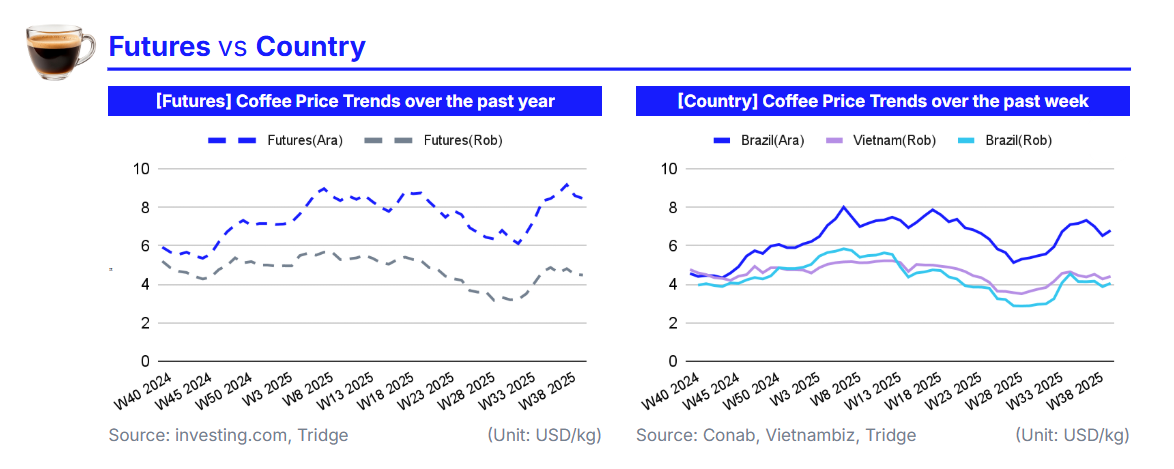

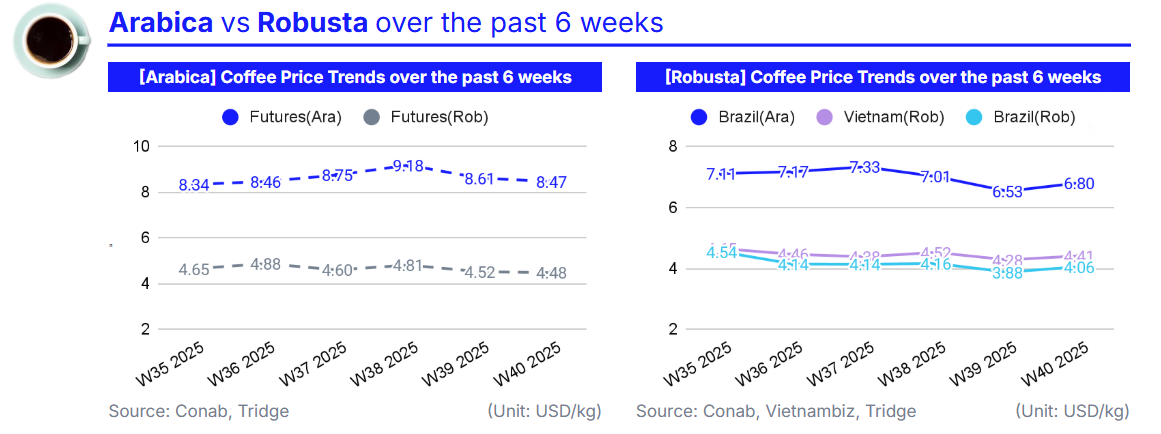

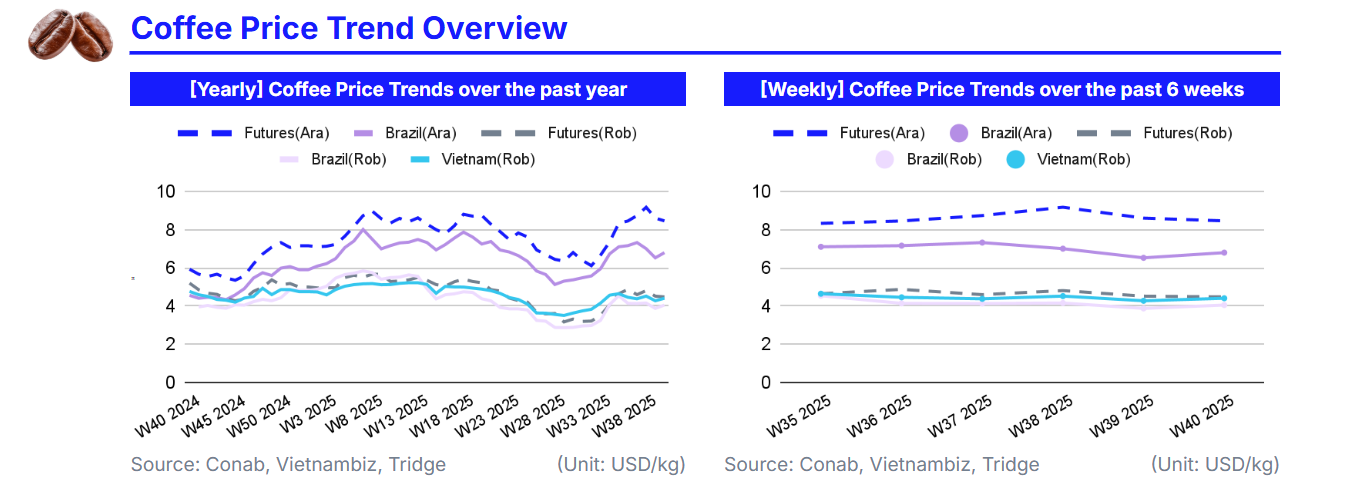

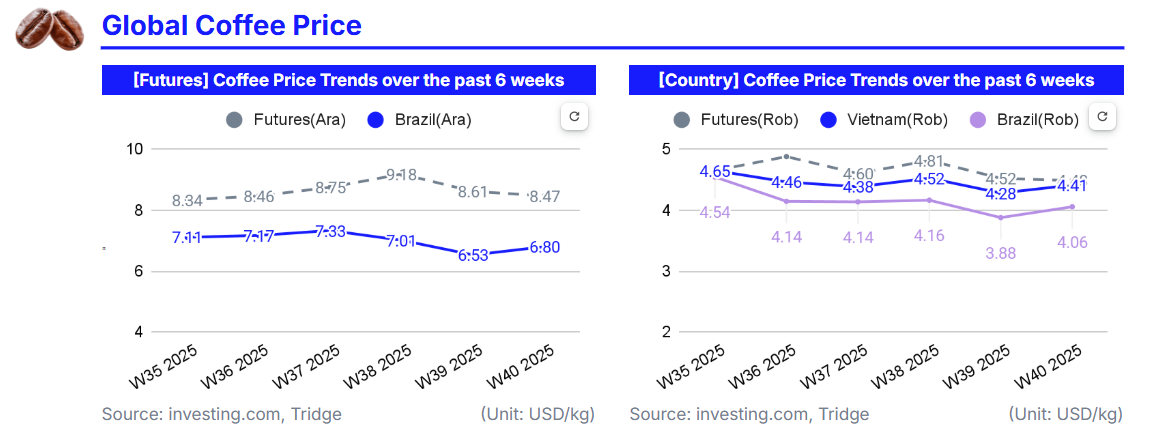

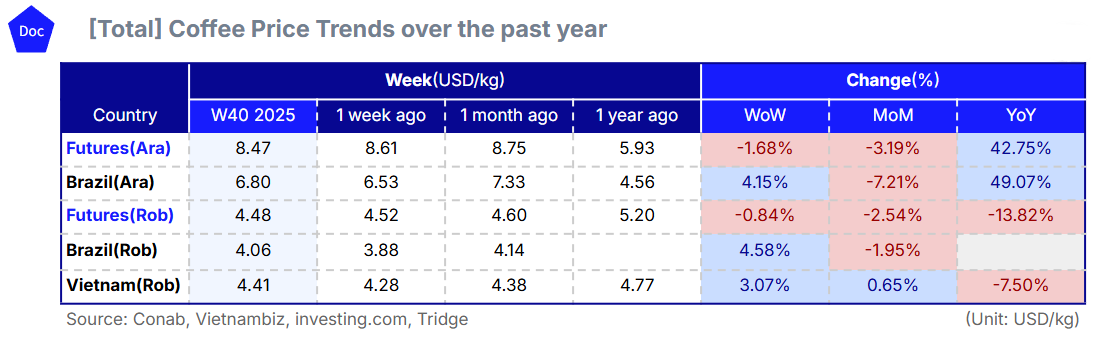

As of W40 2025, global coffee prices showed mixed movements as improved rainfall in Brazil and investor profit-taking eased previous rallies. Arabica (US Coffee C Futures) fell 1.68% week-on-week (WoW) to USD 8.47 per kilogram (kg), and Robusta (London Coffee Futures) declined 0.84% WoW to USD 4.48/kg. In Brazil, however, both Arabica and Robusta rose 4.15% and 4.58% WoW, respectively, supported by tight inventories, strong export demand, and expectations of US tariff removal. Vietnam’s Robusta increased 3.07% to USD 4.41/kg but remained 7.50% lower YoY amid stable supply and strong exports. Despite recent corrections, low certified stocks and US trade uncertainty continue to underpin market fundamentals, while Vietnam’s robust 2025/26 crop outlook of 1.76 mmt (+6% YoY) positions it as the key competitive supplier in the global Robusta segment.

1. Weekly Price Overview

Mixed Global Coffee Trends as Brazilian Prices Rebound and Vietnam Sees Moderate Gains

Driven by improved rainfall prospects in Brazil, the world’s largest coffee producer, and investor profit-taking after earlier rallies, global coffee prices showed mixed movements in W40 2025 compared to W39. The international Arabica price, represented by US Coffee C Futures, fell 1.68% WoW to USD 8.47/kg, while Robusta, represented by London Coffee Futures, declined 0.84% WoW to USD 4.48/kg amid long-position liquidations and easing weather concerns.

In Brazil, Arabica rose 4.15% WoW to USD 6.80/kg and Robusta 4.58% WoW to USD 4.06/kg. Despite a brief drop in late Sep-25, domestic prices remain supported by tight global inventories, strong export demand, and potential US tariff removal. According to Cepea, Arabica and Robusta fell 10.2% and 11.1% between September 15–22 but stayed at historically high levels.

Vietnam’s Robusta increased 3.07% WoW to USD 4.41/kg, though down 7.50% YoY amid stable supply and exports. Overall, while recent financial corrections softened international futures, low stocks, limited supply, and US trade uncertainty continue to support market fundamentals.

2. Price Analysis

Tight Global Coffee Stocks, Rising Vietnamese Supply Reshape Price Outlook

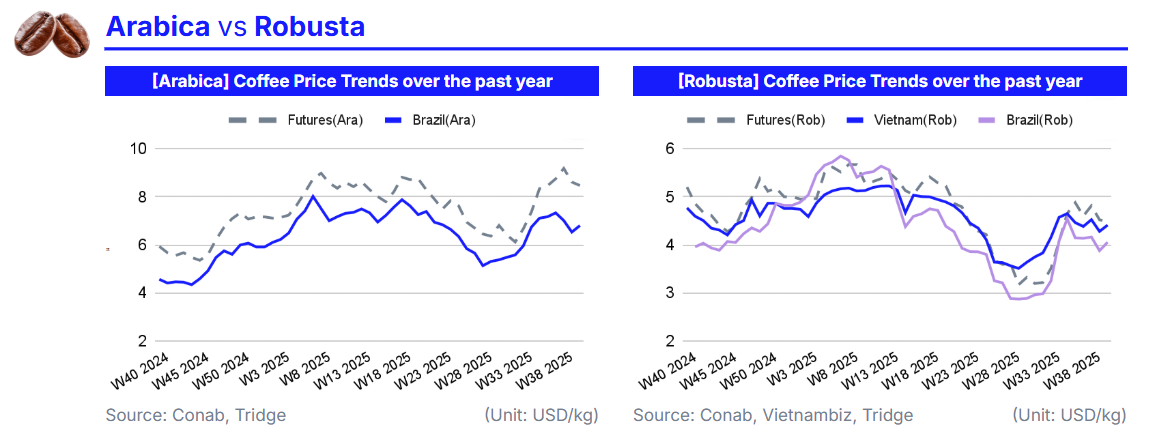

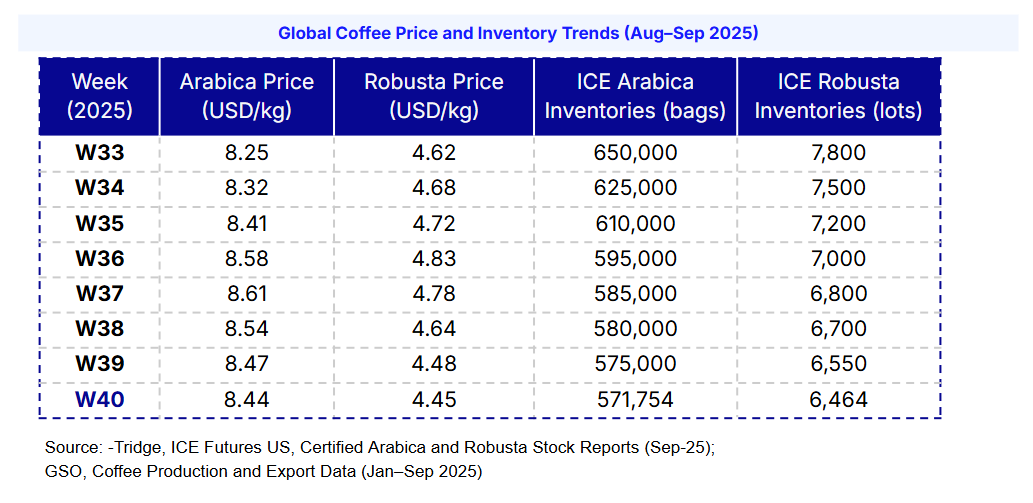

Over the past month, global coffee prices have shown mixed movements driven by a combination of supply constraints, trade policies, and weather events. Arabica prices on ICE were supported by tight inventories, which fell to a 1.5-year low of 571,754 bags, while Robusta stocks declined to a two-month low of 6,464 lots. The 50% US tariffs on Brazilian coffee have discouraged American purchases, tightening local supply and providing a short-term bullish factor for international prices.

Vietnamese Robusta also received temporary support from Typhoon Bualoi, which caused flooding and restricted farm access. However, the outlook for Vietnam’s 2025/26 crop is structurally bullish on supply, with production forecast at 1.76 mmt (+6% YoY), a four-year high. Exports in the first nine months of 2025 reached 1.23 mmt worth 6.98 billion USD, up 11.1% in volume and 61.4% in value YoY. Growth in processed coffee exports reflects Vietnam’s ongoing strategy to increase added value and strengthen its international market position.

Despite these supportive factors, global prices fell sharply in late Sep-25 due to financial market volatility following Fed rate cuts, improved supply in Vietnam and Brazil, and delayed purchases by roasters anticipating lower prices. Certified Arabica stocks in New York also declined modestly to 538,606 bags, reflecting a relatively tight supply in key consuming markets, while London Robusta positions saw a 34.2% reduction in speculative long positions, signaling caution among traders.

3. Strategic Recommendations

Vietnamese Robusta Forward Contracts Offer Strategic Advantage Amid Market Shifts

Given current price adjustments and shifting supply dynamics, coffee importers and roasters should prioritize forward contracts for Vietnamese Robusta over the coming months. Vietnam’s 2025/26 harvest is projected to rise 6% YoY to 1.76 mmt, offering stable and competitive prices compared to Brazil, where export volumes face higher costs due to US tariffs. This approach would help buyers secure a lower-cost supply ahead of potential price rebounds during the year-end demand surge.

At the same time, investment in value-added Vietnamese coffee, particularly roasted and processed varieties, could offer higher returns as the country’s export mix continues to diversify. Processed coffee exports already rose 63.5% YoY in early 2025, reflecting growing capacity and international competitiveness. Strategic partnerships with established Vietnamese processors could ensure supply consistency while aligning with rising global demand for traceable and premium-quality Robusta.

For exporters, Brazilian producers may benefit from hedging strategies to mitigate exposure to tariff-related risks and currency fluctuations. Given tight ICE inventories and volatile weather patterns, selectively locking in prices during temporary dips could preserve margins while positioning for medium-term recovery once market fundamentals reassert upward pressure.

4. Price Indicators