W22 2025: Orange Weekly Update

In W22 in the orange landscape, some of the most relevant trends included:

- Australia’s orange industry anticipates export growth in 2025. Moora Citrus expects a 10 thousand mt harvest, despite the warm autumn delaying fruit maturation and ongoing labor and climate challenges.

- Mexico’s orange production in Tamaulipas has dropped by up to 80% due to extreme weather, severely impacting growers who seek urgent government support to recover and stabilize future harvests.

- Morocco’s orange production has declined by 30% YoY this season, yet the country maintains stable exports of the Maroc Late variety to Canada, Europe, and the Middle East amid global supply disruptions.

- California projects a lower 2024/25 Valencia orange yield of 15 million cartons, down from 18.6 million, due to reduced bearing acreage and smaller average fruit size.

1. Weekly News

Australia

Australia Eyes Orange Export Growth as Production Challenges Persist

Australia’s orange industry is cautiously optimistic about export growth in 2025 despite ongoing challenges such as erratic weather, labor shortages, and limited yields in recent seasons. Moora Citrus, the largest grower in Western Australia, expects a harvest of about 10 thousand metric tons (mt) this year. Warm autumn conditions have delayed fruit maturation, with growers hoping for cooler nights to improve coloring. Export success hinges on meeting strict grading and blemish standards, especially for key markets like China, Japan, Thailand, the United States (US), Canada, and the United Arab Emirates (UAE). While the industry recalls the 2019 export peak of 304 thousand mt valued at USD 541 million, rising labor costs and climate-related risks have prompted growers to explore adaptive measures such as protective netting to improve fruit quality, water efficiency, and long-term resilience.

Mexico

Tamaulipas Orange Sector Suffers Steep Production Decline

Mexico’s orange production in Tamaulipas has plunged by up to 80% in one of the region’s worst agricultural crises, caused by prolonged droughts, frost, and hailstorms. Traditionally yielding around 800 thousand mt annually, this season’s output barely reached 160 thousand mt, disrupting livelihoods across the supply chain. Spanning November to May, the harvest delivered low yields and volatile pricing, initially peaking at USD 0.68 per kilogram (MXN 13/kg) before falling to USD 0.26 (MXN 5) or less. Despite maintaining a strong reputation for juice blending, growers urgently need government support. This includes fertilizers, modern irrigation, agricultural equipment, and improved marketing strategies to reduce dependency on middlemen and stabilize the sector for future harvests.

Morocco

Morocco’s Orange Season Sees Lower Yields but Stable Market Presence

Morocco’s ongoing orange season, focused on the Maroc Late variety harvested from April to August, remains stable in global markets. This is despite a 30% year-on-year (YoY) drop in production due to drought, pest pressures, and natural alternation in yields. With early-season disruptions from Egypt and Spain creating supply gaps, Moroccan exports have helped fill the void. This has maintained price and demand stability in key destinations like Canada, Europe, and the Middle East. Although water scarcity limits expansion, growers are optimistic for the next season, expecting improvements in fruit quality and a more balanced global market as Egyptian oversupply fades and local juice concentrate production gains traction.

United States

California Projects Lower Valencia Orange Yield for 2024/25

California’s 2024/25 Valencia orange crop is projected to decline to 15 million cartons, down from 18.6 million the previous year. The drop is primarily driven by a reduction in bearing acreage from 25.5 to 25 thousand acres, while tree density remained at 124 trees per acre. The average fruit set per tree rose 4.3% YoY to 552, but the average fruit diameter decreased by 1.7% to 2.39 inches, slightly below the five-year norm. These figures come from the California Department of Food and Agriculture’s annual Valencia Orange Objective Measurement Survey, based on Jan-25 to Feb-25 data from 301 groves across Tulare, Kern, San Diego, and Ventura counties. The results indicate tighter supply expectations for the upcoming season.

2. Weekly Pricing

Weekly Orange Pricing Important Exporters (USD/kg)

Yearly Change in Orange Pricing Important Exporters (W22 2024 to W22 2025)

* Blank spaces on the graph signify data unavailability stemming from factors like missing data, supply unavailability, or seasonality

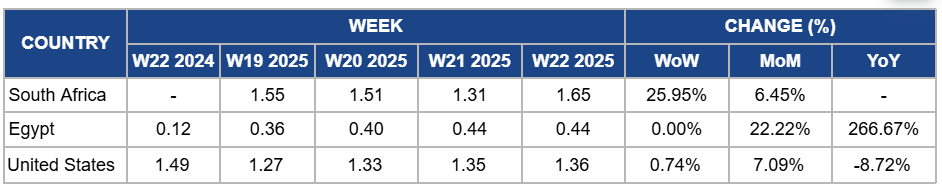

South Africa

In W22, South Africa's orange prices surged by 25.95% week-on-week (WoW) to USD 1.65/kg, with a 6.45% month-on-month (MoM) increase. This significant rise is primarily due to adverse weather conditions, including frost, hailstorms, and floods, which have reduced both the quantity and quality of citrus fruits in key production areas such as Limpopo and Citrusdal. Consequently, the Citrus Growers Association of Southern Africa (CGA) has adjusted its export forecast downward to 162.3 million 15-kg cartons, a decrease from the previous year's record of 165.1 million cartons. Additionally, the global surge in orange juice prices, driven by crop failures in Brazil and Florida, has led to increased competition from the juicing market, further tightening supply. These combined factors have led to a substantial price increase in the domestic market.

Egypt

Orange prices in Egypt remained stable WoW at USD 0.44/kg in W22, reflecting a 22.22% MoM increase and a remarkable 266.67% YoY surge. This sharp price rise is primarily due to reduced orange production caused by adverse weather conditions, including drought and unseasonal rainfall, which affected key growing regions such as Beheira and Sharkia. Additionally, increased domestic demand during the Ramadan season and export restrictions aimed at preserving local supplies have tightened availability in the market. The combination of lower supply and higher consumption pressure has driven prices significantly higher than last year.

United States

In the US, orange prices increased by 0.74% WoW to USD 1.36/kg in W22, reflecting a 7.09% MoM rise. This increase could be attributed to reduced arrivals from key growing regions, leading to a tighter local supply. However, YoY prices declined by 8.72% because of a significant drop in consumer demand, driven by high prices and diminished juice quality. Reports indicate that oranges harvested in late 2024 suffered from an unfavorable sugar/acid ratio and an excess of limonin, resulting in a bitter taste and reduced market acceptance, particularly in the US. Additionally, a bumper orange crop in Spain has flooded the market, further driving prices down. Looking ahead, global orange juice production is projected to increase in 2025, with Brazil anticipating a substantial rise in output. However, production is expected to decline in the EU and significantly in the US, creating a dynamic and volatile market.

3. Actionable Recommendations

Optimize Orchard Management to Maximize Yield Quality

Orange producers should focus on improving tree health and fruit size through targeted pruning, nutrient management, and irrigation optimization. Growers in Spain and Brazil can implement precise water scheduling and foliar feeding to boost fruit diameter despite reduced acreage. Additionally, adopting high-density planting in new orchards can offset acreage decline by increasing overall production capacity while maintaining fruit quality.

Strengthen Climate-Resilient Practices to Secure Orange Yields

Orange producers should urgently adopt climate-resilient techniques like drip irrigation, frost protection nets, and hail barriers to reduce weather damage. Growers in Brazil and South Africa have successfully integrated solar-powered irrigation and hail netting to protect orchards. Additionally, investing in direct-to-consumer marketing platforms and cooperatives can help producers improve pricing power and reduce reliance on intermediaries, stabilizing income despite yield fluctuations.

Sources: Tridge, ABC News, Citrus Industry, Freshplaza, Hoytamaulipas