W41 2025: Cheese

In W41, global cheddar markets showed mixed performance, with EU prices easing slightly in USD terms due to currency effects but remaining strong YoY, while US prices continued to decline amid high inventories and weak foodservice demand. However, Oceania showed signs of stabilization, supported by rising Asian demand and tighter supply conditions. With EU milk production still running above last year and US exporters losing competitiveness due to falling European prices, the market is expected to move sideways in the near term, with potential downward pressure by Dec-25. Against this backdrop, suppliers are recommended to focus on forward contracting, value-added formats, niche export channels, and strengthened demand partnerships in Asia and emerging markets to manage inventory risks and protect margins.

Cheese Price Forecasting

1. Weekly Price Overview

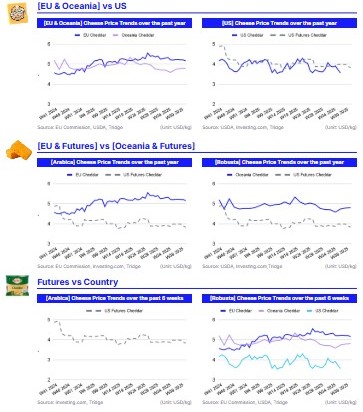

Oceania Cheddar Finds Stability as EU and US Face Downward Pressure

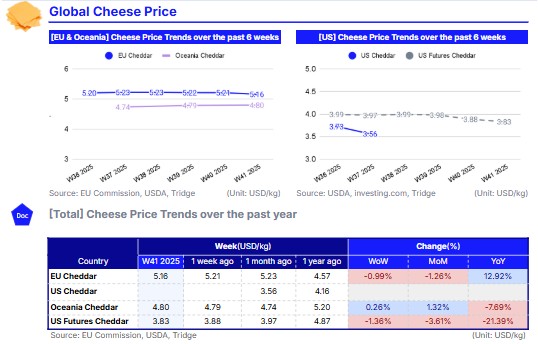

In W41, European Union (EU) cheddar cheese prices averaged USD 5.16 per kilogram (kg), representing a 0.99% week-on-week (WoW) decline but remaining 12.92% higher year-on-year (YoY). While prices fell in USD terms, they held steady at EUR 4.44/kg WoW, highlighting the impact of currency movements rather than a fundamental market shift. The 1.26% month-on-month (MoM) decrease suggests that ample supply is struggling to meet sufficient demand in both domestic and export channels. In the United States (US), cheddar futures averaged USD 3.83/kg, down 1.36% WoW, 3.61% MoM, and a significant 21.39% YoY. The decline reflects high stock levels and a bearish sentiment, with processors focusing on clearing existing inventories rather than actively competing for spot volumes. According to United States Department of Agriculture (USDA) data, domestic cheese consumption remains steady, but foodservice demand is still 8% below pre-2020 levels. While retail channels are absorbing some of the excess, they are not fully compensating for the shortfall.

On the contrary, Oceania’s cheddar market averaged USD 4.80/kg, a 0.26% WoW increase and a 1.32% MoM rise, though still 7.69% lower YoY. The region appears to be entering a stabilization phase, where rising demand is helping to curb further price declines despite growing supply availability.

2. Price Analysis

Global Dairy Market Softens as EU Supply Rises and Demand Plateaus

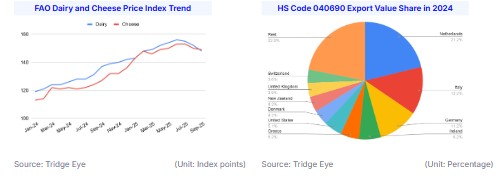

According to the Food and Agriculture Organization (FAO), the global dairy price index averaged 148.26 points in Sep-25, a 2.63% MoM decline. The cheese price index also eased by 0.59% MoM to 149.19 points, driven by price easing in the EU, where steady milk output and softer export interest weighed on the market. However, this was partially offset by firmer prices in Oceania, where smaller early-season milk supplies and stronger demand from Asian buyers supported New Zealand cheddar prices. At the Global Dairy Trade (GDT) auction on October 7, cheddar rose 0.8% to USD 4,858 per metric ton (mt), making it the only product to record gains across all contract periods, while mozzarella fell 11.8% to USD 3,393/mt.

In Europe, milk production continues to exceed last year’s levels, particularly in Ireland, Germany, Poland, and Austria. Domestic consumption in Germany remains solid, while export demand is showing gradual improvement, especially for cheese and whey products. Recent price declines have restored Europe’s competitiveness in global trade. However, prices are expected to trend sideways in the near term, with downward pressure likely from Dec-25 onward, depending on global market movements.

In the US, domestic cheese demand is steady but largely flat, with retail channels maintaining consistent interest. Export sales remain the stronger outlet, although declining European prices are eroding the US advantage in international markets. In Oceania, milk production remains firm, supported by ample milkfat availability. While domestic demand softened slightly during the period, export interest strengthened, helping to stabilize.

3. Strategic Recommendations

Strategic Export and Channel Realignment for Cheddar Market Players

Given the current global cheddar market dynamics, market participants should adopt a demand-driven and efficiency-focused strategy. EU producers and exporters should capitalize on their renewed price competitiveness by securing forward contracts with Middle Eastern, North African, and Southeast Asian buyers before the anticipated downward pressure from Dec-25 sets in. Strengthening value-added product lines such as shredded, sliced, and foodservice-ready cheddar formats for retail and quick-service restaurant segments could help absorb excess supply and sustain margins even in a sideways price environment. US suppliers, facing high inventories and increased competition, should explore bundled export offerings and logistics incentives to retain presence in key markets like South Korea, Japan, and Mexico, while targeting niche demand channels such as private-label contracts and processed cheese inputs for ready-meal manufacturers. Meanwhile, Oceania exporters should leverage current Asian demand momentum to lock in multi-shipment agreements, particularly with China, Malaysia, and the Philippines, where importers are showing preference for competitively priced New Zealand cheddar over US-origin supplies.

4. Price Indicators