1. Weekly News

Global

USDA Forecasts Slight Decline in Global Corn Production for 2024/25 Season

In its May-24 report, the United States Department of Agriculture (USDA) forecasted global corn production for the 2024/25 season at 1.219 billion metric tons (mt), slightly lower than the 1.228 billion mt produced in 2023/24. Notably, the United States (US) is expected to harvest 377.46 mmt, down from 389.69 mmt in the 2023/24 season, while Argentina's production is projected at 51 mmt, down from 53 mmt. Brazil is expected to increase its output to 127 mmt from 122 mmt, and Ukraine's production is forecasted to decline to 27 mmt from 31 mmt. The global corn export forecast for 2024/25 is 191 mmt, down from 197.38 mmt in 2023/24, with the US expected to increase its exports to 55.88 mmt, Argentina to export 36 mmt, Brazil 49 mmt, and Ukraine 24 mmt. Global ending stocks for 2024/25 are estimated at 312.27 mmt, a slight decrease from the 313.08 mmt predicted for the end of the current season.

Brazil

Brazilian Corn Exports Dip in May-24

According to the Foreign Trade Secretariat (Secex), Brazil shipped 96,649.5 mt of unground corn on May-24, constituting 25.11% of the total exported on May-23, which stood at 384,884.8 mt. The daily average of shipments until the second week of May-24 was 13,807.1 mt, reflecting a 21.1% year-on-year (YoY) decrease, which recorded a daily average of 17,494.8 mt. Moreover, Brazilian corn exports will fall below last year's figures due to a reduction in production forecasts for 2024 compared to 2023.

France

France's Maize Area Expected to Increase by Nearly 10% YoY in 2024

France's farm ministry projects a nearly 10% YoY increase in grain maize area for the 2024 planting season as farmers pivot to spring varieties following heavy rain that damaged winter crops. The forecast indicates that farmers will plant 1.44 million hectares (ha) of grain maize, including seed crops, representing a 9.6% YoY increase. Despite this increase, the area remains 5% below the five-year average and is the second-smallest in three decades after last year's low. Although initial rain delays raised concerns about maize planting, a recent warm and dry spell likely facilitated fieldwork. The ministry attributes the shift to spring crops to the decline in winter crop sowing due to adverse weather conditions.

United States

US Corn Planting and Emergence Rates Increased

According to the USDA, the corn planted area index as of May 12 increased from 36% to 49% over the past week, aligning with market expectations. This compares to 60% in the same time in 2023 and an average of 54%. Additionally, the report indicated that 23% of corn crops are in the emerging phase, up from 12% the previous week, though slightly behind the 25% seen in 2023 and the 21% average.

Zimbabwe

Zimbabwe Corn Harvest Down 72% YoY Due to Severe Drought

Zimbabwe is facing a severe drought, resulting in a 72% YoY decrease in its corn harvest, with maize production expected to drop to 634,699 mt compared to 2023. This decline is attributed to the El Niño weather phenomenon, marking the season as the latest and driest in 40 years. Consequently, Zimbabwe plans to import at least 1.4 mmt of maize by Jul-24 to compensate for the shortfall. The country consumes 2.2 mmt of maize annually, with 1.8 mmt needed for food and 400 thousand mt for livestock feed.

2. Weekly Pricing

Weekly Maize Pricing Important Exporters (USD/kg)

Yearly Change in Maize Pricing Important Exporters (W20 2023 to W20 2024)

.png)

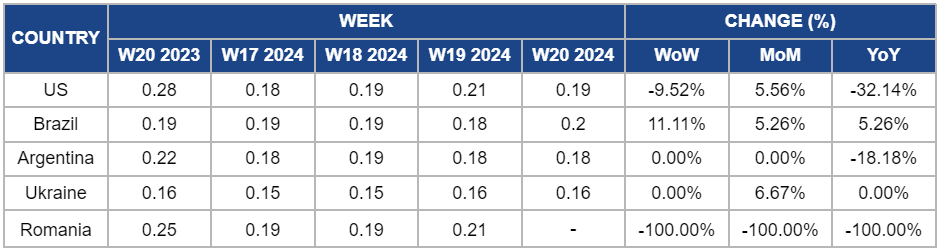

United States

The US wholesale maize price experienced a notable 9.52% week-on-week (WoW) decline, dropping from USD 0.21 per kilogram (kg) in W19 to USD 0.19/kg. This price reduction comes as improved growing conditions across Texas and the broader US are expected to yield above-average crop outputs. As a result, corn prices and the acreage devoted to corn cultivation decreased in response to these favorable agricultural conditions.

Brazil

The wholesale price of Brazilian maize increased by 11.11% WoW to USD 0.20/kg in W20. This notable increase is due to the impact of heavy rainfall and flooding in the southern region of Brazil, particularly in areas like Mato Grosso do Sul. The flooding, which even led to a dam break, has raised concerns about the condition of the corn crop, prompting close monitoring by the corn market.

Argentina

The wholesale price of Argentinian maize remained unchanged WoW at USD 0.18/kg, despite the USDA lowering corn production estimates for Argentina to 53 mmt from the previous estimate of 55 mmt in Apr-24.

Ukraine

Ukrainian maize prices held steady WoW at USD 0.16/kg. This stability coincided with the forecast for the corn harvest in Ukraine for 2024, which remained unchanged at 30.5 mmt.

3. Actionable Recommendations

Implement Contingency Plans for Delayed Harvests

Due to the wet weather conditions affecting corn harvest progress in key producing countries like Argentina and Brazil, farmers must establish and execute contingency plans to alleviate potential yield losses and operational disruptions. These plans should entail optimizing machinery maintenance schedules, adapting harvesting techniques to suit field conditions, and prioritizing harvesting in areas with more favorable weather forecasts. Moreover, close monitoring of weather updates and collaboration with local agricultural extension services for timely guidance on harvest management practices are crucial.

Enhance Supply Chain Resilience

To address disruptions in corn exports caused by weather-related challenges and market dynamics, exporters in major corn-producing nations, such as Brazil, Argentina, and the US, need to bolster supply chain resilience. This involves strategies like diversifying export destinations to reduce reliance on specific markets, enhancing logistics infrastructure to improve transportation efficiency, and implementing risk management protocols to mitigate the impact of price volatility and trade disruptions.

Diversify Crop Portfolio and Income Streams

Given the uncertainties and volatility in the corn market, farmers should consider diversifying their crop portfolio and income streams to mitigate risk exposure. Exploring alternative crops and value-added opportunities, such as soybeans, wheat, pulses, oilseeds, fruits, vegetables, and livestock, alongside corn production can provide diversified sources of income. Adopting integrated crop-livestock systems, agroforestry practices, and diversified farming models can optimize resource utilization, enhance farm profitability, and bolster ecological resilience. Furthermore, strengthening market linkages, value chains, and agribusiness networks will facilitate access to diverse market outlets and capitalize on value-added opportunities across different agricultural sectors.