August 2025 Outlook Report: Grains

Benjamin Lategan

Published Aug 22, 2025

PDF File Preview

- Key Indicators: Global freight prices averaged USD 2,531.25/40-foot container, marking a 25.46% month-on-month (MoM) decline and a 50.19% year-on-year (YoY) drop. The decrease was largely attributed to sluggish demand following an earlier wave of frontloading ahead of the initial Jul-25 tariff deadline. Meanwhile, the World Bank’s Fertilizer Index averaged 154.53 points, an 8.05% MoM increase and a 28.41% YoY rise. The overall gain was driven by notable price increases in urea and diammonium phosphate (DAP), which outweighed a slight decline in potassium chloride.

- Wheat: Australian prices are finding support from a reduced production forecast due to varied weather, although significant rainfall could reverse this trend. In Russia, the forecast is bearish for the Russian market due to a larger national crop from increased plantings, but this is tempered by poor yields in its key southern exporting region which may offer short-term price support. Meanwhile, United States (US) wheat prices are weighed down by harvest pressure and a comfortable global supply outlook. However, tighter domestic stocks and strong export demand are expected to provide a floor for the market, even as global competition limits significant upward price movement.

- Maize: US maize prices are expected to face significant downward pressure due to a record-breaking production forecast, which is leading to the highest ending stocks since the 2018/19 season. In Brazil, maize prices are expected to be balanced, with a record domestic supply capping significant gains, while a strong export forecast, potentially boosted by shifting global trade, provides a supportive floor. Similarly, Argentina’s maize prices will be influenced by competing factors. While a large anticipated domestic crop and strong regional competition may cap price gains, the recent reduction in export duties is expected to enhance export competitiveness.

- Rice: Indian rice prices are expected to remain bearish due to massive domestic stocks and forecasts for another record harvest. Thai rice prices are expected to remain under pressure due to a global oversupply, fierce competition, and the need to clear substantial domestic stocks. Vietnamese rice prices are expected to soften in the near term as temporary demand subsides and the market contends with a global supply overhang.

- Wheat: Australian prices are finding support from a reduced production forecast due to varied weather, although significant rainfall could reverse this trend. In Russia, the forecast is bearish for the Russian market due to a larger national crop from increased plantings, but this is tempered by poor yields in its key southern exporting region which may offer short-term price support. Meanwhile, United States (US) wheat prices are weighed down by harvest pressure and a comfortable global supply outlook. However, tighter domestic stocks and strong export demand are expected to provide a floor for the market, even as global competition limits significant upward price movement.

- Maize: US maize prices are expected to face significant downward pressure due to a record-breaking production forecast, which is leading to the highest ending stocks since the 2018/19 season. In Brazil, maize prices are expected to be balanced, with a record domestic supply capping significant gains, while a strong export forecast, potentially boosted by shifting global trade, provides a supportive floor. Similarly, Argentina’s maize prices will be influenced by competing factors. While a large anticipated domestic crop and strong regional competition may cap price gains, the recent reduction in export duties is expected to enhance export competitiveness.

- Rice: Indian rice prices are expected to remain bearish due to massive domestic stocks and forecasts for another record harvest. Thai rice prices are expected to remain under pressure due to a global oversupply, fierce competition, and the need to clear substantial domestic stocks. Vietnamese rice prices are expected to soften in the near term as temporary demand subsides and the market contends with a global supply overhang.

Table of Content

Part I: Key Indicators

- Freight

- Fertilizer

- FAO Cereals Price Index

Part II: Wheat

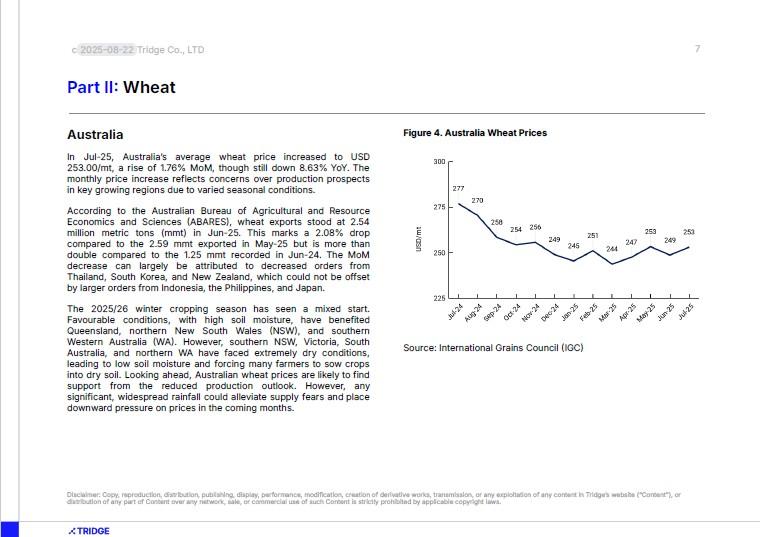

- Australia

- Russia

- United States

Part III: Maize

- United States

- Brazil

- Argentina

Part IV: Rice

- India

- Thailand

- Vietnam

Related market data

Read more relevant content

By clicking “Accept Cookies,” I agree to provide cookies for statistical and personalized preference purposes. To learn more about our cookies, please read our Privacy Policy.

By clicking “Accept Cookies,” I agree to provide cookies for statistical and personalized preference purposes. To learn more about our cookies, please read our Privacy Policy.