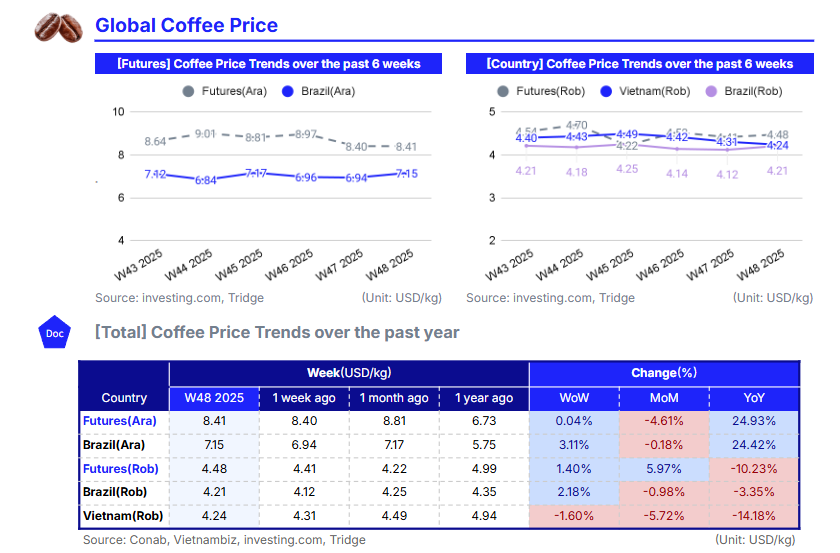

In W48 2025, global coffee markets began to stabilize as the removal of US tariffs on Brazilian coffee eased trade costs while weather uncertainty in Brazil and Vietnam continued to influence pricing. Arabica edged up to USD 8.41/kg, and Robusta moved to USD 4.48/kg, reflecting a modest recovery after earlier volatility. Minas Gerais weather issues kept Arabica supported, while excessive rainfall in Vietnam raised concerns over Robusta quality and disrupted harvesting. Brazilian domestic prices strengthened in both varieties, and Vietnam posted slight declines, signaling ongoing divergence between origins.

Global roasters sourcing Brazilian Arabica and Vietnamese Robusta should follow a two-speed strategy that builds controlled long exposure in Arabica while maintaining flexible, opportunistic purchasing in Robusta. Arabica positions for early 2026 benefit from structured hedging that captures upside linked to crop risk, while Robusta procurement should remain diversified between Vietnam and Brazil to manage weather disruptions and preserve blend consistency. This approach leverages Arabica’s firmer outlook while keeping Robusta purchasing adaptable in a more supply-sensitive environment.

1. Weekly Price Overview

Global Coffee Prices Recover as Tariff Suspension and Weather Volatility Reshape Market Sentiment

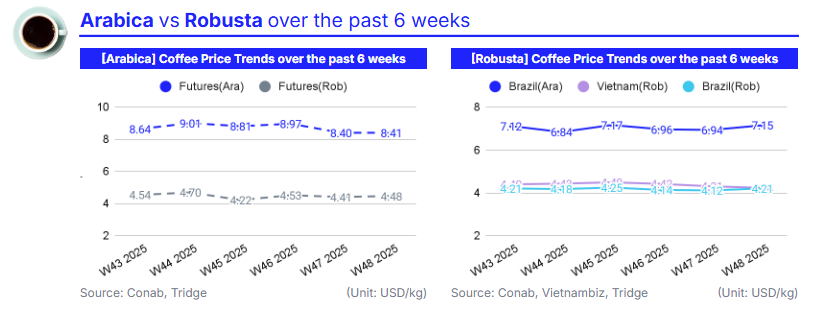

In W48 2025, global coffee prices entered a period of adjustment as markets responded to the removal of the United States (US) tariffs on Brazilian coffee and continued weather-driven uncertainty in Brazil and Vietnam. The international Arabica benchmark, represented by US Coffee C Futures, rose 0.04% week-on-week (WoW) to USD 8.41/kg, while Robusta, represented by London Coffee Futures, increased by 1.40% WoW to USD 4.48/kg, reflecting cautious recovery after sharp declines earlier in the month. The suspension of the additional 40% US tariff restored predictability to US–Brazil trade flows, reducing costs for US buyers and improving competitiveness for Brazilian exporters. However, the announcement initially triggered steep declines in New York and London futures before concerns over irregular rainfall in Brazil revived upward pressure. Weather instability in Minas Gerais continued to threaten the development of the 2026 crop, supporting firmer prices during the final sessions of Nov-25.

In Brazil, Arabica rose 3.11% WoW to USD 7.15/kg, and Robusta increased 2.18% WoW to USD 4.21/kg, mirroring movements on international exchanges. Physical markets were cautious, with producers delaying sales and buyers avoiding aggressive purchases amid volatility. In southern Minas Gerais, high-quality Arabica reached USD 432.68 per 60kg bag (BRL 2,340/60kg bag), marking an increase of 3.5% month-on-month (MoM), while Robusta type 7 in Vitória slipped 0.7% MoM to USD 255.17 per 60kg bag (BRL 1,380/60kg bag), highlighting regional divergence. Meanwhile, Vietnam’s Robusta prices declined 1.60% WoW to USD 4.24/kg as excessive rainfall and flooding disrupted harvesting and raised concerns about bean quality, adding further uncertainty to already tight global stocks. The combination of tariff removal, volatile weather in the two main producing countries, and continued stock scarcity kept market sentiment firm, with buyers closely monitoring climate conditions and trade normalization in Dec-25.

2. Price Analysis

Brazil–Vietnam Divergence Widens as Arabica Strengthens on Weather Risks While Robusta Faces Mixed Outlook

Analyzing recent data, Brazil’s coffee market shows a clear divergence between Arabica and Robusta that explains the contrasting year-on-year (YoY) price trends. Arabica surged 24.42% YoY to USD 8.41/kg as weather irregularities in Minas Gerais tightened expectations for the 2026 crop and global buyers remained willing to pay premiums for high-quality Brazilian beans. This supply-side uncertainty, combined with Brazil’s strong export performance, helped lift prices even as total shipments fell 20.3% YoY. Revenues rose 27.6% despite lower volumes, confirming that higher global valuations, not increased supply, were the primary driver of Brazil’s Arabica strength. However, Robusta dropped 3.35% YoY to USD 4.21/kg, reflecting more stable supply conditions and weaker export participation, as canephora represented just 10.5% of Brazil’s total shipments. The divergence also stems from consumer preference shifts. Arabica commanded nearly 80% of exports, reinforcing Brazil’s price leverage in the premium segment while limiting upside momentum in Robusta.

Vietnam’s market moved in the opposite direction, with Robusta prices down 14.18% YoY to USD 4.24/kg despite a recent short-term rebound driven by exchange-traded gains and domestic price increases. Heavy rains and flooding disrupted early-season harvesting, reducing bean quality and adding volatility, but the broader YoY decline reflects improved global availability compared to last year’s historically tight supply. Even so, Vietnam’s export performance remains exceptionally strong, with volumes up 15.4% and export revenue up 62.6% year-to-date (YTD), evidence that competitive pricing and rising demand for both Robusta and increasingly attractive Vietnamese Arabica are supporting external sales. Growing Arabica exports to South Korea, where Vietnam holds a 19% market share, further signal diversification and rising international confidence in Vietnam’s quality.

Arabica prices are likely to remain firm through early 2026, supported by Brazil’s weather-driven supply risks, continued demand for high-quality beans, and strong export earnings that reduce producer pressure to sell. Without a clear improvement in rainfall patterns in Minas Gerais, upward bias will persist. Robusta is poised for a more mixed path, with Brazil’s prices expected to stabilize near current levels given softer demand and limited export shares, whereas Vietnam could see a moderate recovery if weather conditions normalize and if quality concerns ease, especially with London futures showing renewed buying interest. The market is shifting into a phase of differentiated performance, with Arabica maintaining a bullish structure and Robusta trading in a narrower, more technically driven range.

3. Strategic Recommendations

Optimize Coffee Procurement and Hedging Strategies as Arabica Strengthens and Robusta Remains Supply-Driven

Given the current market structure, buyers and traders should adopt a two-speed strategy that reflects the widening divergence between Arabica and Robusta fundamentals. Arabica retains a bullish trajectory into early 2026 as Minas Gerais weather instability continues to threaten Brazil’s 2026 crop potential, supporting elevated international prices despite recent futures volatility linked to the removal of US tariffs. The ability of Brazilian exporters to maintain a 27.6% revenue increase even with a 20.3% decline in shipped volumes signals a strong global willingness to absorb higher Arabica prices, reducing producer pressure to sell and tightening the supply pipeline. In contrast, Robusta remains influenced by improved availability and more balanced fundamentals, with Brazil showing softer demand and Vietnam navigating weather-related harvest disruptions even as exports surge 15.4% YTD.

In this environment, traders should prioritize long exposure in Arabica through a controlled buildup of Q1–Q2 2026 futures or call-spread structures that limit premium risk while capturing the upside tied to persistent crop uncertainty and strong export valuations. According to data from Tridge Eye, sourcing roasted Brazilian products from firms such as Cruzeiros or Pilão should secure multi-month forward positions to mitigate basis volatility and avoid paying higher premiums once Minas Gerais weather conditions are fully priced in. On the Robusta side, a flexible stance is preferable. Short-term opportunistic buying of Vietnamese volumes is recommended while weather-related quality concerns persist, supported by strong export performance and competitive pricing. Buyers relying on Robusta-heavy blends should diversify origin allocation by combining Vietnam’s expanding supply with smaller Brazilian shipments to protect against regional weather shocks and maintain consistent quality.

For the next 45 to 90 days, importers should advance freight bookings to avoid year-end logistics congestion at Santos and Vietnamese ports, which could tighten spot availability and raise delivered costs. Arabica positions should be reassessed regularly as rainfall updates in Minas Gerais emerge in early 2026, while Robusta exposure should remain optional through call structures or staggered shipment commitments that allow buyers to benefit from any recovery in Vietnamese supply conditions. This dual-track approach ensures that traders capitalize on Arabica’s structurally bullish profile while maintaining the agility needed to navigate Robusta's more technical, weather-driven price environment.