1. Weekly News

Bolivia

Cochabamba Banana Sector Faces Severe Losses Due to Road Blockades

Banana producers in the Cochabamba tropics of Bolivia are facing significant losses after more than two weeks of roadblocks, which have halted exports to key markets like Uruguay and Chile. This disruption also prevented supplying bananas to the national market. The roadblocks threaten the bilateral export agreements with these countries, potentially leading to canceled contracts. In addition to the banana industry, the blockades have impacted other agricultural and fish farming projects in the Chapare region, including research at the Toralapa Innovation Center and breeding efforts at a fish production facility. The situation remains unresolved, and the ongoing disruptions continue to affect the development of critical agricultural projects in the region.

China

China's Banana Imports Dropped by 13.8% YoY

In Sep-24, China imported 105 thousand metric tons (mt) of bananas, marking a 13.82% year-on-year (YoY) decline and a 16.7% YoY decrease in value to USD 62.8 million. From Jan-24 to Sep-24, China's total banana imports reached 1.2 million tons, down 8.5% YoY, valued at USD 654.7 million, a 22.44% YoY drop. Among major suppliers, Vietnam and Laos saw increases in shipment volumes, while imports from the Philippines, Cambodia, and Ecuador declined, with Ecuador's exports to China falling by 10.61% over the period.

Ecuador

Ecuador's 2024 Banana Exports Rise 0.5% YoY Despite Production Challenges

From Jan-24 to Aug-24, Ecuador exported 274.39 million boxes of bananas, reflecting a modest 0.5% YoY increase. The European Union (EU) remained Ecuador's largest market, followed by Russia, the Middle East, and the United States (US). However, adverse weather conditions, including temperature shifts, excessive rainfall, and intense solar radiation, contributed to a 15% YoY decline in production from Jan-24 to Sep-24. Despite increased bagging efforts, output in the year's second half lagged behind the first. Additionally, exports to Russia fell due to elevated prices and economic pressures from the Ukraine conflict. However, a 1.64% YoY rise in exports to the EU helped offset some of these losses.

Russia

Russian Banana Imports from Ecuador Hit 12-Year Low Amid 20% YoY Decline

Russia's banana imports from Ecuador have dropped to a 12-year low, with only 776 thousand tons imported in the first eight months of 2024, a 20% YoY decrease. This volume marks the lowest since 2012, when imports totaled 755 thousand tons. Historically, Russia imported an average of 958 thousand tons annually over the past five years, accounting for around 25% of Ecuador's banana exports. Although Ecuador remains Russia's primary supplier, Guatemala also provides a notable share of the country's banana imports.

Uganda

Climate Challenges Threaten Uganda's Banana Industry, Prompting New Resilience Measures

Ugandan banana farmers are increasingly vulnerable to extreme weather, with events like the Oct-23 hailstorm destroying 300 banana trees and killing livestock, highlighting the impact of climate change on agriculture. Bananas, a staple crop involving nearly half of Uganda's farmers, have decreased production over the past 15 years due to unpredictable weather. The Nationally Determined Contributions (NDCs) Action Project, led by the United Nations Environment Program (UNEP) and UNEP Copenhagen Climate Centre, has introduced crop insurance, digital damage assessment platforms, and training in sustainable practices to address these challenges. These initiatives aim to build resilience and protect Uganda's banana sector from the growing threats of climate change.

2. Weekly Pricing

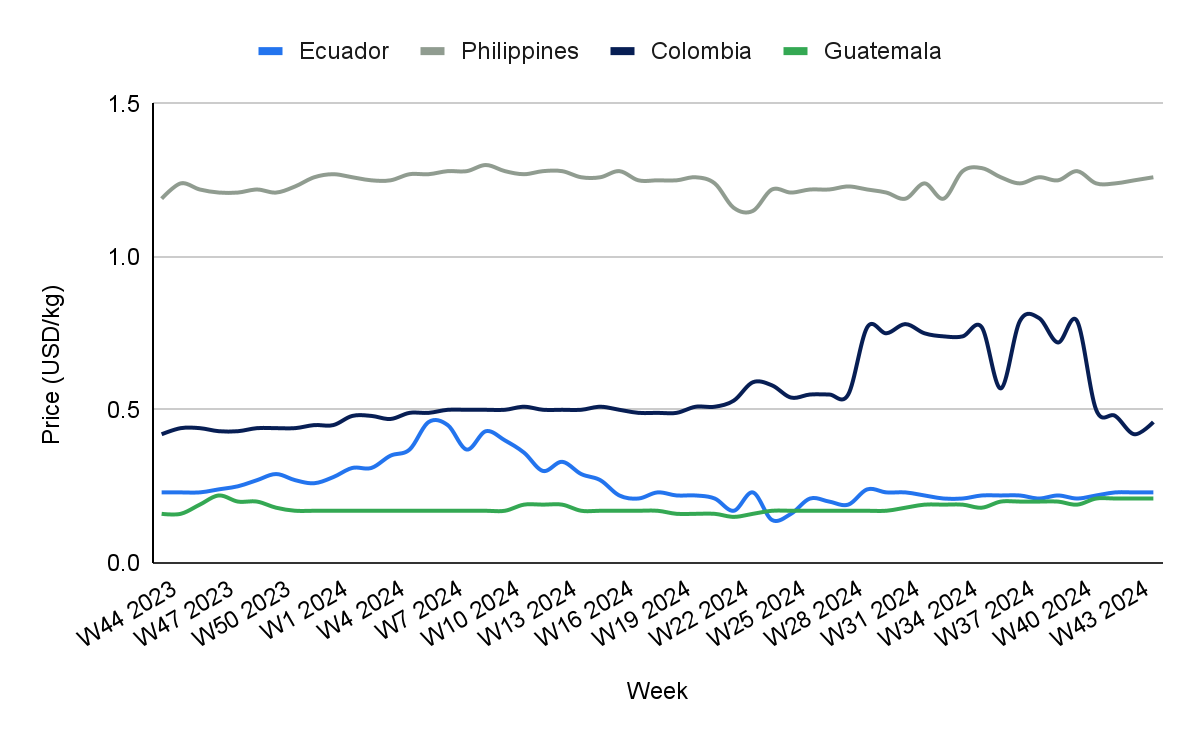

Weekly Banana Pricing Important Exporters (USD/kg)

* Varieties: Ecuador and the Philippines (overall banana average), Colombia (uraba), and Guatemala (criollo)

Yearly Change in Banana Pricing Important Exporters (W44 2023 to W44 2024)

* Varieties: Ecuador and the Philippines (overall banana average), Colombia (uraba), and Guatemala (criollo)

* Blank spaces on the graph signify data unavailability stemming from factors like missing data, supply unavailability, or seasonality

Ecuador

In Ecuador, banana prices remained steady at USD 0.23/kg in W44 since W42, with a 4.55% month-on-month (MoM) increase and no YoY change. This stability is due to a balanced supply level following recent rainfall, which gradually mitigated the prolonged drought's impact on production. Although production volumes are slowly recovering, the market still feels the effects of last season's drought, which limited output. Consistent demand from major markets like the US and the Middle East helped maintain prices. At the same time, increased competition from Central America and African producers, combined with ongoing logistical cost pressures, continues to create a competitive pricing environment.

Philippines

Banana prices in the Philippines increased slightly by 0.80% week-on-week (WoW) to USD 0.26/kg in W44, with a 1.61% MoM increase and a 5.88% YoY rise. This increase is due to ongoing disruptions from recent severe typhoons, which have continued to limit farm access and impacted production volumes. These weather challenges, persistent disease outbreaks, and land use restrictions have tightened supply levels. Despite these difficulties, strong demand from key export markets, particularly Japan and South Korea, sustained price stability and supported the gradual upward trend in YoY prices.

Colombia

In W44, banana prices in Colombia increased by 9.52% WoW and YoY due to a recovery in export demand following the previous week's slowdown and robust interest from primary international buyers throughout the year. This surge in demand, especially from primary export markets like the US and Europe, stabilized prices after the sharp drop in W43. Additionally, YoY prices reflect consistent growth in export volumes driven by improved market access and favorable trade agreements, bolstering Colombia's position in the global banana market. However, MoM prices declined by 8% due to ongoing oversupply from enhanced production conditions, as recent rains have improved yields and fruit quality. While the increased supply initially led to price reductions, the strong demand only partially offset the surplus, resulting in a slight MoM price decrease.

Guatemala

In W44, banana prices in Guatemala remained steady at USD 0.21/kg, with no WoW or MoM change. Moreover, there is a 31.25% YoY increase in banana prices due to sustained strong export demand, particularly from key markets such as the US and Europe. This ongoing demand supported price levels despite previous weather-related disruptions. Additionally, improved weather conditions have further enhanced fruit quality and export readiness, allowing producers to effectively meet international demand and contributing to the YoY price increase. The continued appeal of Guatemalan bananas in the global market also reinforced this positive price trend.

3. Actionable Recommendations

Redirect Banana Exports and Explore Alternative Routes

To mitigate losses, banana producers in Cochabamba should urgently explore alternative transport routes, including cross-border options through Peru and Argentina, to facilitate exports to primary markets like Uruguay and Chile. For domestic supply, producers should consider rail transport and local distribution hubs to bypass affected areas, ensuring steady supply to national markets. Coordinating with logistics providers and negotiating flexibility with trading partners on contract terms can help maintain trade stability and reduce losses amid ongoing disruptions.

Strengthen Banana Farmers' Climate Resilience and Ensure Access to Markets

Ugandan banana farmers should consider alternative supply routes, such as regional railways through Kenya and Tanzania, to maintain access to export markets when facing weather-related disruptions. For domestic supply, establishing resilient local distribution channels and leveraging cooperative-based networks in high-demand areas can provide farmers with more stable outlets for their produce. By adopting these strategies alongside climate adaptation initiatives, farmers can reduce the impact of extreme weather on their livelihoods and ensure continued supply for both export and local markets.

Expand Supplier Base to Secure Banana Imports

Russian banana importers should diversify their sourcing by increasing purchases from alternative suppliers like Guatemala and other Latin American countries to offset the recent drop in Ecuadorian imports. This strategic expansion will help maintain steady supply levels, reduce reliance on a single supplier, and ensure a more resilient banana import market.

Sources: Tridge, Agraria, Agronegocios, EFEcomunica, Expreso, INIAF, Publiagro, RG, UNEP