1. Weekly News

Brazil

Brazil's Orange Production Affected by Drought in 2024/25 Season

The Fundecitrus Association has released its first crop report for the 2024/25 season, revealing that Brazilian orange production in the São Paulo and Minas Gerais regions, known as the Citrus Belt, is expected to reach just under 215.8 million boxes. This figure represents a 7.1% decrease from the initial forecast of nearly 232.4 million boxes made on May-24, amounting to a loss of 16.6 million boxes. The reduction in forecasted production is due to smaller fruit sizes caused by severe hot and dry weather conditions during the first four months of the growing season, which were worse than anticipated. Over half of the crop has been harvested under drought conditions, with a sharp decline in annual rainfall and increased temperatures leading to accelerated ripening. Additionally, minimizing losses from citrus greening or Huanglongbing (HLB) disease has prompted an earlier harvest, resulting in 45% of the total crop being collected by mid-August, compared to approximately 30% in previous seasons.

Spain

Intercitrus Calls for Stronger Controls on South African Citrus Imports

The Spanish Citrus Interprofessional Association (Intercitrus) has requested a meeting with key officials from the Ministry of Economy, Trade, and Enterprise to address the ongoing World Trade Organization (WTO) dispute over South African citrus imports. They are advocating for stricter European Union (EU) phytosanitary measures to prevent pests like the false moth and diseases like black spot from entering the region, citing 26 black spot detections in South African shipments this year. Intercitrus contends that the EU's current cold treatment standards for South African oranges are less stringent than those imposed by other countries. This assertion is made even though evidence from the European Food Safety Authority (EFSA) and findings from Tunisia demonstrate that black spots can thrive in Mediterranean climates. The association urges the Spanish government to take strong action to defend these measures against South Africa's repeated phytosanitary issues.

Ukraine

Ukraine's Orange Imports Surge Despite Ongoing Conflict

Ukraine has restored its orange imports for the 2023/24 season, marking the third consecutive year of imports despite the ongoing conflict with Russia. This resilience demonstrates Ukraine's ability to adapt its supply chains in response to the challenges posed by the war. From Nov-23 to Jun-24, Ukraine imported 65 thousand tons of oranges, surpassing last season's total. If this trend continues, the final import figure could approach levels seen in the 2021/22 season, although imports remain below pre-war levels. Notably, in Jan-22, imports were twice the volume recorded in January 2023/24. The market is recovering, driven by increased global orange production. Turkey has significantly boosted its supply to Ukraine, doubling the volume compared to the previous season.

Meanwhile, Egypt is expected to maintain its second-place position as a supplier, especially as Ukraine turned to South African oranges from Jul-24 to Oct-24. Despite competition from Turkey, Egypt remains a crucial player, previously exporting nearly twice as many oranges to Ukraine. As of W42, Ukraine stands as Egypt's second-largest market for oranges in Eastern Europe, following Poland. Additionally, the Egyptian government, in collaboration with the Food and Agriculture Organization of the United Nations (FAO) and the European Bank for Reconstruction and Development (EBRD) project, is organizing a trade mission to Cairo from December 3 to 5, 2024, inviting importers and supermarket chains from Ukraine and the surrounding region.

United States

Florida Citrus Industry Shows Resilience Post-Hurricane Milton

Despite initial concerns, Florida's citrus industry experienced less severe damage from Hurricane Milton than anticipated. In the northern regions near Tallahassee, growers reported minimal storm effects, though some fruit loss occurred earlier due to Hurricane Helene. Satsuma mandarins are still expected to be harvested on schedule in the coming weeks. However, wind and water damage across the state resulted in more fruit on the ground and groves. As growers begin harvesting, a lighter orange crop is anticipated to lead to higher juice prices. With limited Florida citrus and increased production from Texas and Mexico, the market's response will be closely watched.

USDA Predicts Challenging Citrus Harvest for Florida in 2024/25 Season

The United States Department of Agriculture's (USDA) preliminary forecast for Florida's 2024/25 citrus season predicts significant challenges, with orange production expected to reach only 15 million boxes, alongside 1.4 million boxes of grapefruit and 200 thousand boxes of tangerines and tangelos. This represents a nearly 3-million box decline from the previous season, continuing a downward trend. Florida Citrus Mutual, the state's primary citrus growers' organization, raised concerns over the impact of Hurricane Milton and HLB disease on yields, calling for increased support and research. The forecast sharply contrasts with the industry's peak in the 1990s, when production hit 244 million boxes. However, citrus growers remain committed to rebuilding their orchards, restoring production levels, and revitalizing the industry through improved agricultural practices, increased research efforts, and enhanced support systems.

2. Weekly Pricing

Weekly Orange Pricing Important Exporters (USD/kg)

Yearly Change in Orange Pricing Important Exporters (W42 2023 to W42 2024)

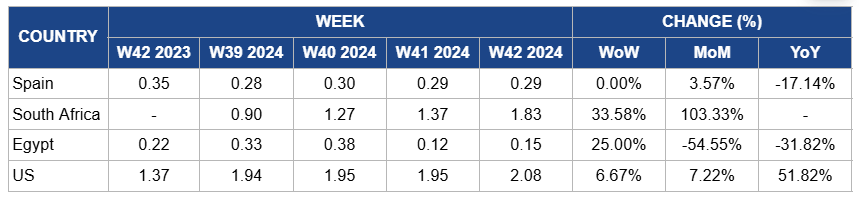

Spain

Orange prices in Spain have remained steady at USD 0.29 per kilogram (kg) in W42 since last week. There was a slight increase of 3.57% month-on-month (MoM) due to favorable production expectations for the 2024/25 season, alongside high prices in the orange juice market that have positively influenced fresh market pricing. However, year-on-year (YoY) prices declined by 17.14% due to last year's abundant harvests and lower production costs, which resulted in increased supply and reduced price levels in the previous season. The current labor shortages and rising production costs contribute to the market's stability, suggesting potential upward pressure on prices in the coming weeks.

South Africa

In South Africa, orange prices surged by 33.58% week-on-week (WoW) to USD 1.83/kg in W42, with a 103.33% MoM increase. This significant rise is due to heightened local demand due to the ongoing concerns over phytosanitary issues affecting exports, particularly the request from Intercitrus for stricter EU measures on South African imports. These developments have generated uncertainty in the export market, prompting local producers to focus on domestic sales. As a result, the increased demand for local oranges has driven prices higher. However, potential regulatory challenges and pest detections in shipments could create market fluctuations in the near future, impacting the sustainability of these price levels.

Egypt

Egypt's orange prices in W42 increased by 25% WoW to USD 0.15/kg due to a slight recovery in demand as buyers sought alternatives to other markets amidst ongoing supply challenges. This uptick followed a significant price decline in W41, allowing producers to regain some pricing power. However, prices remain lower compared to previous periods, with a 54.55% MoM decrease and a 31.82% YoY decline. The monthly and yearly price drops are primarily due to an oversupply in the market ahead of the citrus harvest in December, as producers released more stock to balance inventories and address concerns regarding excess supply, particularly in Europe.

United States

In W42, orange prices in the United States (US) reached USD 2.08/kg, reflecting a 6.67% WoW increase. Additionally, prices rose by 7.22% MoM and surged by 51.82% YoY. The price increase is due to a lighter orange crop anticipated in Florida as growers begin harvesting, following some residual losses from Hurricane Helene. Although Hurricane Milton caused less damage than expected, the overall supply from Florida remains constrained, contributing to upward pressure on prices. Additionally, higher juice prices resulting from the reduced supply likely influence fresh orange prices. The market is also adjusting to increased citrus production from Texas and Mexico, which may help balance supply, but for now, the limited Florida citrus is driving prices higher.

3. Actionable Recommendations

Implement Targeted Pricing Strategies for Florida Citrus

Florida citrus growers should implement targeted pricing strategies to navigate the anticipated lighter orange crop and increased juice prices. By closely monitoring market trends and competitor pricing, growers can adjust their prices to remain competitive while maximizing profits. Additionally, they should consider direct-to-consumer sales channels, such as local markets and online platforms, to capture consumer interest and enhance profit margins. Emphasizing the quality and freshness of Florida citrus can also help differentiate their products in a crowded market, particularly against competitors from Texas and Mexico.

Enhance Water Management Strategies for Brazilian Citrus Production

Citrus growers in Brazil should enhance their water management strategies to mitigate the impacts of ongoing drought conditions. Growers can optimize water usage and improve fruit size and quality by investing in advanced irrigation techniques and moisture monitoring systems. Additionally, soil conservation practices can help retain moisture and reduce the adverse effects of severe weather. Collaborating with agricultural experts to develop contingency plans for future drought scenarios will safeguard production and minimize losses from HLB disease.

Strengthen Phytosanitary Standards for Citrus Imports

The Spanish Citrus Interprofessional Association should advocate for enhanced phytosanitary standards within the European Union to address the ongoing risks of South African citrus imports. By collaborating with relevant stakeholders and conducting thorough research on pest threats, Intercitrus can present a compelling case for stricter regulations. This may include proposing stronger cold treatment protocols and ensuring comprehensive monitoring of shipments. Engaging in discussions with EU officials will help reinforce the importance of safeguarding local citrus production from invasive pests and diseases.

Sources: Tridge, Asaja Cordoba, Comite De Citricos, Eastfruit, Freshplaza, Valencia Fruits, Fruitnet