W24 2024: Beef Weekly Update

.jpg)

1. Weekly News

Global

FAO Meat Price Index Drops in May-24

The Food and Agriculture Organization (FAO) reported that the meat price index averaged 116.6 points in May-24, a slight 0.17% decrease from Apr-24's 116.8 points. This decline can be partly attributed to a 0.79% month-over-month (MoM) drop in the beef price index, which fell to 125 points. The decrease in beef prices was driven by sluggish import demand and ample exportable supplies from Oceania.

European Union

Mixed Trends in EU Compound Feed Production Amid Economic and Regulatory Challenges

The European Feed Manufacturers' Federation (FEFAC) projects a varied outlook for European Union (EU) compound feed production in 2024, with mixed trends across livestock sectors. The primary factors influencing this projection are economic uncertainty, regulatory changes, and ongoing environmental and animal welfare policies.

According to FEFAC, the EU's industrial compound feed production is forecasted to decline to 147 million metric tons (mmt) in 2024, a 0.3% decrease from 2023. Cattle feed production is expected to remain relatively stable, with minor growth or reductions depending on regional conditions. For instance, Ireland anticipates modest growth in cattle feed due to a delayed grazing season. In contrast, the Netherlands expects a further 5% year-on-year (YoY) decline in the dairy and beef sectors, largely attributed to persistent regulatory and environmental challenges.

New Zealand

New Zealand Drops Agricultural Emissions Pricing Plan

New Zealand has scrapped its plan to impose a price on agricultural emissions, including methane from belching sheep and cattle. This move followed pressure from farmers who argued that the plan would render their businesses unprofitable. Instead, the new government has allocated USD 245.43 million (NZD 400 million) over the next four years to expedite the commercialization of tools and technology aimed at reducing on-farm emissions. Additionally, funding for the New Zealand Agricultural Greenhouse Gas Research Centre will be increased by USD 30.99 million (NZD 50.5 million) over the next five years. The previous government had proposed a methane emissions tax for cattle owners starting at the end of 2025, which would have been a global first.

South Korea

South Korea Lifts Barriers on French and Irish Beef

South Korea has lifted trade barriers on beef exports from France and Ireland, which were imposed on 15 EU member states in 2001 due to the outbreak of bovine spongiform encephalopathy (BSE). After extensive discussions with the European Commission (EC), South Korea previously reopened its market to EU beef from Denmark and the Netherlands in 2019. This recent removal of trade restrictions signals a positive trend for future trade involvement of other EU countries and underscores the EU's commitment to maintaining stringent animal and food safety control measures. The EC anticipates that more EU member states will soon be able to export beef to South Korea, strengthening the EU-South Korea trading relationship.

2. Weekly Pricing

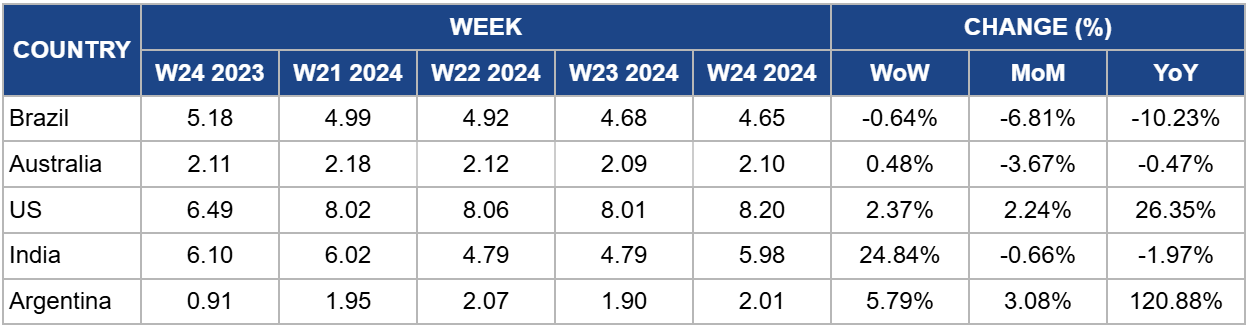

Weekly Beef Pricing Important Exporters (USD/kg)

Yearly Change in Beef Pricing Important Exporters (W24 2023 to W24 2024)

Brazil

In W24, the wholesale price of boneless rear beef in Brazil averaged USD 4.65 per kilogram (kg). This represents a 0.64% week-on-week (WoW) drop, a 6.81% MoM decrease, and an 10.23% YoY decline. Notably, the price of the Brazilian real (BRL) remained unchanged from W23 at BRL 25.00/kg, indicating that the WoW drop in USD is due to the devaluation of the real against the US dollar. Nonetheless, the YoY decline is primarily attributed to a high beef supply in the Brazilian market resulting from increased production. This surge in beef output has led to record exports. According to Safras and Mercado, Brazil's beef shipments reached 57.94 thousand metric tons (mt) in the five working days of Jun-24, a 26.3% increase compared to the same period in 2023. However, the price per ton dropped by 11.7% YoY to USD 4,460.60.

Australia

Australia's national young cattle indicator averaged USD 2.10/kg in W24. This indicates a 0.48% WoW increase but a 3.67% MoM decline. The WoW could be attributed to the short supply of prime-quality cattle and a limited number of prime-grown steers and heifers. According to Meat and Livestock Australia (MLA), the price increase was primarily observed in Queensland, where high-quality feeder steer cattle suitable for feedlot buyers drove the price increase.

United States

The average price of lean beef (92-94%) in the United States (US) reached USD 8.20/kg, a 2.37% WoW increase and a substantial 26.35% YoY rise. These price hikes are due to a reduced beef supply in the market, stemming from a decrease in US beef production caused by prolonged droughts. Kemin reported that beef supply from manufacturers is declining and is projected to average 56 pounds per capita in 2024, a 1.9% drop compared to 2023.

India

In W24, the average price of beef (cow) in India was USD 5.98/kg, a significant 24.84% WoW increase but a 0.66% MoM drop and a 1.97% YoY decline. The substantial WoW rise underscores the volatility of the Indian beef market, which has been pronounced over the past year. This volatility is mainly driven by fluctuations stemming from both domestic and international regulations.

Argentina

In W24, the average price of beef (steer) in Argentina was USD 2.01/kg, a 5.79% WoW increase, and a 3.08% MoM rise. These price increases suggest a rebound in beef demand in Argentina. However, despite this suspected demand recovery, beef consumption has remained subdued in recent months due to the challenging economic environment, leading many consumers to choose more cost-effective options like poultry.

3. Actionable Recommendations

Strengthening Trade Agreements and Market Access

Following South Korea's lifting of trade barriers on beef exports from France and Ireland, the EU should continue to negotiate the removal of similar barriers for other member states. This approach will enhance market access for EU beef producers and provide a more stable market for EU meat exports, thus reducing price volatility and supporting the livestock sector.

Investing in Sustainable Farming Practices

Considering the EU’s projected decline in compound feed production and New Zealand's focus on reducing agricultural emissions, countries should invest in advanced farming technologies that enhance productivity and sustainability. Technologies such as precision farming, efficient feed management systems, and methane-reducing feed additives can help mitigate the impacts of environmental regulations and production declines.

Strengthening Research and Development Initiatives

Other countries are recommended to follow New Zealand's example by increasing funding for agricultural research centers focused on emission reduction and sustainable farming practices. This investment will drive innovation, improve farm efficiency, and reduce environmental impacts, ensuring long-term sustainability in the agricultural sector.