W41 2025: Sugar

As of W41 2025, Brazil's sugar prices continued their downward trajectory, reflecting oversupply in the market despite strong export performance. In Oct-25, domestic sugar prices averaged USD 400.40/mt, a 15.7% decline YoY, despite a 32.8% increase in export volumes compared to Oct-24. This price drop is attributed to a steady supply, with mills increasing the proportion of sugarcane allocated to sugar production despite weaker sucrose content. Strong international demand, particularly for VHP sugar, has led to a surge in exports, with 1.8 mmt shipped in the first half of Oct-25 alone.

The global sugar market faces a projected surplus of 4.1 mmt for the 2025/26 season, further pressuring prices. As a result, Brazil's sugar market remains oversupplied, and prices are expected to stay stable to lower in the short term. Exporters can leverage this opportunity to secure competitively priced sugar, particularly as shipping activity remains high at key ports such as Santos.

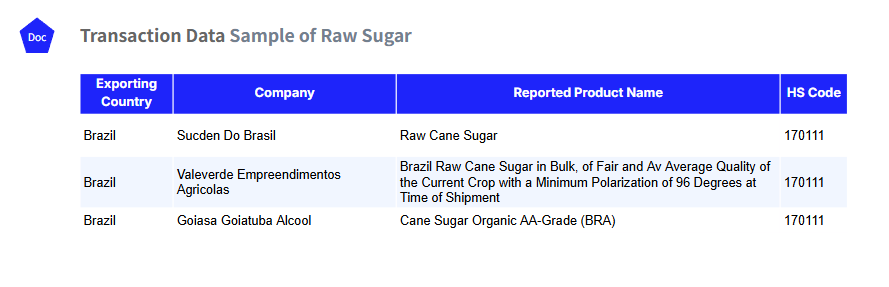

Importers should consider locking in forward contracts now to benefit from lower prices. Key Brazilian exporters such as Sucden Do Brasil, Valeverde Empreendimentos Agrícolas, and Goiasa Goiatuba Álcool are well-positioned to provide raw and organic sugar grades. Buyers across Asia, the Middle East, and Africa should act swiftly to secure supply before potential logistical disruptions or adverse weather conditions disrupt the upcoming crush.

1. Weekly Price Overview

Global Sugar Prices Mixed as Brazilian Supply Pressures Contrast with Asian Import Demand

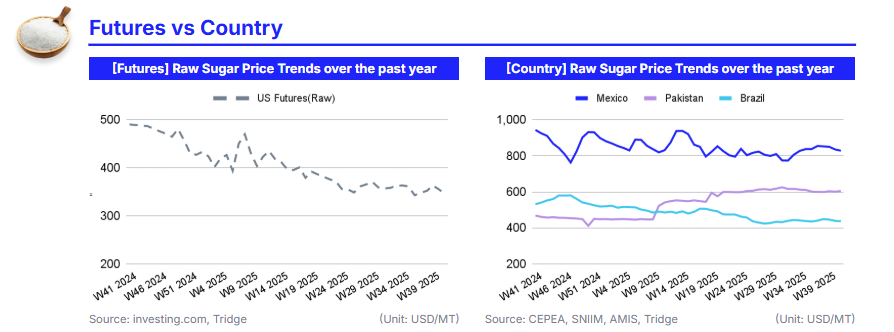

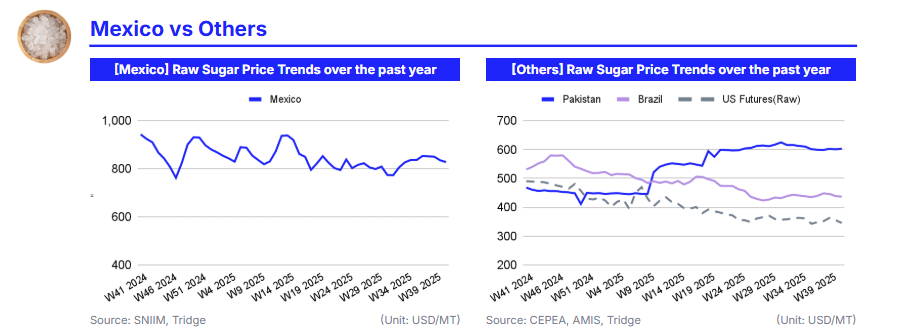

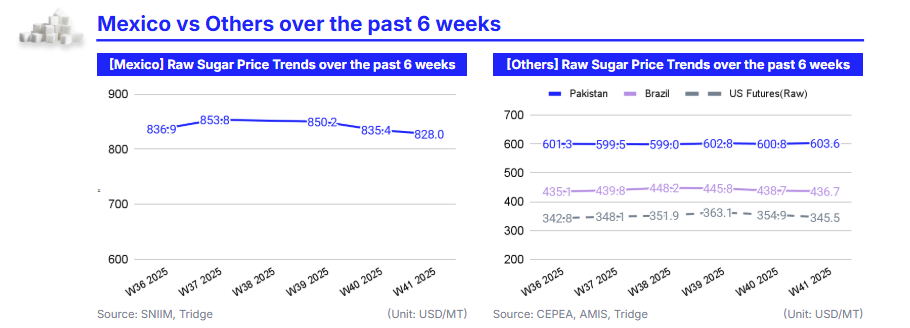

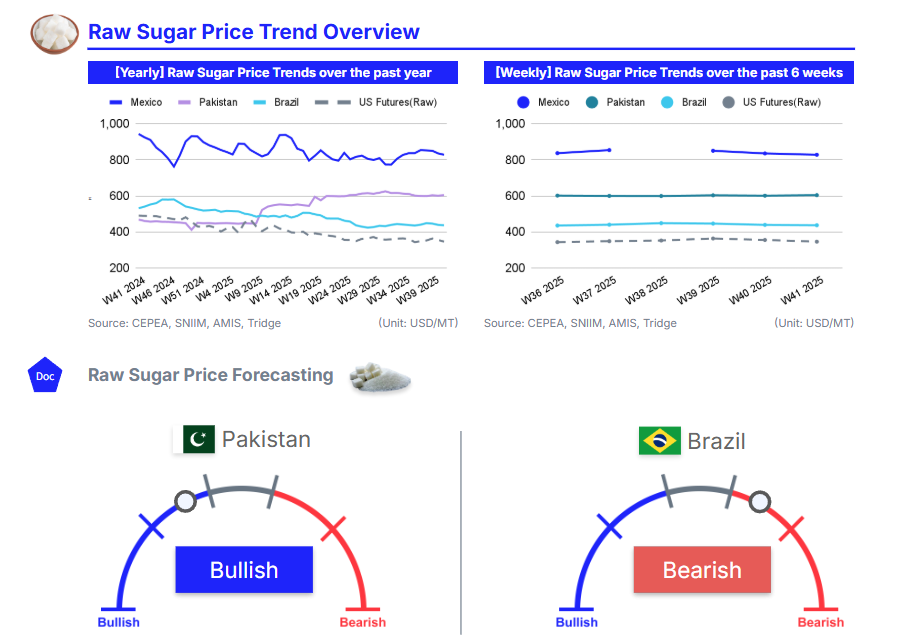

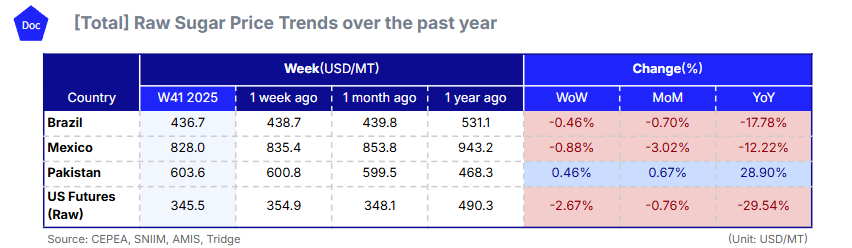

In W41, global sugar prices showed mixed movements driven by varying supply conditions and trade dynamics. Brazil’s sugar prices fell slightly by 0.46% week-on-week (WoW) to USD 436.7 per metric ton (mt), a 17.78% decline YoY from USD 531.1/mt. The price drop stems from a steady supply despite weaker sugarcane quality. The the Brazilian Sugarcane Industry Association (UNICA) reported lower sucrose content at 154.58 kg/mt, but mills increased sugar allocation to 53.49%, sustaining production and limiting price support.

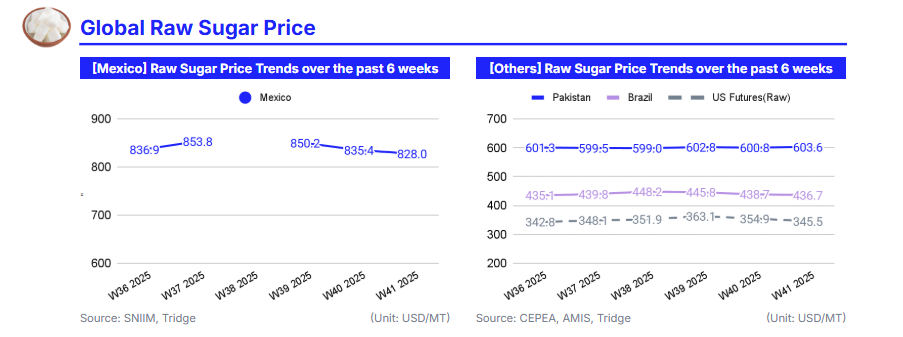

In Mexico, domestic sugar prices declined by 0.88% WoW to USD 828/mt, marking a 12.22% YoY decrease from USD 943.2/mt. The downturn reflects a deepening structural crisis in the sugar industry. The National Sugarcane Growers Union reported producer losses exceeding USD 759.26 million (MXN 14 billion) in the 2024/25 cycle due to weaker demand, increased use of high-fructose corn syrup, and proposed IEPS tax reforms that could further harm domestic producers.

Pakistan’s sugar prices rose by 0.46% WoW to USD 603.6/mt, up 28.90% YoY from USD 468.3/mt, supported by strong import demand and a weaker US dollar. Pakistan’s Trading Corporation (TCP) has issued tenders for up to 320,000 mt of sugar for immediate delivery, as part of a broader government-approved plan to import 500,000 mt to stabilize domestic retail prices. Meanwhile, US raw sugar futures declined by 2.67% WoW to USD 345.5/mt, down 29.54% YoY from USD 490.3/mt pressured by analytics’ forecast of a 4.1 mmt global surplus for 2025/26 and investor profit-taking. Sugar markets remain under bearish pressure due to ample supply from Brazil and global surplus forecasts, though selective import activity in Asia continues to provide regional price support.

2. Price Analysis

Brazilian Sugar Declines as Exports Surge, Supply-Driven Pressure Persists

Brazil’s sugar prices have continued their gradual decline in Oct-25, driven by rising export volumes and stable production levels that are maintaining market oversupply. In W41, domestic sugar prices averaged USD 400.40/mt, down 15.7% YoY from USD 475.20/mt despite a sharp 32.8% increase in export volumes compared to Oct-24. This divergence between higher output and lower prices underscores a classic supply-driven price correction, as mills sustain record-high crushing rates and exports expand.

Data from the Secretariat of Foreign Trade (Secex) show that Brazil exported 1.8 mmt of sugar in the first half of Oct-25, generating USD 721 million in revenue, while the number of vessels waiting to load sugar rose to 90, the highest in months. The increase in shipping activity—especially through the Port of Santos—suggests that Brazilian producers are capitalizing on strong international demand, particularly for Very High Polarization (VHP) sugar, even at reduced price levels.

In the short term, Brazilian sugar prices are likely to remain under bearish pressure, with global markets already facing a projected 4.1 mmt surplus for 2025/26. The combination of robust export flows, sustained milling activity, and steady demand from Asia will likely keep prices near current levels through year-end. However, if logistical congestion at ports persists or weather conditions disrupt the upcoming crush, temporary upward corrections may occur. Overall, Brazil’s sugar market remains supply-heavy, favoring stable-to-lower price dynamics in the near term.

3. Strategic Recommendations

Capitalize on Brazil’s Sugar Price Decline Before Supply Pressures Rebound

Global sugar importers should capitalize on Brazil’s current price weakness, as the market remains driven by oversupply and robust export activity. In Oct-25, Brazilian sugar prices averaged USD 400.40/mt, marking a 15.7% YoY decline despite a sharp 32.8% increase in export volumes. This imbalance between elevated output and soft prices reflects a classic supply-driven correction, supported by stable milling activity and strong demand for VHP sugar. With a projected 4.1 mmt global surplus for 2025/26, international buyers have an opportunity to secure competitively priced raw sugar before potential logistical disruptions or weather-related production risks emerge.

This situation presents an optimal procurement window for industrial users and refiners across Asia, the Middle East, and Africa. Importers should prioritize forward contracts and fixed-price agreements with key Brazilian exporters such as Sucden Do Brasil, Valeverde Empreendimentos Agrícolas, and Goiasa Goiatuba Álcool, which are actively supplying raw and organic sugar grades. Securing a multi-month supply now would allow buyers to hedge against port congestion risks—particularly at Santos—and lock low-cost access to high-quality Brazilian sugar through early 2026.