In W2 in the maize landscape:

- Argentina’s 2024/25 corn planting area expanded to 6.6 million ha, signaling a strong production outlook for the upcoming season.

- In Brazil, summer corn planting progress reached 83.7%, slightly behind last year. However, 2024 corn exports declined by 28.8% YoY due to reduced production, although domestic markets remained relatively stable.

- China reduced its corn import forecast, increasing reliance on domestic production to meet demand.

- In Ukraine, corn exports to the EU decreased slightly to 14.06 mmt. Maize prices surged WoW and YoY, driven by a severe drought that caused a significant drop in production.

- In the US, maize prices rose MoM as the USDA revised production forecasts downward due to lower yields, tightening supply expectations.

- In Brazil, maize prices remained steady despite a decline in export volumes.

1. Weekly News

Argentina

Argentina Revised Corn Planting Estimates for 2024/25

The Buenos Aires Grains Exchange (BAGE) revised Argentina's 2024/25 corn planting area upward to 6.6 million hectares (ha), an increase from the earlier estimate of 6.3 million ha. A leading corn exporter and the top global supplier of soy byproducts, Argentina sees high competition between corn and soybean for planting areas. As of Jan-25, 85% of the corn fields have been planted.

Brazil

Brazil's Summer Corn Planting Progressed to 83.7% Completion

The National Supply Company (CONAB) reported that planting for Brazil's 2024/25 summer corn harvest reached 83.7% as of January 5, up from 80.8% the previous week but slightly behind the 84.3% progress recorded during the same period in the 2023/24 cycle. Planting is complete in Goiás, Minas Gerais, São Paulo, Paraná, and Santa Catarina, while other states such as Rio Grande do Sul (94%), Bahia (75%), Piauí (45%), and Maranhão (30%) are still progressing. Despite steady advancements, this year's planting pace remains marginally slower than the previous season.

Brazil’s 2024 Corn Exports Dropped 28.8% YoY

In 2024, Brazil's corn exports experienced a significant decline of 28.8% year-on-year (YoY), totaling 39.783 million metric tons (mmt), driven by lower production and increased domestic demand. Despite this, the domestic market remained stable, with stocks staying well-supported. This year, there is potential for a recovery in exports, supported by anticipated higher supply and favorable exchange rate conditions, especially if the dollar continues to appreciate against the Brazilian real. Moreover, China's stance on Brazilian corn exports could play a crucial role, as China accounted for 27% of Brazil's corn exports in 2023. The ongoing political tensions between China and the United States (US), particularly around trade, could further shape the demand landscape for Brazilian corn.

China

China Cuts 2024/25 Corn Import Estimate to 9 MMT

China’s Ministry of Agriculture raised its corn production forecast for the 2024/25 crop year to 294.92 mmt, a 0.4% increase from previous estimates. At the same time, the import forecast was cut sharply to 9 mmt, down from 13 mmt, marking a significant decline compared to the 23.4 mmt imported in the 2023/24 season. The ministry attributed the reduced imports to high domestic demand for feed and processing, which is expected to remain strong throughout the upcoming crop year.

Ukraine

Ukraine's Corn Exports to EU Dip to 14.06 MMT in 2024

Ukraine exported 14.06 mmt of corn to the European Union (EU) in 2024, a reduction of 1.2 mmt compared to 2023. Despite the decline, the EU remains Ukraine's primary corn market, accounting for 49.2% of its total corn exports.

Corn Exports from Ukraine Slightly Declined in 2024/25

According to the Ministry of Agrarian Policy and Food, Ukraine's grain and pulse exports for the 2024/25 marketing year (MY) rose by 15.5% YoY as of January 8, reaching 22.442 mmt. However, corn exports experienced a slight decline of 1.5% YoY, totaling 10.162 mmt.

2. Weekly Pricing

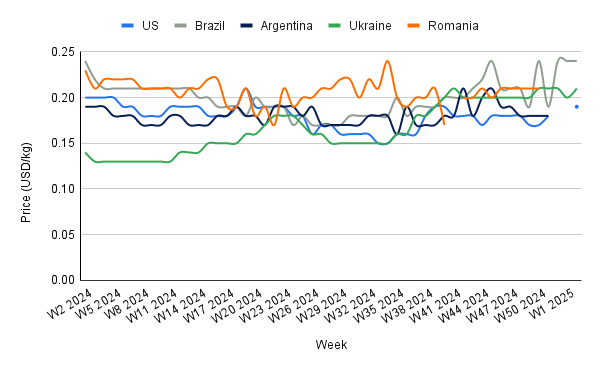

Weekly Maize Pricing Important Exporters (USD/kg)

Yearly Change in Maize Pricing Important Exporters (W2 2024 to W2 2025)

US

In W2, wholesale maize prices in the US rose by 5.56% month-on-month (MoM), reaching USD 0.19 per kilogram (kg). The United States Department of Agriculture (USDA) has revised its corn production forecasts for the 2024/25 season, projecting a decrease in yields to result in a corn harvest of 377.63 mmt, down by 7 mmt from the Dec-24 estimate. The lower production forecasts have also led to a projected drop in corn stocks in the US by 5.03 mmt by the end of the period.

Brazil

In W2, wholesale maize prices in Brazil stood at USD 0.24/kg, remaining unchanged week-on-week (WoW) and YoY. This stability is primarily due to balanced supply and demand dynamics in the Brazilian maize market during this period. The USDA reports that Brazil's corn production is projected to reach 127 mmt in the 2024/25 MY, a significant increase from the previous year's 119.74 mmt. This growth is attributed to favorable weather conditions and increased planted acreage. Despite the increased production, domestic demand remains robust, driven by the livestock sector's need for animal feed and the food processing industry's requirements. The CONAB estimates that Brazil's total corn crop in the 2024/25 season will be 4,717 million bushels, a 3.6% YoY increase.

Ukraine

In W2, wholesale maize prices in Ukraine increased 5% WoW and 50% YoY to USD 0.21/kg. This significant price increase is primarily due to a substantial reduction in maize production due to severe drought conditions. The USDA reports that Ukraine's corn production is projected to fall to 25 mmt in the 2024/25 MY, a 23% decrease from 2023/24 and the lowest level since 2017. The drought has adversely affected crop yields, leading to a tighter supply of maize in the domestic market. This reduced availability has exerted upward pressure on prices. Moreover, the Ukrainian hryvnia (UAH) strengthening against the US dollar (USD) has made Ukrainian maize more expensive for foreign buyers, further reducing demand.

3. Actionable Recommendations

Develop Partnerships with Feed and Food Processing Companies

For Brazil and Argentina, forging long-term partnerships with feed manufacturers and food processing companies can create stable demand and mitigate price volatility. Farmers can secure long-term contracts with agreed pricing, ensuring a stable market for their produce while minimizing the risk of market fluctuations. Moreover, these partnerships can provide access to pre-financing for seed procurement and production, further strengthening financial stability for growers.

Strengthen Export Diversification to Non-Traditional Markets

With Argentina’s increased corn planting area and Brazil’s growing production, expanding to non-traditional export markets is essential for sustainability, such as Africa, where corn imports are projected to grow significantly. By establishing partnerships with local importers in countries like Nigeria or Ghana, Argentina can tap into new demand sources driven by population growth and increased food consumption. Similarly, Brazil should target Southeast Asian countries such as Vietnam and Indonesia, where feed demand for livestock is booming due to rising meat consumption. Exporters in both countries can offer competitive pricing and fulfill the growing need for corn in these emerging markets, reducing dependency on traditional buyers like China.

Invest in Climate-Resilient Corn Varieties and Water Management Systems

Ukraine should invest in climate-resilient corn varieties to address drought impact. These varieties, such as drought-tolerant hybrids like DKC9023 or Pioneer P9913, are engineered to withstand dry conditions without compromising yield. Alongside seed improvement, implementing advanced irrigation systems like drip irrigation or precision sprinklers can optimize water usage during dry spells. Furthermore, soil moisture sensors can help farmers monitor water availability more accurately, ensuring efficient irrigation and preventing overuse. By adopting these technologies, farmers can increase yield stability and reduce the impact of future droughts, safeguarding productivity and income.

Sources: Tridge, Food Mate, NoticiasAgricolas, UkrAgroConsult