W32 2024: Beef Weekly Update

.jpg)

1. Weekly News

Global

FAO Meat Price Index Rose By 1.23% MoM in Jul-24

According to the Food and Agriculture Organization (FAO), the meat price index averaged 119.46 points in Jul-24, marking a 1.23% increase from the revised 118.01 points in Jun-24. Increases in beef, lamb, and poultry prices primarily drove this growth. FAO data indicates that the beef index rose by 1.70% month-on-month (MoM) to 126.69 points, while the lamb index grew by 3.93% MoM to 110.24 points. The increases were due to robust import demand and seasonally falling animal supplies for slaughter in Oceania. The poultry price index averaged 116.39 points in Jul-24, a 1.67% MoM rise, driven by strong import demand, especially from the Middle East and North Africa (MENA) region, amid production challenges from avian influenza outbreaks in several producing countries. Conversely, the pig meat price index dropped by 0.18% MoM to 114.78 points, attributed to an oversupply situation in Western Europe due to weaker domestic and international demand.

Brazil

Brazil’s Beef Exports Set New Record in Jul-24

According to data from the Ministry of Development, Industry, Commerce, and Services (MDIC) data, Brazil’s beef exports, including in natura, offal, processed, tripe, salted, and fat, reached a monthly record of 267.67 thousand metric tons (mt) in Jul-24, a 21.6% MoM increase. This shipment was valued at USD 1.15 billion, a 20.3% MoM rise, placing it among the top 10 highest monthly revenue in history.

This record shipment was primarily destined for China, receiving 123.4 thousand mt, valued at USD 537.68 million. Notable markets that registered significant increases include the United Arab Emirates (+18.6% MoM), the Philippines (+49.3% MoM), Russia (+67.5% MoM), and Hong Kong (+23.5% MoM). It is also worth noting that Indonesia received around 2 thousand mt in Jul-24 from Brazil, the highest value since Aug-22. The Brazilian Association of Meat Exporting Industries (ABIEC) attributes this exceptional performance to the sector's efforts to explore opportunities in existing markets and adjust its product offerings to meet demand.

Brazil’s Beef Consumption is Expected to Rise by 4% YoY in 2024

The United States Department of Agriculture (USDA) projects that beef consumption in Brazil could rise by 4% year-on-year (YoY) in 2024, driven by higher income levels and a robust domestic supply. The Brazilian Institute of Geography and Statistics (IBGE) indicates that income in the Brazilian real (BRL) increased by 2.5% from Mar-24 to May-24. The Center for Advanced Studies on Applied Economics (CEPEA) suggests that a 1% increase in income leads to a 0.7% rise in the consumption of high-quality beef. Additionally, beef consumption has been supported by lower prices for cuts, resulting from an increased cattle supply.

China

China's Meat Market is Evolving Driven by Consumer Habits

China's consumer market is rapidly evolving due to economic growth, market expansion, and digitalization. Rabobank indicates that while overall consumer spending has decreased in some categories, spending on food remains high, with consumers seeking value beyond just the product itself. In the animal protein sector, there is a growing emphasis on value for money and high-quality products, aligning with China's shift toward an experience-driven economy. Health concerns, such as obesity, are also prompting consumers to focus on balanced diets and nutrition.

China's animal protein consumption remains significant, with meat consumption at 72 kilograms (kg) per capita in 2023. However, demographic changes, including an aging population and smaller households, influence preferences, leading to a shift from pork to poultry, beef, and seafood, which are considered healthier options.

The rise of e-commerce and live streaming is reshaping distribution channels, with local restaurants, bars, and live-streaming platforms gaining popularity. Companies must adopt consumer-centric strategies to succeed in this dynamic environment, focusing on adapting to these new trends and consumer demands.

United States

US Beef Exports in Jun-24 Registered Highest Value in Nearly Two Years

The United States Meat Export Federation (USMEF) reports that United States (US) beef exports amounted to 110.16 thousand mt in Jun-24, a 4% YoY drop and the second-largest shipment in 2024. These exports were valued at USD 938.3 million, a 3% YoY increase and the highest value since Aug-22.

Japan regained its status as the most significant volume destination for US beef, with an 8% YoY shipment increase, while Canada saw a substantial 29% YoY rise in export value. Taiwan also recorded its third-highest volume on record. Meanwhile, exports to South Korea fell compared to Jun-23 but recovered compared to May-24.

2. Weekly Pricing

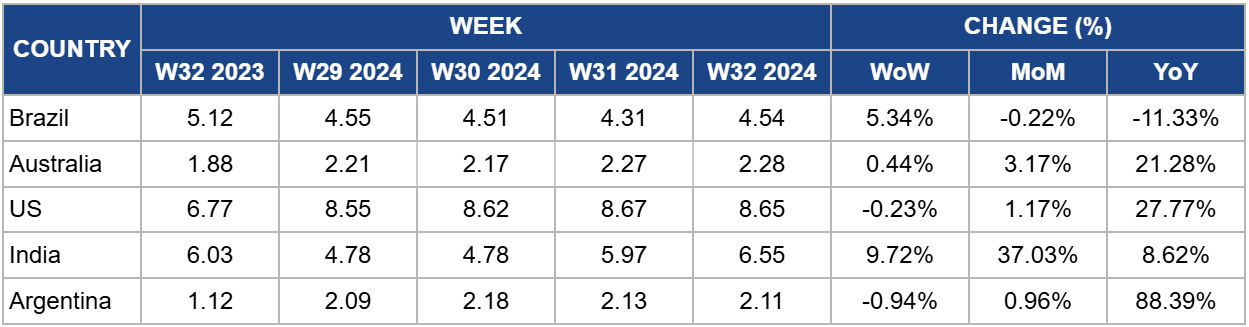

Weekly Beef Pricing Important Exporters (USD/kg)

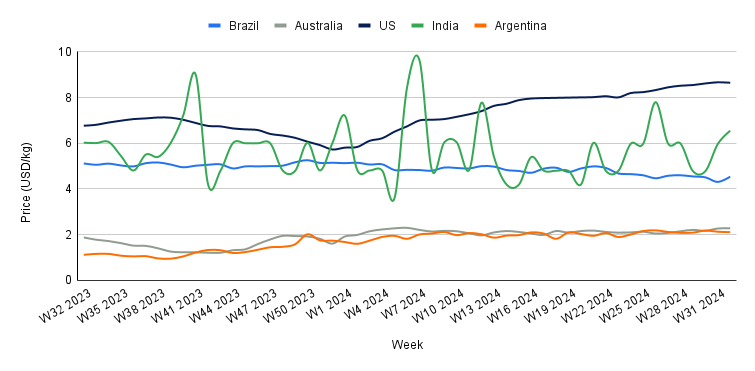

Yearly Change in Beef Pricing Important Exporters (W32 2023 to W32 2024)

Brazil

In W32, the wholesale price of boneless rear beef in Brazil averaged USD 4.54/kg, a 5.34% week-on-week (WoW) increase but a 11.33% YoY decline. The WoW increase could be attributed to an increased beef demand over the week. However, the YoY drop can be linked to an increased beef supply in the market due to higher production levels. According to the National Supply Company (CONAB), Brazil's beef production is expected to reach 10.19 million metric tons (mmt) in 2024, a 7.1% YoY increase, surpassing the previous record set in 2006. This growth is driven by the livestock cycle nearing its peak, particularly with an anticipated rise in female cattle slaughter. As a result, CONAB projects domestic beef availability will increase by 4.2% YoY, reaching 6.82 mmt.

Australia

Australia's national young cattle indicator averaged USD 2.28/kg in W32, a 0.44% WoW rise, a 3.17% MoM growth, and a 21.28% YoY increase. Despite this weekly gain in USD terms, the average price in Australian dollars (AUD) was AUD 3.47/kg, a 0.29% decline from the previous week. The varying WoW shifts are likely due to fluctuations in the AUD-USD exchange rate. The weekly decrease in AUD prices can be attributed to increased cattle supply. According to Meat and Livestock Australia (MLA), cattle yardings rose 7% WoW, reaching 66.56 thousand heads, with Roma recording the highest throughput of 11.19 thousand heads since Apr-19. Additionally, concerns over the cattle quality contributed to the price drop across all states, except for Victoria and Western Australia.

United States

In W32, the average price of lean beef (92% to 94% lean) in the US was USD 8.65/kg, showing a slight 0.23% WoW decline but a significant 27.77% YoY increase. Despite the weekly drop, prices remain at record highs. The substantial YoY rise is primarily driven by a reduced beef supply in the market, mainly due to a decline in US beef production caused by herd shrinkage. In Q2-2024, the slaughter of cows and bulls averaged 16% lower than in the same period in 2023 and nearly 30% below levels from two years ago.

India

The average price of cow beef in India reached USD 6.55/kg in W32, marking a 9.72% WoW increase and an 8.62% YoY rise. These price increases highlight the ongoing volatility in the Indian beef market, which has been particularly evident over the past year. This instability is primarily driven by domestic and international regulations, and fluctuations in supply within the Indian market.

Argentina

In W32, the average price of steer beef in Argentina was USD 2.11/kg, a 0.94% WoW decline. This price reduction is likely due to weakened demand in the country, as beef consumption has hit its lowest levels amid a challenging economic environment. According to the Chamber of the Meat and Cattle Industry and Commerce (CICCRA), per capita beef consumption in Jun-24 was 48.0 kg, a 10.4% drop from the previous year. Additionally, the average per capita consumption for the first half of 2024 was 44.7 kg, representing a 16.7% decrease compared to the same period in 2023. As a result, many consumers have shifted to more affordable options like poultry.

3. Actionable Recommendations

Strengthening and Diversifying Export Markets Amid Record Beef Shipments

With Brazil’s beef exports reaching record highs in Jul-24, exporters must diversify their market base further. While China remains the largest market, continued efforts should be made to increase market share in growing regions like the UAE, the Philippines, and Russia. Additionally, strategic investments in marketing and distribution channels in Indonesia, which showed the highest import volume since Aug-22, could yield long-term benefits. Expanding product offerings tailored to the tastes and needs of these emerging markets will help mitigate risks associated with over-reliance on particular destinations.

Leveraging Growing Domestic Consumption for Premium Beef Products

The anticipated 4% YoY increase in beef consumption in Brazil presents an opportunity for domestic producers to capitalize on the rising demand for high-quality products. Producers can maximize profit margins by focusing on premium cuts and products that cater to consumers with increased purchasing power. Marketing strategies should emphasize premium beef's quality and nutritional benefits, especially as lower beef prices and increased income levels make these products more accessible. Collaboration with retailers to highlight these premium products in supermarkets and online platforms can drive higher sales.

Adapting to Shifting Consumer Preferences in the Evolving Meat Market

In response to China's evolving consumer habits, meat producers and suppliers should focus on offering products that align with the growing demand for healthier, high-quality, and value-for-money options. Expanding into poultry, beef, and seafood, which are gaining popularity due to health concerns, will be critical. Additionally, leveraging e-commerce and live-streaming platforms to reach consumers directly can enhance brand visibility and market penetration. Partnerships with local restaurants and bars, and influencer collaborations on live-streaming platforms can further drive consumer engagement and loyalty.

Sources: Agromeat, Portal de Campo, Canal Rural, The Cattle Site, Agropopular,