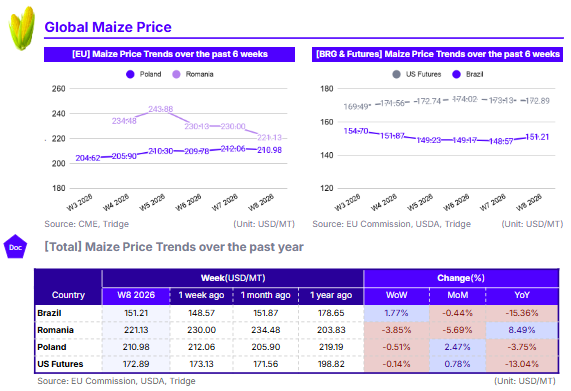

As of W8 2026, global maize prices reflect a surplus-driven market, with double digit YoY deflation in the US and Brazil. US Futures (USD 172.89/mt) dropped 13.04% YoY following a record 17 billion bushel harvest in 2025. Similarly, Brazil (USD 151.21/mt) declined 15.36% YoY due to production recovery, though WoW prices rose 1.77% on safrinha planting delays in Mato Grosso. In the EU, Romania (USD 221.13/mt) saw a 5.69% MoM drop as 2026 production is forecast to rise to 7.79 mmt. Poland remains a cost-effective origin at USD 210.98/mt, despite a 2.47% MoM increase tied to a projected lower 2026 harvest of 9.62 mmt. Buyers are advised to prioritize Poland for EU needs and the US for large-volume global procurement.

1. Weekly Price Overview

Prices in Brazil Rise on Planting Delays While Production Recovery in Romania Weighs on Prices

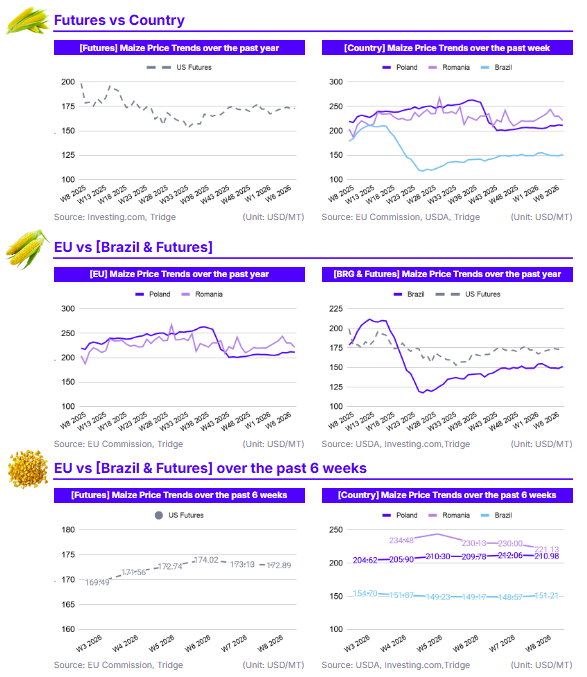

In Brazil, the price of maize was USD 151.21 per metric ton (mt) in W8, reflecting a 1.77% increase week-on-week (WoW). This slight upward movement is primarily attributed to planting progress concerns for the safrinha crop in the Mato Grosso region, where prolonged wet conditions have caused sowings to lag behind the five-year average. Conversely, Romania saw a sharp 3.85% WoW decline to USD 221.13/mt. This downward correction follows a broader trend of high global production and an improved 2026 outlook for the European Union (EU), where Romanian production is forecast to rise to 7.79 million metric tons (mmt) due to improved yields.

Poland and the United States (US) exhibited marginal WoW fluctuations, signaling a period of relative price stability. Polish prices edged down 0.51% WoW to USD 210.98/mt, as the market balances a projected 2026 production decline to 9.62 mmt against the weight of a large global supply. US Futures remained nearly flat, declining 0.14% WoW to USD 172.89/mt. While the US market continues to be anchored by the record 17 billion bushel (approximately 432.34 mmt) harvest of 2025, robust foreign demand provides a steadying influence on weekly prices.

2. Price Analysis

Persistent High Global Supply Continues to Weigh on Long Term Prices

In Brazil, maize prices fell 0.44% over the past month, contributing to a substantial 15.36% total price decrease for the year to USD 151.21/mt. This year-on-year (YoY) decline is primarily driven by the production recovery seen during the 2024/25 cycle. Furthermore, the February WASDE report raised Brazil's 2024/25 production to 136.00 mmt, and with the 2025/26 season expected to reach another record high for national grains, consistent downward pressure remains on long-term values. The marginal month-on-month (MoM) decrease reflects a market that is largely well-supplied despite current planting delays in Mato Grosso.

Romania’s price stands at USD 221.13/mt, having declined 5.69% MoM while maintaining an 8.49% gain YoY. The MoM drop is a response to high global inventories and an optimistic 2026 European Union (EU) outlook, where Romanian production is forecast to climb to 7.79 mmt from the 6.12 mmt recorded in 2025. Although prices are higher YoY, much of this increase in USD terms is attributed to Euro strength against the Dollar rather than local scarcity. In contrast, Poland’s price rose 2.47% MoM to USD 210.98/mt, despite a 3.75% YoY decrease. The MoM strength in Poland is likely due to projections for a smaller 2026 harvest of 9.62 mmt compared to the 10.31 mmt produced in 2025, while downward YoY pressure is due to high global supplies and anticipated improved EU production in 2026.

US Futures are down 13.04% YoY to USD 172.89/mt, while edging up 0.78% over the past month. The heavy YoY deflation is the direct result of the record 17 billion bushel (approximately 432.34 mmt) harvest in 2025. However, the slight MoM firming is supported by robust foreign demand, with the USDA raising 2025/26 export forecasts by 100 million bushels to a record 3.3 billion bushels.

3. Strategic Recommendations

Prioritize Poland for Cost-Effective EU Maize Procurement

European buyers and industrial processors seeking to optimize procurement within the EU should continue to prioritize Poland as their primary sourcing origin. While regional prices in Romania have faced volatility, dropping 5.69% month-on-month (MoM) to USD 221.13/mt, Poland remains more price-competitive at USD 210.98/mt. Although Poland's price saw a modest 2.47% MoM increase due to projections of a slightly smaller 2026 harvest, it remains a stable and lower-cost alternative to Romanian supply, which is still 8.49% higher YoY in USD terms. Furthermore, global and EU-wide production for 2026 is expected to be robust, which will likely keep Polish maize as a cost-effective floor for the region.

Capitalize on Record US Supply for Large-Volume Global Procurement

Global importers looking to source from the Americas and requiring high liquidity and large volumes should focus procurement efforts on the US, which is currently benefiting from a record 2025 harvest of approximately 17 billion bushels (432.34 mmt). Despite a significant 13.04% YoY price drop to USD 172.89/mt, the US market is showing signs of firming MoM due to robust foreign demand, with 2025/26 exports raised by 100 million bushels to a record 3.3 billion bushels. This makes the current window an ideal time to lock in large-volume contracts before potential 2026 market corrections occur. The February WASDE report confirms that US export shipments are running 60% ahead of last year’s pace, particularly to partners like Japan and the EU, underscoring the high global confidence in US supply stability. Given that the 2026 harvest is unlikely to repeat the exceptional 2025 record, prices may face upward pressure in the medium term. Large-scale buyers should leverage the current plentiful supply in the US to fulfill long-term inventory requirements at competitive rates.