In W9 in the tomato landscape, some of the most relevant trends included:

- Germany remains the top market for Italy's Sicilian table tomatoes, accounting for 30% of exports. However, competition is increasing in the German market from Spain, Türkiye, and emerging players like Albania and North Africa.

- In Maharashtra, India, wholesale tomato prices dropped from USD 3.45 to USD 0.92 per 20-kg crate due to oversupply. Meanwhile, Mexico’s tomato prices fell due to high yields in Sinaloa and increased domestic supply.

- Morocco’s prices rose 122.92% MoM due to cold weather and strong export demand; Spain saw an 85% YoY increase from weather-related supply constraints; and Türkiye’s prices climbed 1.85% WoW due to strong export growth.

1. Weekly News

Italy

Sicilian Tomato Exports Face Growing Competition in Key Markets

Germany remains the top market for Italy's Sicilian table tomatoes, accounting for around 30% of total exports in 2024, followed by Great Britain and Scandinavia. However, competition is intensifying. Spain and Türkiye have expanded their presence, with Turkish exports to Germany rising by 17% in 2022. Meanwhile, new players like Albania are emerging alongside traditional competitors from North Africa, adding further pressure to Sicilian tomato producers.

India

Tomato Prices Plunged in Maharashtra Due to Oversupply

In recent weeks, wholesale tomato prices in Maharashtra, India, have plummeted, creating financial distress for farmers. Traders are purchasing a 20-kilogram (kg) crate for USD 0.92, a sharp drop from USD 3.45 per crate a few months ago. Retail prices have also declined, with tomatoes now selling for USD 0.11 to 0.23/kg in W9, compared to USD 0.46/kg in early 2025. The abundant supply of high-quality tomatoes has driven prices down, with farmers struggling to cover labor and transportation costs. Many have abandoned or destroyed crops due to unprofitability, traders report. At Narayangaon, one of Maharashtra’s largest tomato markets, daily arrivals stand at 5,000 crates, lower than last year but still exceeding demand across districts. Farmers attribute the oversupply to high-yield tomato varieties, which mature in just two months and produce up to 5,000 kg/acre, compared to the usual 3,000 to 3,500 kg/acre.

Philippines

Calls for Government Action to Address Tomato Surplus and Prevent Wastage

Industry representatives in the Philippines urged the government to address logistics bottlenecks and invest in storage infrastructure to mitigate tomato wastage amid oversupply. They highlight the need for small- to medium-sized logistics infrastructure in production clusters and propose that the Department of Agriculture (DA) subsidize refrigerated trucks to improve transport efficiency and reduce spoilage. Meanwhile, tomato prices remain critically low, with a 22-kg crate selling for just USD 1.40 in provinces like Nueva Ecija, Nueva Vizcaya, and Pangasinan. Some farmers receive only USD 0.035/kg from middlemen, making harvesting unprofitable. Rural Rising Philippines (a social enterprise dedicated to empowering farmers by providing better market access, fair pricing, and logistical support for their produce), which has been facilitating rescue buys, warns that farmers barely cover transportation costs, forcing many to abandon crops or give tomatoes away for free. Proposed solutions include connecting farmers directly to processing plants and expanding wholesale markets for tomato-based products to stabilize prices and ensure fair returns for producers.

Uganda

Tomato Prices Drove Inflation Surge in Feb-25

According to the Uganda Bureau of Statistics (UBOS), Uganda's monthly headline inflation rose by 0.6% in Feb-25, more than doubling the 0.3% recorded in Jan-25, as tomatoes and fresh leafy vegetables emerged as the primary inflationary drivers. UBOS data released on February 28, 2025 shows that tomato prices spiked from 4.7% in Jan-25 to 12.4% in Feb-25. In absolute terms, tomato prices increased from USD 0.70/kg to USD 0.77/kg.

2. Weekly Pricing

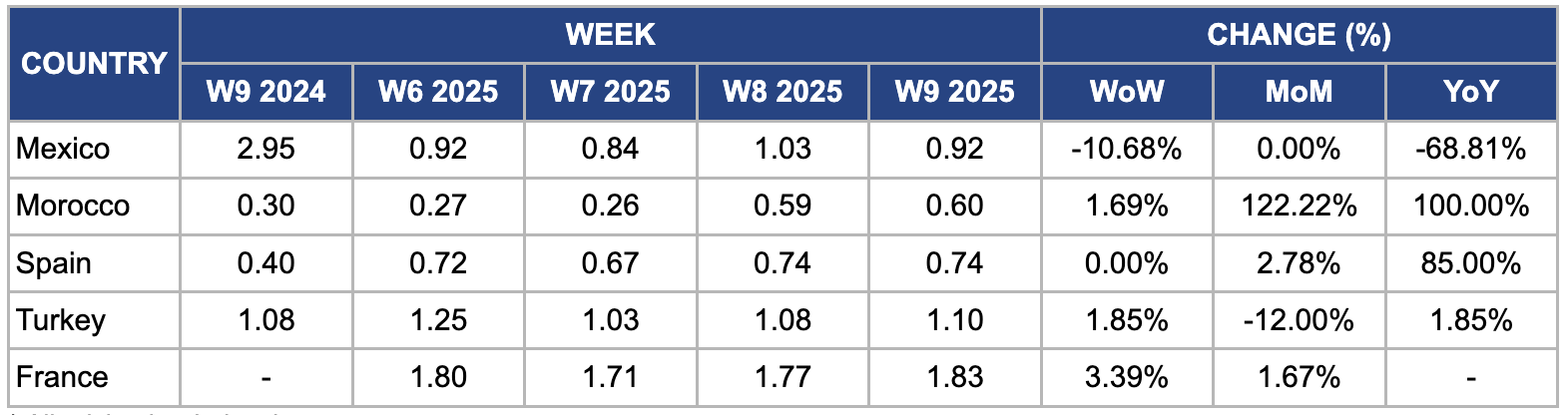

Weekly Tomato Pricing Important Exporters (USD/kg)

Yearly Change in Tomato Pricing Important Exporters (W9 2024 to W9 2025)

Mexico

In W9, Mexico's tomato prices fell 10.68% week-on-week (WoW) and 68.81% year-on-year (YoY) to USD 0.92/kg from USD 1.03/kg in W8. This decline is primarily due to a substantial increase in domestic production, particularly in Sinaloa, which accounts for 22% of national production. Favorable growing conditions have resulted in higher yields, leading to oversupply and downward price pressure. Moreover, the global processing tomato production is projected to decline by 11.5% YoY in 2025, potentially impacting market dynamics and contributing to future price fluctuations. Meanwhile, the recent imposition of a 25% tariff on Mexican tomato exports to the United States (US) may have caused a surge in domestic supply, further intensifying the price drop.

Morocco

In W9, Morocco's tomato prices increased 1.69% WoW and surged 122.92% month-on-month (MoM) to USD 0.60/kg. This sharp price rise is due to cold temperatures and irregular rainfall in key producing regions like Souss-Massa, Agadir, and Chtouka-Aït Baha, resulting in lower yields and delayed harvests, tightening domestic supply. Furthermore, strong export demand from European markets, particularly France and Spain, has intensified competition for available produce, further pushing prices higher. The onset of Ramadan has also boosted local consumption, adding further strain to the already limited supply. These factors combined have contributed to the significant price surge in Morocco's tomato market.

Spain

In W9, Spain's tomato prices remained unchanged WoW but increased 2.78% MoM and 85% YoY to USD 0.74/kg. The price surge is mainly due to adverse weather conditions in Almería and Murcia, where cold temperatures in Feb-25–with daytime averages of 17 to 19°C and nighttime lows of 7 to 9°C–slowed plant growth and delayed harvests, tightening market supply. Furthermore, excessive rainfall disrupted harvesting schedules and reduced quality and availability. However, the Spanish State Meteorological Agency (AEMET) reported a warming trend in the following weeks, with temperatures rising to 22 to 24°C, which could improve growing conditions and stabilize production in the coming weeks.

Türkiye

In W9, Türkiye's tomato prices increased 1.85% WoW to USD 1.10/kg. This price rise is primarily driven by strong export demand, as Türkiye's tomato exports reached USD 536 million in 2023 and continue to grow. The tightened domestic supply due to heightened international demand has exerted upward pressure on prices. Moreover, the Turkish tomato market expanded modestly to USD 8.7 billion in 2024, reflecting a 3.5% YoY increase, signaling robust domestic consumption alongside export growth.

France

In W9, France's tomato prices increased 3.39% WoW to USD 1.83/kg from USD 1.77/kg. This marks a turning point for the market after a month of weak prices in Feb-25 due to sluggish demand. However, market conditions reversed sharply in W8, driven by revived demand. Factors such as the start of the month, schools reopening, improving weather, and a shift toward spring produce have all contributed to higher tomato consumption. Some retail chains are already transitioning to French-grown tomatoes, further boosting demand. With supply struggling to keep up, producers are looking to raise prices in response to the market rebound.

3. Actionable Recommendations

Diversify Export Markets for Sicilian Tomatoes

Sicilian tomato producers depend heavily on Germany, which accounts for 30% of their total exports. However, with increasing competition from Spain, Türkiye, and new players like Albania and North African countries, relying on Germany as a primary market could pose long-term risks. To reduce market saturation and pricing pressure, producers should expand into emerging Eastern European markets such as Poland, the Czech Republic, and Romania, where demand for fresh produce is rising due to growing urban populations and evolving consumer preferences. Moreover, the Middle East presents a promising market, particularly in countries like the United Arab Emirates (UAE) and Saudi Arabia, where high disposable income and reliance on imported fresh vegetables create strong demand. Sicilian exporters can achieve better price stability and reduce dependence on highly competitive Western European markets. Government-backed trade missions and participation in international agri-food expos (such as Gulfood in Dubai) could further facilitate market penetration and direct buyer engagement.

Develop Tomato Processing and Storage Infrastructure

Tomato farmers in India and the Philippines face severe price drops due to oversupply, leading to financial distress and product wastage. One of the biggest challenges is the lack of processing and storage infrastructure, which forces farmers to sell at distressed prices or abandon crops entirely. Investments should be directed toward cold storage facilities and processing units for products like tomato puree, ketchup, dried tomatoes, and canned goods. By setting up small- to medium-scale processing centers near key production areas, farmers could store surplus produce during periods of low demand and sell processed products at better margins. Moreover, governments and private sector players could provide subsidized refrigerated transport to extend tomato shelf life and reduce post-harvest losses. Implementing cooperative models where smallholder farmers collectively invest in storage and processing infrastructure could enhance bargaining power and improve long-term profitability.

Strengthen Supply Chain and Export Logistics

Morocco and Türkiye have seen significant price increases due to supply constraints and strong export demand. Given these trends, Moroccan and Turkish exporters should strengthen their supply chain and logistics infrastructure to maintain their competitive edge in European markets, particularly France, Spain, and Germany. One approach is negotiating long-term freight agreements with European retailers and wholesalers, ensuring consistent supply despite seasonal fluctuations. Moreover, diversifying export logistics by utilizing multiple shipping routes (including rail and sea transport) can reduce delays and cost fluctuations. Investing in pre-cooling facilities at export hubs could improve product shelf life, making Moroccan and Turkish tomatoes more competitive against Spanish and Sicilian varieties. Producers can mitigate price volatility, improve export revenues, and establish stronger market dominance.

Sources: Tridge, Business World, Horti Daily, MyPunePulse, UkrAgroConsult