1. Weekly News

Brazil

Brazilian Corn Exports Forecasted to Decline YoY in Sep-24

The National Association of Cereal Exporters (ANEC) has revised its forecast for Brazilian corn exports for Sep-24, up to the 28th, at 6.68 million metric tons (mmt), consistent with earlier projections. However, this marks a notable decrease of around 2.7 mmt compared to the 9.43 mmt exported in Sep-23. In W39, corn shipments reached 1.695 mmt, and the expected volume for W40 is 1.768 mmt, reflecting steady weekly exports despite the yearly decline.

Brazil's Corn Export Forecasted at 4.44 MMT for Oct-24

Brazil's shipment schedules indicate an export of 4.44 mmt of corn in Oct-24. However, as of October 1, no shipments have been recorded for the new month. Meanwhile, the projected exports for Nov-24 are significantly lower, at 68.1 thousand metric tons (mt). Between Feb-24 and Jan-25, total corn shipments are expected to reach 24.86 mmt.

Croatia

Croatia's 2024 Maize Production Forecasted to Decline to 1.647 MMT

Croatia forecasts to produce approximately 1.65 mmt of maize in 2024, a decline of 17.09% year-on-year (YoY) from the 1.99 mmt harvested in 2023. These estimates reflect significant shifts in crop production dynamics within the country.

Paraguay

Paraguay Faces Potential Corn Shortage, Impacting Key Agricultural Sectors

The president of the Paraguayan Association of Pig Producers (APPC) warned that a potential corn shortage could pose significant challenges for sectors reliant on the grain. Driven by diseases and adverse weather conditions, the possible decline in corn production in 2024, would lead to higher costs for industries that depend heavily on corn as a critical input. While some producers grow their corn and are less affected by market fluctuations, most rely on market-supplied corn, making this issue critical. Hence, government intervention is needed, proposing incentives to encourage stable corn production or regulations mandating that a percentage of the corn supply be reserved for domestic use.

Russia

Russia’s Corn Exports Grow Despite Forecasted Decline in 2024 Harvest

In the first eight months of 2024, Russia exported over 5 mmt of corn, reflecting a 7% YoY increase. The main buyers of Russian corn were Iran with 47%, Turkey with 31%, and Libya with 4%. In 2023, Russia ranked fifth globally in corn exports, totaling 7.3 mmt. This year, Russia dedicated 3.99 million hectares (ha) to grain cultivation, with 2.62 million ha allocated for corn production, concentrated mainly in Central Russia and the Southern and North Caucasian federal districts. Key production areas include the Krasnodar Krai, Tambov, and Voronezh regions. Russia’s corn exports could exceed 8.7 mmt by 2030. However, the Institute for Agricultural Market Research (IKAR) has cautioned that a reduced corn harvest in 2024 will limit export potential. Analysts forecast this year’s corn harvest to be between 11.8 and 12.4 mmt, the lowest level since 2018.

2. Weekly Pricing

Weekly Maize Pricing Important Exporters (USD/kg)

Yearly Change in Maize Pricing Important Exporters (W40 2023 to W40 2024)

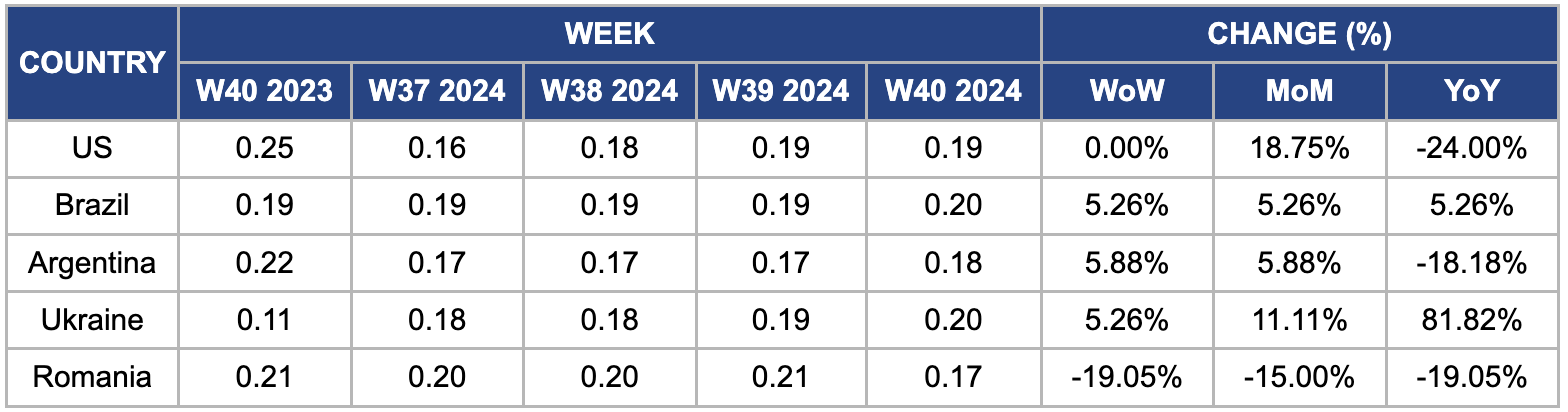

United States

In W40, wholesale maize prices in the United States (US) remained unchanged week-on-week (WoW) but rose 18.75% month-on-month (MoM), reaching USD 0.19 per kilogram (kg). Key issues impacting the market include potential labor strikes at Gulf of Mexico ports, threatening to disrupt the agricultural supply chain and affect half of the country's ocean trade. Furthermore, low water levels on the Mississippi River are causing shipping delays and increased costs. Despite these challenges, prices are 24% lower YoY, mainly due to the United States Department of Agriculture's (USDA) upward revision of corn production and yield forecasts, estimating output at 15.186 billion bushels and an average yield of 183.6 bushels per acre, both higher than previous estimates. This improved production outlook contributes to a more favorable supply scenario, significantly impacting the YoY price decline.

Brazil

In W40, wholesale maize prices in Brazil increased by 5.26% WoW, MoM, and YoY, reaching USD 0.20/kg. Despite the near completion of the second corn crop harvest and a higher overall supply, domestic prices rose in Sep-24 due to the notable absence of many sellers from the market. This situation was influenced by the solid international demand, rising corn prices abroad, and the appreciation of the US dollar, which elevated port values. Consequently, Brazilian buyers faced challenges in purchasing corn batches, even though some farmers had previously been willing to lower their asking prices in early September due to storage constraints and cash flow needs.

Argentina

The wholesale price of Argentine corn increased by 5.88% WoW and MoM, reaching USD 0.18/kg in W40. This price rise is due to concerns growing that a leafhopper plague, similar to the one that devastated the previous corn harvest, could affect fields again, potentially resulting in an estimated 2 million ha of corn being left unplanted, with a significant portion expected to be shifted to soybeans. This situation has delayed input sales and lowered planting expectations, leading to an anticipated production shortfall of approximately 21% YoY, with the total planted area projected to decrease to around 8 ha.

Ukraine

Ukrainian wholesale maize prices rose by 5.26% WoW, 11.11% MoM, and 81.82% YoY, reaching USD 0.20/kg. According to the Ukrainian Agrarian Council (UAC), this price increase is due to solid demand from exporters. Contrary to market expectations, the anticipated influx of new corn from Argentina did not alleviate demand or lower prices for Ukrainian grain. The UAC highlighted that China has been actively contracting Ukrainian corn, with significant purchases from other importers like Turkey, Egypt, Italy, and Spain. European traders reported that Chinese importers acquired at least 65 thousand mt of animal feed corn from Ukraine.

Romania

In W40, Romanian maize wholesale prices decreased by 19.05% WoW to USD 0.17/kg, down from USD 0.21/kg. Prices also declined 15% MoM and 19.05% YoY. Despite this price drop, Romania, as Europe’s second-largest grain exporter, is facing a significant reduction in corn harvests due to one of the worst droughts in decades. Nearly 2 million ha of farmland are affected, and corn output is expected to decline by 10 to 15% in the upcoming Oct-24 to Sep-25 season, raising concerns about tighter supply and market disruptions.

3. Actionable Recommendations

Implement Risk Mitigation Strategies

Brazilian corn producers should adopt comprehensive risk mitigation strategies to address export volume and pricing fluctuations. This could include developing hedging practices through futures contracts and exploring insurance products that protect against price drops and unforeseen yield losses. Engaging in risk-sharing agreements with exporters can enhance producers' stability, particularly in light of the recent declines in export forecasts. By creating a buffer against market volatility, Brazilian farmers can ensure a more predictable income stream, encouraging sustained production levels despite external pressures.

Enhance Crop Disease Management

Given the imminent threat of a leafhopper plague potentially impacting maize yields, Argentine producers should prioritize integrated pest management (IPM) strategies to protect their crops. This can include routine monitoring for pest populations through weekly scouting and yellow sticky traps to track leafhopper movement. Farmers should also introduce natural predators, such as spiders and predatory beetles, alongside microbial insecticides like Bacillus thuringiensis (Bt) to manage pest populations sustainably. Moreover, employing genetically resistant maize varieties can significantly reduce damage while strengthening collaboration with agricultural extension services and enhancing farmers’ knowledge of effective pest management practices. Establishing community-based action plans through farmer cooperatives can further support resource sharing and coordinated responses to outbreaks. By implementing these IPM strategies, Argentine farmers can effectively safeguard their production and maintain competitiveness in both domestic and international markets.

Invest in Weather-Resilient Practices

To address corn production fluctuations, Russia should invest in weather-resilient agricultural practices to protect yields from climate variability. This strategy includes promoting drought-resistant corn varieties through partnerships with agricultural research institutions to develop and distribute these seeds to farmers. Moreover, implementing advanced irrigation techniques, such as drip irrigation, will ensure a consistent water supply during dry spells. Investing in data-driven forecasting systems can provide farmers with timely weather updates, enabling them to adjust planting schedules accordingly. By prioritizing these practices, Russia can stabilize its corn production, which is vital for meeting domestic and export demands amid increasing global competition, particularly from significant importers like Iran, Turkey, and Libya, who rely on Russian corn for animal feed and food production. As competition grows from other significant exporters such as Brazil and Ukraine, Russia must ensure reliable supply chains to maintain its market share.

Sources: Tridge, Vinanet, UkrAgroConsult, PortalDBO, Elagro, Successful Farming, Portal Do Agronegócio