In W10 in the maize landscape, some of the most relevant trends included:

- Improved rainfall in Argentina boosted soil moisture, slightly improving corn conditions. Brazil’s Safrinha planting reached 64%, lagging last year due to earlier delays.

- Brazil’s Feb-25 corn exports fell 16.4% YoY in daily shipments due to seasonal factors and logistical disruptions. Meanwhile, Ukraine’s corn exports declined 11% YoY in 2024/25 due to reduced domestic production from adverse weather and conflict.

- US maize prices fell MoM due to improved harvest progress and increased farmer sales, while Brazil’s rose MoM to USD 0.25/kg on strong export demand and logistics disruptions, and Ukraine’s surged YoY due to supply constraints from lower production.

1. Weekly News

Argentina

Argentina's W10 Rainfall Eases Corn Moisture Stress

In W10, improved rainfall boosted soil moisture in Argentinian central production areas, and forecasts predict more rain in central and southern regions that could significantly reduce dryness and moisture stress on corn. By late W10, the Argentine corn harvest reached 5.4%, marking a 3% weekly advance, with early yields averaging 7.79 metric tons (mt) per hectare (ha). The Buenos Aires Grain Exchange (BAGE) reported that 29% of the 2025 corn crop was rated poor/very poor, 50% fair, and 21% good/excellent, with the proportion of good/excellent corn rising by 3% from the previous week. Meanwhile, soil moisture ratings improved by 1%, with 65% of fields now assessed as favorable/optimum, while 34% were rated short/very short, and 1% had surplus moisture.

Brazil

Brazil’s Safrinha Corn Planting at 64%, Lagging Behind 2024 Pace

In W10, Brazilian farmers achieved 64% Safrinha corn planting, down from 73% in 2024, though they advanced 28% over the week. While some planting will continue in Mar-25, the pace remains lower than expected, and with another good week, it reached 85% by March 1. Meanwhile, as harvest operations wrap up in parts of Rio Grande do Sul, Brazil’s first corn crop reached 37% harvested in W10, compared to 42% in 2024. In Mato Grosso, the Mato Grosso Institute Of Agricultural Economics (IMEA) reported that Safrinha corn planting stood at 67.1%, down from 80.3% in 2024 and slightly below the 70.2% average, representing a 22% weekly advance that left the region just 3% behind average. The mid-north region leads the pace, with 78.4% of its Safrinha corn planted.

Brazil's Feb-25 Corn Exports Down 16.4% YoY

According to the Foreign Trade Secretariat (SECEX), unmilled corn shipments (excluding sweet corn) reached 1.43 mmt throughout Feb-25, representing 83.59% of the volume exported in Feb-24 at 1.71 mmt. Over the 20 working days of the month, traders averaged 71,603 mt per day, a 16.4% decline from Feb-24's daily average of 90,162 mt.

Türkiye

Drought Concerns Drive Corn Expansion in Adana, Türkiye

Worried about intensifying drought, farmers in Adana, Türkiye, are increasingly turning to planting corn as a lower-risk alternative. With spring underway, especially in the Kozan district, farmers are actively sowing corn seeds across many fields and shifting more of their production area toward corn. Severe drought conditions have led farmers to allocate 150 ha for corn production out of 200 ha.

Ukraine

Ukraine's Corn Shipments Declined 11% YoY

As of March 5, Ukraine exported 29.68 million metric tons (mmt) of grain and leguminous crops in the 2024/25 marketing year (MY), a 4.4% year-on-year (YoY) decline, according to the Ministry of Agrarian Policy and Food. Corn exports fell by 11.02% YoY to 14.924 mmt, down by 1.645 mmt compared to 2023/24 MY.

United States

USDA Reports 114 Thousand MT Corn Sale to Mexico for 2024/25

On March 3, the United States Department of Agriculture (USDA) reported the sale of 114,000 mt of corn to Mexico, all from the 2024/25 harvest.

2. Weekly Pricing

Weekly Maize Pricing Important Exporters (USD/kg)

Yearly Change in Maize Pricing Important Exporters (W10 2024 to W10 2025)

United States

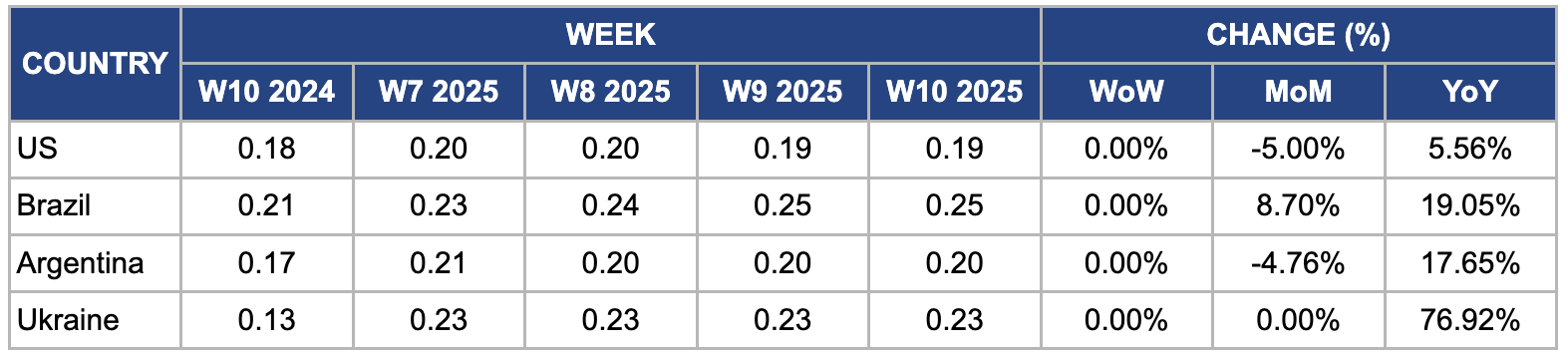

In W10, US wholesale maize prices remained unchanged week-on-week (WoW) but fell 5% month-on-month (MoM) to USD 0.19 per kilogram (kg). Improved weather conditions accelerated harvest progress and boosted farmer sales, driving price drop. Moreover, the USDA reported a sale of 114 thousand mt of corn to Mexico, all sourced from the 2024/25 harvest.

Brazil

In W10, Brazil's wholesale maize prices remained unchanged WoW but rose 8.70% MoM and 19.05% YoY to USD 0.25/kg, driven by strong export demand, particularly from China, as Brazilian corn exports surged 12.3% YoY in Jan-25. Another key factor supporting the price increase is Brazil's seasonal reduction in maize exports as the country enters the off-season. Moreover, domestic logistics disruptions, including transportation delays in Mato Grosso and Paraná due to heavy rains, have slowed shipments to ports and tightened supply. Meanwhile, lower-than-expected early harvest yields in some regions have further pressured prices upward.

Argentina

In W10, Argentine maize prices remained unchanged WoW but declined 4.76% MoM to USD 0.20/kg, driven by improved supply conditions as the harvest progressed and market availability increased. Favorable weather in key maize-producing regions such as Buenos Aires, Córdoba, and Santa Fe likely boosted yields, contributing to the price drop. Meanwhile, currency fluctuations and macroeconomic instability influenced price movements, as the Argentine peso’s depreciation against the US dollar enhanced export competitiveness and led to higher shipments, potentially increasing domestic supply. However, inflation and financial instability may have raised production costs and affected farmer selling decisions, adding to overall price volatility.

Ukraine

In W10, Ukraine's wholesale maize prices remained stable WoW but surged 76.92% YoY to USD 0.23/kg. This significant YoY increase was primarily due to severe supply constraints from reduced domestic maize production. Adverse weather conditions, including below-average temperatures and insufficient rainfall during the growing season, combined with ongoing conflict-related disruptions in key producing regions, led to a decline in production from an estimated 32 mmt in 2022 to roughly 28 mmt in 2023 and further down to approximately 24 mmt in 2025. This production shortfall and strong export demand in a recovering global market compressed supply and pushed prices sharply higher over the past year, even as WoW conditions have remained stable.

3. Actionable Recommendations

Enhance Brazil’s Maize Export Logistics to Overcome Delays

Brazil's maize exports face strong demand, especially from China, but logistical bottlenecks, including heavy rains in Mato Grosso and Paraná, have delayed shipments and tightened domestic supply. Seasonal export reductions have further contributed to price increases. To mitigate these challenges, exporters should expand rail and inland water transport to reduce reliance on weather-sensitive truck routes. Investing in additional storage near export hubs can also help maintain a steady flow of shipments. These measures will improve Brazil’s export reliability, enhance competitiveness, and prevent costly delays in international markets.

Capitalize on Improved Argentina’s Improved Maize Yields to Strengthen Regional Trade

Argentina’s maize production outlook has improved with better rainfall, boosting yields in Buenos Aires, Córdoba, and Santa Fe. The peso’s depreciation has made exports more competitive, but economic instability and inflation still create market volatility. Argentine traders should secure long-term contracts with key buyers like Vietnam and Egypt while using forward contracts to hedge against currency risks to maximize export potential. Expanding storage and improving port logistics will also ensure smooth exports, stabilizing domestic prices and maintaining Argentina’s strong market position.

Monitor Ukraine’s Supply Constraints to Optimize Buying Strategies

Due to supply constraints, Ukraine’s maize production has fallen due to weather and conflict-related disruptions, with YoY prices surging nearly 77%. Logistical challenges, including restricted port access, have created market uncertainty. Importers should monitor Ukraine’s export conditions closely while diversifying sourcing from Brazil and Argentina to avoid supply shocks. Securing advance purchase agreements with fixed pricing can help stabilize costs and reduce risk, ensuring a steady maize supply despite Ukraine’s ongoing challenges.

Sources: Tridge, NoticiasAgricolas, UkrAgroConsult