1. Weekly News

Global

USDA Forecasts 2024/25 Global Corn Production and Trade Trends

According to the United States Department of United States (USDA) report for June-24, analysts have adjusted their forecasts for global corn production, exports, and ending stocks for the 2024/25 season. The world corn production forecast increased to 1.22 billion metric tons , which is up by 0.61 million metric tons (mmt) compared to the previous forecast. Likewise, the estimate for world corn exports has been raised to 191.75 mmt, an increase of 0.65 mmt. Meanwhile, the forecast for ending stocks has been reduced to 310.77 mmt, down by 1.5 mmt. Specifically for Ukraine, the USDA projects a corn harvest of 27.7 mmt, an increase of 0.7 mmt from previous estimates. Corn exports from Ukraine are forecasted to reach 24.5 mmt, up by 0.5 mmt, with ending stocks expected at 1.48 mmt. In the United States (US), the USDA has maintained its forecast for corn production at 377.4 mmt. The export estimate has been raised to 55.88 mmt, an increase of 1.27 mmt while ending stocks are projected at 53.39 mmt, unchanged from previous forecasts.

USDA Maintains Brazil Corn Production Forecast

The USDA's latest World Agricultural Supply and Demand Estimates (WASDE) report, released on June 12, maintained the corn production estimates for Brazil and Argentina for the 2024/25 season. Brazil's corn harvest forecast is unchanged at 127 mmt, consistent with previous projections. Similarly, the 2023/24 estimates were also unchanged at 122 mmt, despite earlier expectations of a slight reduction. In contrast, Argentina's corn production forecast for the 2023/24 cycle stood at 50 mmt. This figure comes amid concerns over the impact of the leafhopper plague in Argentina's primary corn-producing regions. Local entities such as the Buenos Aires Cereal Exchange (BCBA) and the Rosario Commerce Exchange (BCR) have slightly lower estimates, predicting harvests of around 46.5 to 47 mmt respectively. The USDA report underscores the stability in Brazil's corn production outlook despite market speculations while highlighting the challenges faced by Argentina due to phytosanitary issues affecting crop yields.

Ukraine

Ukraine's Corn Production and Exports Set to Decline Amidst Extreme Heat

Ukraine's corn production and exports are projected to decline in 2024 due to hot weather during the planting season, which has negatively impacted yields, according to the Ukrainian Grain Association (UGA). UGA announced at the International Grains Council (IGC)'s annual meeting that the intense heat in Apr-24 during the planting period is expected to result in lower yields. As a result, UGA forecasts that Ukraine's corn production will drop to 25.5 mmt in the 2024/25 season, down from 29.6 mmt in 2023. Corn exports are forecasted to decrease from 26 mmt to 20.5 mmt. Contrastingly, the IGC forecasts Ukraine's corn production at 27.7 mmt and exports at 20.5 mmt. Ukraine achieved a record corn production of 42.13 mmt in 2021.

Zimbabwe

Zimbabwe Corn Production Plummeted by 72% YoY in 2024 Due to Drought

Zimbabwe is facing its most severe drought in 40 years, reducing corn production drastically. According to a report from New Zimbabwe on May 9, as of May 31, the 2024 corn production stood at 634,699 metric tons (mt), marking a staggering 72% year-on-year (YoY) decline. Zimbabwe's grain mills plan to import at least 1.4 mmt of corn by July-24 to mitigate the shortage. The El Niño weather phenomenon has been a significant factor in triggering drought conditions across southern Africa. As a result, South Africa's corn production has decreased by at least 20%, and countries such as Malawi, Zambia, and Zimbabwe have declared national states of disaster due to widespread crop failures.

* Varieties: The US (feed grade), all others (overall average)

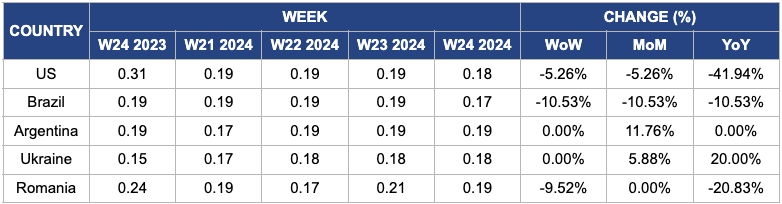

Yearly Change in Maize Pricing Important Exporters (W24 2023 to W24 2024)

* Varieties: The US (feed grade), all others (overall average)

* Blank spaces on the graph signify data unavailability stemming from factors like supply unavailability, missing data, or seasonality

US

In W24, the wholesale maize price in the US decreased week-on-week (WoW) to USD 0.18 per kilogram (kg), marking a significant year-on-year (YoY) decline of 41.94%. The drop in corn prices is due to improved overall growing conditions, which delivered above-average yields, leading to reduced planting acreage. In Texas, corn acres are projected to decrease by 16%, from 2.5 million in 2023 to 2.1 million acres. While much of the corn in southern Texas has already been planted and has emerged, growers in the High Plains and Panhandle regions are expected to begin planting soon, with sowing continuing across the US corn belt.

Brazil

In W24, the wholesale price of Brazilian maize decreased by 10.53% WoW to USD 0.19/kg but saw a YoY increase of 5.56%. Early in the month, prices experienced stress due to exchange rate volatility and weather speculation. However, the return of rain in the Safrinha maize-producing areas, which had been experiencing drought, led to an increased supply from producers, contributing to a drop in cereal prices. Moreover, consumer interest in maize remains limited due to the anticipation of a favorable harvest season. Additionally, Brazil's maize exports face competition from countries such as Argentina, limiting its participation.

Argentina

In W24, the wholesale price of Argentine maize remained unchanged week-on-week (WoW) at USD 0.19/kg. However, the month-on-month (MoM) price increased by 11.76%. Corn harvesting in Argentina has progressed to 20% of the area, with varying yield conditions reported across different regions. Despite diseases and pests impacting yields in certain areas, the Buenos Aires Grain Exchange has maintained its corn harvest forecast for the 2023/24 season.

Ukraine

Ukrainian maize prices held steady WoW at USD 0.18/kg. However, prices increased by 5.88% MoM and by 20% YoY. This price trend reflects market dynamics influenced by export figures and forecasts. As of June 3 in the 2023/24 marketing year (MY), Ukraine had exported 26.6 mmt of corn, slightly lower than the 27.1 mmt exported by the same date last year but exceeding the USDA forecast of 26 mmt for this period. There is potential to export an additional 1.5 mmt of corn by the end of the season, which is expected to significantly reduce final stocks.

Romania

In W24, maize prices in Romania decreased by 9.52% WoW and 20% year-YoY to USD 0.19/kg. Romanian maize production rose in 2023 as yields recovered following a drought-driven drop the previous year.

3. Actionable Recommendations

Monitor Weather Patterns and Adjust Risk Management Strategies

Recent droughts in Zimbabwe and heatwaves in Ukraine significantly impacted global corn production. Stakeholders must intensify monitoring of weather forecasts and adopt proactive risk management strategies. This includes leveraging hedging tools, crop insurance products, and early warning systems to mitigate potential yield losses and price volatility associated with adverse weather conditions. Such measures are crucial for safeguarding agricultural investments and ensuring stable food supply chains globally.

Diversify Supply Chains and Sourcing Strategies

With localized disruptions like Zimbabwe's drastic production decline due to drought, importers must diversify sourcing strategies. This involves exploring multiple supply sources and securing contracts early to mitigate supply chain disruptions and price fluctuations. Meanwhile, exporting countries like Brazil and Argentina should enhance logistical efficiencies to remain competitive amid currency fluctuations and weather-related challenges affecting crop yields and export capabilities.

Sources: Foodmate, UkrAgroConsult, Graintradem, Hellenic Shipping News, Foodmate