In W14 in the soybean landscape, some of the most relevant trends included:

- The EU plans to impose 25% retaliatory tariffs on US agricultural products, including soybeans, potentially reducing US soybean exports to the EU.

- Argentina lowered its soybean harvest projection due to rainfall. However, crop conditions have improved for five consecutive weeks, with 29% of the crops rated good/excellent. Soil moisture levels have also improved, supporting better yield potential.

- Brazil has reduced its soybean crop forecast due to adverse weather in Rio Grande do Sul, which led to price declines. The increased global supply, particularly from the US and Argentina, and weaker demand from China further contributed to the price softness.

1. Weekly News

Europe

US Soybean Exports to EU Face Setback Amid Retaliatory Tariff Threat

The European Union (EU), traditionally the second-largest buyer of United States (US) soybeans after China, is preparing to impose 25% retaliatory tariffs on US agricultural products, including soybeans, in response to US duties on steel and aluminum imports. This move will negatively impact US soybean exports to the EU. In the 2024/25 season, the US is projected to export around 50 million metric tons (mmt) from its nearly 119 mmt crop. Although China remains the primary destination, the EU also plays a crucial role, having imported 5.3 mmt of US soybeans last season. However, during the current season up to March 16, 2025, the EU had imported 9.6 mmt of soybeans, with the US accounting for 5.1 mmt (53%). Yet, this trend may shift as Brazil’s 2025 harvest becomes available and offers ample supply to global markets in the coming months. With punitive tariffs set to take effect in mid-Apr-25 and global supplies remaining strong, EU importers are expected to pivot toward South American and possibly Ukrainian soybeans. As a result, US soybean producers risk losing a key export market.

Argentina

W14 Rains in Argentina Delay Harvest as Soybean Conditions Improve

In Argentina, weekend rainfall in central regions and a wetter forecast for the next one to two weeks may slow ongoing corn and early soybean harvests. Farmers have likely harvested less than 1% of soybean fields, leaving yield outcomes uncertain until more reports emerge. Despite limited progress, soybean conditions have improved for five consecutive weeks, which may lead to better yields. By late W14, analysts rated soybean conditions at 27% poor, 44% fair, and 29% good/excellent, an increase of 5% week-on-week (WoW) in the good/excellent category. The Buenos Aires Grain Exchange (BAGE) reported soil moisture conditions at 16% short/very short, 82% favorable/optimum, and 2% saturated, with favorable/optimum moisture rising by 2% WoW as of March 19, 2025.

Brazil

Brazil’s 2024/25 Soybean Forecast Downgraded Due to Weather Setbacks in Rio Grande do Sul

Brazil's 2024/25 soybean crop forecast was reduced from 168.34 mmt to 167.54 mmt, mainly due to unfavorable weather conditions in the Rio Grande do Sul. These adverse weather conditions, including drought, excessive rainfall, or extreme temperatures, likely affected crop development and reduced yield in the region. Rio Grande do Sul is a key soybean-producing state in Brazil, so weather-related setbacks significantly impact the national crop estimate. Such conditions can reduce the area suitable for planting or decrease the yield potential per hectare (ha), leading to a downward revision.

Russia

IKAR Forecasts Increased Soybean and Oilseed Production for 2025/26 in Russia

For the 2025/26 seasons, the Institute for Agricultural Market Studies (IKAR) forecasts a soybean harvest of 8.38 mmt, up from approximately 7 mmt the previous year. The total oilseed harvest will reach 33 mmt, an increase of 3.6 mmt compared to the current season. This growth is due to an expansion in sowing areas, which will rise from 4.2 million ha to 4.5 to 4.6 million ha. However, IKAR highlights that farmers' attitudes towards soybeans are varied, with some reducing their planted areas or abandoning soybean production altogether, depending on the region.

2. Weekly Pricing

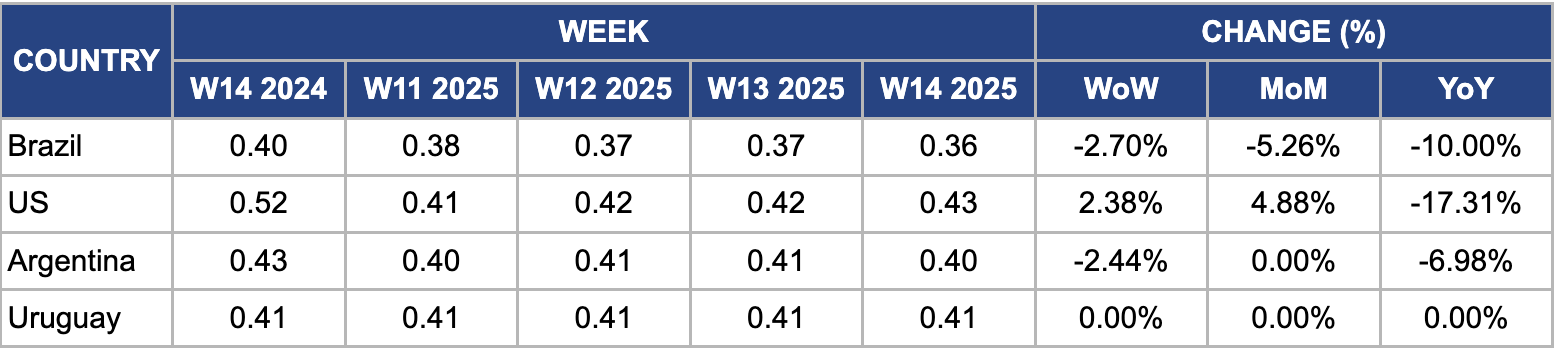

Weekly Soybean Pricing Important Exporters (USD/kg)

Yearly Change in Soybean Pricing Important Exporters (W14 2024 to W14 2025)

Brazil

In W14, Brazil’s soybean prices declined due to several market factors. The 2.70% WoW and 5.26% month-on-month (MoM) declines can be attributed to an increase in global soybean supply, particularly from competing countries like the US and Argentina, which led to a more saturated market. Moreover, weaker demand from major importers, such as China, contributed to price softness, as China’s economic slowdown and reduced livestock feed requirements led to a decline in soybean purchases. On a year-on-year (YoY) basis, the 10% decrease reflects the impact of Brazil's record soybean production in the 2024/25 season, which increased the country’s exportable surplus and contributed to downward pressure on prices. The lower-than-expected demand from global buyers and ongoing logistical challenges in key export corridors, such as the congestion at ports, compounded the pricing pressure.

United States

In W14, US soybean prices increased by 2.38% WoW and 4.88% MoM to USD 0.42/kg but experienced a significant 17.31% YoY decrease. The price increase was due to various market factors, including the proposed US port fee on Chinese-built vessels, which aims to support domestic shipbuilding but could also elevate soybean export costs. The American Soybean Association (ASA) estimates that this fee could raise export costs by approximately USD 0.39 per bushel, increasing freight rates and potentially reducing farmgate prices. This added cost burden, coupled with already challenging conditions within the US farm economy, could diminish the competitiveness of US soybeans in the global market, especially in comparison to lower-cost producers in South America.

Argentina

In W14, Argentina's soybean prices declined by 2.44% WoW and 6.98% YoY.. The slower-than-usual sales of the 2024/25 harvest, with only 17 to 18% sold by mid-Mar-25, reflects farmers’ hesitation to sell their crops amid economic uncertainty and anticipation of a stronger Argentine peso. This slowdown is a significant departure from the usual pace, with sales down 25% compared to last year. As a result, Argentina's foreign exchange earnings are impacted, as soybean exports are a critical source of economic stability. Farmers are holding off on sales, hoping for better exchange rates, which adds to market instability. The Argentine government is under increasing pressure to find ways to stimulate soybean sales.

Uruguay

In W14, Uruguay's soybean prices remained stable at USD 0.41/kg, reflecting expectations of a strong harvest due to favorable weather conditions. Despite this, international prices have remained lower, which continues to exert pressure on margins for producers. As a result, farmers are adjusting their hedging strategies to manage financial risks more effectively. The reference price for soybeans stood at USD 364 per metric ton (mt), below the levels seen in 2023. However, this price is supported partially by higher premiums stemming from shifts in international purchasing patterns, impacting global demand and trade dynamics.

3. Actionable Recommendations

Diversify Export Markets Amid EU Tariff Threats

To mitigate the impact of EU retaliatory tariffs on US soybeans, US exporters should expand their market diversification efforts, focusing on alternative buyers in Southeast Asia, Africa, and Latin America, where demand for soybeans is growing. Moreover, targeting the food and biofuel sectors in these regions may help offset losses in traditional export markets. Reduced reliance on EU markets, ensuring stable revenue streams despite tariff challenges.

Accelerate Strategic Sales in Argentina to Counter Economic Volatility

Farmers and exporters must lock in favorable prices in response to Argentina's sluggish soybean sales and economic uncertainty. They can achieve this by negotiating forward sales agreements and engaging in pre-sale hedging strategies. By securing export contracts ahead of time, exporters can guarantee sales volumes and lock in favorable pricing before market fluctuations, thus avoiding peso volatility. Farmers can use advanced market analytics to identify the optimal windows for forward contracts based on exchange rate movements and market conditions. This approach will allow exporters to anticipate favorable price movements and hedge against potential losses caused by currency devaluation or market downturns. These actions will enhance the financial stability of farmers by safeguarding their revenue in the face of economic instability.

Optimize Logistics and Export Strategies in Brazil to Offset Price Weakness

With the oversupply of soybeans, mainly from Brazil’s record crop, and the subsequent decline in soybean prices, exporters must improve logistical efficiency to remain competitive. The current port congestion and freight delays are significant hurdles to achieving cost-effective exports. To address this, exporters should actively seek alternative export routes and invest in infrastructure improvements. For instance, enhancing rail and river transportation could reduce the dependency on crowded ports, helping to lower transport costs and avoid delays. Efficient rail systems can ensure that soybeans reach ports quicker while investing in river infrastructure allows for alternative waterways for bulk exports. These logistical upgrades will reduce export costs, enabling exporters to pass on savings to buyers, thereby maintaining price competitiveness in a saturated global market.

Sources: Tridge, Agro Investor, Chacra Magazine, UkrAgroConsult