1. Weekly News

Global

Global Corn Production Expected to Slightly Decrease in 2024/25

Global corn production is expected to slightly decrease to 1.219 billion metric tons (mt) in 2024/25 from 1.22 billion mt in the 2023/24 harvest. In Brazil, corn production is projected to increase by 4% year-on-year (YoY), reaching 127 million metric tons (mmt), while the United States (US) output is anticipated to remain stable at around 384.7 mmt. Despite favorable weather conditions and a larger planting area, US soybean prices are expected to remain below the historical average. This is due to a persistently high exchange rate and the cooling of the Pacific Ocean due to the El Niño Southern Oscillation (ENSO) phenomenon. Globally, rising soybean and corn stocks over the next two harvests are expected to exert downward pressure on prices.

Europe

EU Corn Production Set to Decline in 2024 Due to Eastern Europe's Heatwave Impact

The 2024 corn production in the European Union (EU) is estimated to decrease primarily due to continuous heat waves reducing yields in Eastern Europe. The European Commission's (EC) updated estimates indicate that average yields across the EU in 2024 are expected to be 6% YoY lower. In particular, Romania is projected to experience a significant yield decline, with an 18% YoY drop from 2023 levels and a 22% reduction compared to the five-year average from 2019 to 2023. Due to adverse weather conditions, similar yield decreases are anticipated in Bulgaria, with a 16% YoY decline, and Greece, with a 10% YoY decline. The United States Department of Agriculture (USDA) forecasts Romania's corn production for the 2024/25 marketing season at 8.7 mmt, down 25% from the five-year average. The second-largest corn cultivation area in the EU after France, Romania faces challenges due to inadequate irrigation and vulnerability to extreme temperatures and drought in the Balkan region during summer.

Brazil

Brazil's 2024 Second Corn Harvest Nears Completion

As of August 23, 2024, the second corn harvest in the Center-South of Brazil has reached 98.2% of the estimated 14.711 million hectares (ha). By state, the harvest completion rates are: Paraná at 99.2%, São Paulo at 89%, Mato Grosso do Sul and Mato Grosso at 100%, Goiás at 99.1%, and Minas Gerais at 75.4%. This marks a significant improvement compared to the same period last year when the harvest covered 86.2% of the 15.468 million ha. The five-year average for this period stands at 70.7%. In the Matopiba region, which includes Tocantins, Bahia, Maranhão, and Piauí, the second crop harvest has reached 95.2% of the 1.184 million ha cultivated, with Tocantins and Bahia completing their harvests, Maranhão at 89.3%, and Piauí at 98.4%. This performance is also superior to last year, when the harvest reached 90.7% of the 1.334 million ha, with a five-year average of 91.7%.

Bulgaria

Bulgaria's Corn Production Forecast to Hit Decade Low in 2024 Due to Severe Drought

According to the USDA, Bulgaria is projected to produce its smallest corn crop in over a decade due to severe drought. The 2024/25 maize production is expected to drop to 2.2 mmt from 2.45 mmt in 2023/24, with the planted area estimated at 484,000 ha, a 9% YoY decrease. This marks the third consecutive year of significantly below-average maize yields, which could influence future planting decisions. With over 90% of Bulgaria's corn being non-irrigated and slow progress in new investments, the country's maize production outlook remains challenging. Additionally, the 2023/24 maize exports, as of August 9, were reported at 693 thousand mt, primarily to non-EU countries, down from 950 thousand mt during the same period the previous year.

Paraguay

High Input Costs and Disease Threaten Corn Production in Paraguay

Paraguay's corn production is facing significant challenges that threaten its economic viability. High input costs and frequent, costly fumigations to combat diseases and pests like leafhopper are among the primary concerns. The president of the Association of Planters/Growers of Soybean, Grains, and Oilseeds (APS) highlighted the substantial risks involved in corn production, noting that achieving the necessary high yields to cover costs is becoming increasingly difficult. Many producers might not continue investing in corn, given the slim profit margins and high yield requirements with over 5,500 kilograms (kg) per ha needed to break even. Due to these financial and management challenges, many farmers may opt for more viable alternatives rather than risking corn production.

2. Weekly Pricing

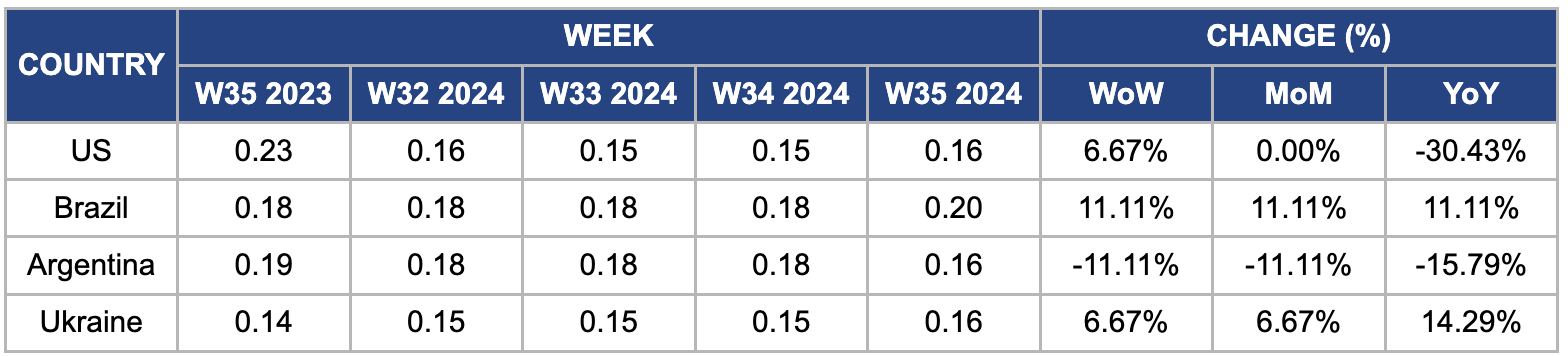

Weekly Maize Pricing Important Exporters (USD/kg)

Yearly Change in Maize Pricing Important Exporters (W35 2023 to W35 2024)

United States

In W35, wholesale maize prices in the US rose by 6.67% week-on-week (WoW) to USD 0.16/kg, driven by increased demand following new export sales announced by the USDA and significant purchases by China and Colombia. The USDA reported weekly export sales of US 2024/25 corn at 1.49 mmt, surpassing trade expectations. However, prices have fallen 30.43% YoY due to the USDA's upward revision of corn production estimates to 384.74 mmt, potentially the third-largest in US history. Despite these favorable production conditions, US weekly corn sales for the upcoming campaign have exceeded market expectations, indicating future solid demand.

Brazil

In W35, wholesale maize prices in Brazil rose by 11.11% WoW to USD 0.20/kg from USD 0.18/kg. Brazil's continued currency devaluation primarily drives this increase. Although the second corn crop harvest is nearly complete, domestic prices rose in early Sept-24 despite the larger supply. The late-month boost is due to the absence of many sellers from the market, who are holding off due to strong international demand, rising corn prices abroad, and the appreciating dollar, which pushes up port values.

Argentina

The wholesale price of Argentine corn decreased by 11.11% WoW and month-on-month (MoM) to USD 0.16/kg, marking a 15.79% decline YoY from USD 0.18/kg in the same week of 2023. This drop is mainly due to expectations of high supply for the 2024 season. The Rosario Grains Exchange anticipates a significant increase in the 2024 corn harvest, projecting a 36% to 49% rise YoY, reaching 49 mmt. Despite a 34% surge in corn exports in the first half of the season, the export value only increased by 5% YoY to USD 4.07 billion due to the lower prices.

Ukraine

The wholesale price of Ukrainian maize increased 6.67% WoW and MoM, reaching USD 0.16/kg, and saw a 14% rise YoY. This price surge is due to concerns over a severe heat wave in Jul-24, which is expected to impact Ukraine's corn production significantly. The Ukrainian Grain Association (UGA) forecasts a corn harvest of 23.4 mmt for 2024, a notable decrease from 29.6 mmt in 2023. This reduction, potentially as high as 30% YoY in affected regions, could drive prices up in the coming weeks. Despite these challenges, the Ukrainian government remains cautiously optimistic, with the acting finance minister projecting a more moderate 15% decline in late crop yields.

3. Actionable Recommendations

Mitigate Risks and Improve Production Practices in Paraguay

Paraguay should address the challenges facing its corn production by focusing on cost management and farming practices. Implementing cost-efficient farming practices and integrated pest management strategies will help reduce input costs and manage pests effectively. Promoting financial risk management tools, such as crop insurance and futures contracts, will stabilize income and support continued investment in corn production. Investing in research and development to improve farming practices and achieve higher yields, along with providing farmers with training and resources, will help increase productivity and address the challenges of high input costs.

Enhance Ukraine's Corn Production and Weather Resilience

Ukraine must address weather-related challenges by adopting climate-resilient farming practices and improving its corn production stability. Investing in research to develop drought-resistant corn varieties, such as Pioneer’s P1197AM and Dekalb’s DKC 62-08, will significantly enhance crop resilience. Implementing climate-smart agriculture practices, including conservation tillage and soil moisture management, can further bolster crop stability. Strengthening irrigation systems and upgrading infrastructure are crucial for mitigating the impact of extreme weather and ensuring consistent production levels. Utilizing market intelligence to adjust production strategies based on weather patterns and global demand trends will help Ukraine manage fluctuations in corn prices and maintain market stability.

Optimize Brazil's Corn Production and Export Management

Brazil should upgrade its storage and logistics infrastructure to address its corn production and export challenges. Investing in modern storage facilities and improving transportation networks will enhance the efficiency of corn exports and help manage production levels. Brazil should also diversify its export markets by exploring new opportunities beyond traditional buyers like China, targeting emerging Southeast Asian and African regions, such as Indonesia and Kenya. Strengthening trade relations through collaborations with trade organizations and participating in international trade fairs will help Brazil secure a stable export market for its corn and address production challenges more effectively.

Sources: Tridge, Elagro, Portal Do Agronegócio, Agri, Agrotypos, UkrAgroConsult, Hellenic Shipping News, NoticiasAgricolas, Successful Farming