In W13 in the orange landscape, some of the most relevant trends included:

- Cyprus and Egypt are experiencing high demand for oranges, which is outpacing supply and leading to elevated prices. Markets in the Far East, Norway, and New Zealand are seeing strong demand for late-season varieties, causing shortages.

- Both Egypt and Florida are facing challenges in meeting global market requirements, with a significant portion of production not qualifying for export. Issues such as sourcing suitable fruit and declining yields are impacting exports.

- As global competition intensifies, Mexico and Egypt are exploring new markets, while established markets like the UK are seeing declining citrus consumption. Exporters are focusing on diversifying destinations to mitigate reliance on traditional markets.

- Hurricanes in Florida and HLB disease are severely affecting orange production, particularly in the US. Similar challenges are seen in Brazil due to drought conditions impacting production.

1. Weekly News

Cyprus

Cyprus Orange Supply Struggles to Meet Rising Demand

In Cyprus, demand for Late Ovals, including Morphou and Lefka oranges, has outpaced supply, leading to elevated prices since March. Typically available until mid-May, the crop is expected to run out soon due to strong demand from markets like Norway, New Zealand, and the Far East. As of early April, the remaining Late Ovals are nearing depletion. Growers receive USD 14.40 (GBP 11) per thousand for Late Ovals and USD 15.71 (GBP 12) for Valencia Lates. In response, exporters are shifting focus to new markets, reducing shipments to traditional destinations such as the United Kingdom (UK), where citrus consumption has been declining.

Egypt

Egypt's Orange Season Faces Challenges Due to Rising Local Demand

The Egyptian orange campaign is nearing its early end due to difficulties in sourcing suitable fruit for export. Only 20% of the production meets the size requirements, with just 40% of that qualifying for international markets, making the season particularly challenging. The emergence of new players in the processing sector, driven by a shortage of oranges in Brazil, has fueled local demand, pushing prices to unprecedented levels and intensifying competition for exporters. Despite having their production, exporters like Al Solimania have faced ongoing supply shortages. Russia remains the dominant market, receiving nearly 80% of Egypt's exports, while the Caribbean has emerged as a promising new destination.

Mexico

Mexico's Valencia Orange Production Thrives Due to Global Demand

Oranges are among the most consumed fruits worldwide, with major producers like Brazil, Spain, Egypt, and the United States (US) driving fresh and processed orange exports. In Mexico, Valencia oranges are the most widely grown variety, known for their sweetness, thin peel, and high juice content. Veracruz leads the country's production, accounting for over half of Mexico’s total orange output. In 2023, the state cultivated 168.9 thousand hectares (ha) of Valencia oranges, yielding 2.5 million metric tons (mmt) out of Mexico’s total 4.7 mmt. Orange availability peaks in March, when the highest percentage of annual production is harvested.

United States

Florida’s Orange Industry Faces Historic Crisis Due to Declining Production and Global Pressure

According to the United States Department of Agriculture (USDA), orange production in the US, particularly in Florida, is facing its most severe crisis since World War II, with the 2024/25 harvest projected at just 11.5 million boxes, a 30% year-on-year (YoY) decline. This sharp drop is due to a combination of factors, including devastating hurricanes, the persistent citrus greening disease (HLB), and long-term shifts in consumer behavior, with orange juice consumption in the US falling by over 50% in recent decades. Major brands are struggling with declining profitability, and as Florida’s groves continue to suffer, global competition from countries like Brazil and Spain intensifies. While Brazil also faces production challenges due to a prolonged drought, recent rainfall offers some hope for the upcoming season.

2. Weekly Pricing

Weekly Orange Pricing Important Exporters (USD/kg)

Yearly Change in Orange Pricing Important Exporters (W13 2024 to W13 2025)

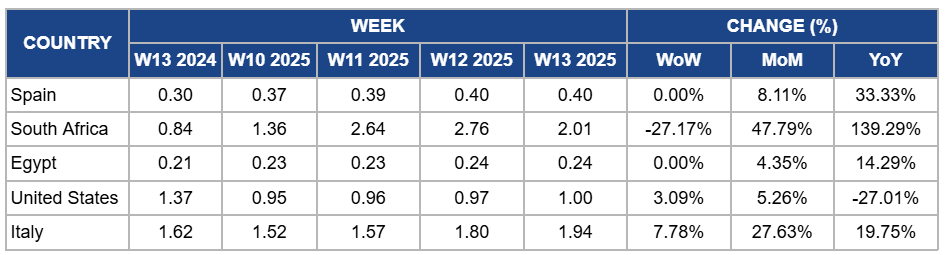

Spain

Spain's orange prices remained steady week-on-week (WoW) at USD 0.40 per kilogram (kg) in W13, with an 8.11% month-on-month (MoM) and a 33.33% YoY increase due to continuing supply constraints from recent adverse weather conditions affecting key citrus-producing regions. The persistent rainfall in Andalusia, Valencia, and Murcia has led to delayed harvesting and reduced supply. Additionally, the quality of late-season varieties like Lane Late and Salustiana has been compromised.

South Africa

In W13, orange prices in South Africa dropped by 27.17% WoW to USD 2.01/kg due to the seasonal shift from the earlier Navel orange variety to the start of the main harvest. This change resulted in a temporary increase in the supply of smaller and less mature fruit, which typically commands lower prices. Additionally, logistical bottlenecks, including delays in transport and port congestion, impacted the timely delivery of oranges to key export markets, further driving down prices. However, there is a 47.79% MoM increase and a 139.29% YoY price surge due to tight early-season supply, as the main harvest usually begins in April. Additionally, strong demand from international markets such as Europe and Asia, coupled with rising production and logistics costs, has pushed prices higher compared to both the previous month and the same period last year.

Egypt

Orange prices in Egypt held steady WoW at USD 0.24/kg in W13, marking an increase of 4.35% MoM and a 14.29% YoY surge. This price rise is due to ongoing logistical challenges, particularly disruptions in the Red Sea region caused by regional instability, which have led to rerouted shipping and increased costs. These factors have significantly impacted Egyptian citrus exports, especially oranges, leading to higher market prices. Additionally, the emergence of new players in the processing sector, driven by a shortage of oranges in Brazil, has fueled local demand, further supporting price increases.

United States

In the US, orange prices increased slightly by 3.09% WoW to USD 1/kg in W13, reflecting a 5.26% MoM rise. This uptick is due to significant production challenges in key citrus-producing regions, notably Florida. The 2024/25 harvest is projected at just 11.5 million boxes, a 30% YoY decline, driven by devastating hurricanes and the persistent HLB disease. These production constraints have led to reduced supply, supporting higher prices. However, YoY prices dropped by 27.01% due to reduced consumer demand and increased production costs. Orange juice consumption in the US has fallen by over 50% in recent decades, influenced by changing consumer preferences and elevated prices. Additionally, the emergence of new players in the processing sector, driven by a shortage of oranges in Brazil, has intensified competition, further impacting prices. These factors have contributed to the observed YoY price decrease.

Italy

Orange prices in Italy increased by 7.78% WoW to USD 1.94/kg in W13, with a 27.63% MoM increase and a 19.75% YoY increase. This significant price rise is due to a substantial reduction in local orange production, especially in Sicily, where severe drought conditions have led to an estimated 50% decrease in the 2024/25 season. The diminished supply has intensified competition for available oranges, driving prices upward. Additionally, increased demand for high-quality Italian oranges in both domestic and export markets has further contributed to the price escalation.

3. Actionable Recommendations

Adapt to Shifting Market Demands and Improve Resilience

Orange growers in Florida should focus on diversifying their production to include varieties that are more resistant to diseases like HLB. This could involve investing in disease-resistant rootstocks and enhancing grove management practices, such as improving irrigation systems and soil health. Additionally, growers should explore alternative markets, such as fresh fruit sales or value-added products like marmalades, to offset the decline in orange juice demand. Collaborating with research institutions to develop innovative solutions and adopting more efficient farming technologies will also help improve long-term resilience and competitiveness.

Optimize Sourcing and Expand Market Reach

Egyptian orange exporters should collaborate with local farmers to implement better cultivation practices, ensuring that a higher percentage of fruit meets export standards. This could include offering training on proper irrigation, pest control, and fruit size management. Additionally, exporters should explore diversifying into more stable markets outside of Russia, such as expanding exports to the Caribbean and emerging markets in Asia. Strengthening relationships with processing sectors to ensure better use of lower-grade fruit could also mitigate supply shortages.

Sources: Tridge, AS, Elperiodicomediterraneo, Farmagusta Gazette, Freshplaza, Portalfruticola