.95 mmt, supported by favorable monsoon rainfall and expanded planting, while Thailand’s output is estimated near 10 mmt under generally positive weather conditions. India has already authorized 1.5 mmt of exports for the new cycle, confirming steady international flows. Together with Brazil’s strong post-Jul-25 milling pace and accumulated production exceeding last year’s levels by the end of Sep-25, these volumes underpin market consensus for a surplus in 2025/26. This surplus environment drove international futures to multi-year lows, with the Mar-26 raw contract falling to 14.04 cents per pound (lb) and the Dec-25 white contract to USD 406/mt, before a short-lived rebound linked to macro sentiment following the end of the US government shutdown.

The near-term sugar price outlook remains bearish to neutral. While ethanol parity and lower oil prices could marginally adjust regional cane allocation, the accumulated sugar-heavy mix earlier in the season limits any meaningful shift in Brazil’s supply profile. With India and Thailand also entering the market with ample volumes, global trade flows are expected to remain well supplied into early 2026. A technical rebound in futures is possible on positioning or macro volatility, but absent a major weather disruption or a reduction in Indian export policy, prices are likely to remain capped and biased to the downside over the next two to three months.

3. Strategic Recommendations

Brazilian Oversupply Pushes Sugar to Multi-Year Lows, Reinforcing Forward Buying Strategy

Global sugar importers and food manufacturers should continue to lean decisively into Brazilian supply, as heavy Centre-South production near 40.9 mmt and confirmed surplus expectations for 2025/26 keep the global market structurally bearish. With Brazil’s domestic prices stable WoW at USD 409.5/mt but down nearly 29.4% YoY, and Mar-26 ICE raw futures recently testing multi-year lows near 14.04 c/lb, the current price environment remains highly favorable for forward procurement. Despite the brief macro-driven rebound linked to improved sentiment in the US, fundamentals remain dominated by strong output from Brazil, Thailand, and India, with 1.5 mmt of Indian exports reinforcing downside pressure into early 2026.

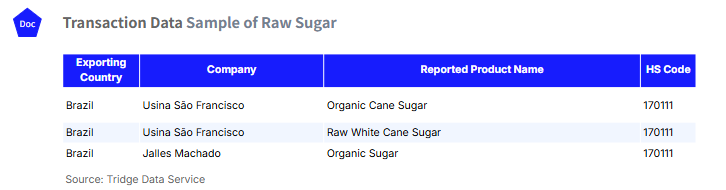

Importers in Asia, the Middle East, Europe, and North America should secure forward volumes of both conventional and organic sugar from Brazil while prices remain compressed. According to Tridge Eye’s transaction data, Usina São Francisco offers competitively priced Organic Cane Sugar and Raw White Cane Sugar with consistent export availability, while Jalles Machado remains a reliable supplier of Organic Sugar for premium and certified segments. Locking in multi-month supply agreements with these producers through Q2-2026 would hedge against freight volatility, port congestion at Santos and Paranaguá, and any late-season weather risks, while preserving cost advantages versus alternative origins. Mexico should remain a secondary, tariff-protected sourcing option only for buyers requiring refined product continuity, while Pakistan’s modest WoW gains remain policy-driven and tactical rather than structurally bullish.

From a trading and risk-management perspective, the market continues to favor a bearish-to-neutral posture. Traders should maintain short exposure via Mar–May 2026 ICE raw sugar futures or via bear put spreads, as surplus-driven fundamentals are likely to cap sustained rallies. However, industrial buyers should complement physical coverage with low-cost call spreads to protect against asymmetric upside risks tied to Indian weather, Thai crop revisions, or a shift in Brazil’s ethanol parity.