1. Weekly News

Global

Global Corn Production Up, Exports Drop Due to Lower Chinese Imports and Regional Adjustments

The United States Department of Agriculture's (USDA) Nov-24 forecast projects the 2024/25 global corn production at 1.217 billion metric tons (mt), a 2.21 million metric tons (mmt) increase from the previous forecast. However, global corn exports are expected to decline slightly to 189.83 mmt, and ending stocks are projected to drop to 304.14 mmt. The corn harvest forecast for Ukraine remains unchanged at 26.2 mmt, with exports and ending stocks are also unchanged at 23 mmt and 0.63 mmt, respectively. In the United States (US), corn production is revised downward to 384.64 mmt, while exports stay at 59.06 mmt. Meanwhile, ending stocks for the US is expected to decrease to 49.23 mmt. For China, the forecasted corn harvest is 292 mmt, with imports reduced to 16 mmt and ending stocks dropping to 206.27 mmt.

Belarus

Belarus Corn Harvest Nears Completion with Record Progress in 2024

As of November 10, Belarus farmers completed 99.8% of corn harvesting, with 2.384 mmt of grain threshed, surpassing 2023’s pace. The Brest and Minsk regions were the first to finish harvesting. The Minsk region leads in the gross harvest with 784.9 thousand mt, followed by the Grodno region with 534.5 thousand mt and the Brest region with 459.9 thousand mt. Farmers in Gomel, Mogilev, and Vitebsk regions harvested 264.6, 192.3, and 148.6 thousand mt, respectively.

Brazil

Brazil's Corn Exports Declined in Early Nov-24

According to the November 11 report of the Foreign Trade Secretariat (SECEX) , Brazil's shipments of unmilled corn (excluding sweet corn) reached 1,706,991 metric tons (mt) in the first six days of Nov-24. This figure represents only 23.04% of the total exported in the same month in 2023, which stood at 7,405,902 mt. The daily average of shipments for the first six days of Nov-24 was 284,498.5 mt, reflecting a 23.2% decline compared to the daily average of 370,295 mt recorded in Nov-23.

Brazil's Corn Planting Progress Lags Behind Last Year

As of late W46, Brazil planted 72% of its first corn crop, down from 76% last year, with a 13% weekly advance. In Parana, the Department of Rural Economics (DERAL) reported that farmers planted 98% of their first corn crop for 2024/25, marking a 1% weekly advance. The crop is 2% germinating, 97% in vegetative development, and 1% pollinating, with 96% rated as good and 4% average. Farmers switched some of their planned corn fields to grain sorghum in some areas due to lower production costs. In Rio Grande do Sul, Emater reported 78% planting completion, with the crop generally rated in good condition. Although the forecast predicts that the weather will be dry in Southern Brazil, it does not pose an immediate issue for the corn crop and will need monitoring.

Philippines

Philippines Corn Imports Forecast to Reach 1.5 MMT in 2024/25 Amidst Tariff Reductions

Driven by reduced tariffs, the Philippines will experience a sharp increase in corn imports, projected to reach 1.5 mmt for the 2024/25 season. Recent government measures have slashed in-quota tariffs from 35% to 5% and out-of-quota tariffs from 50% to 15%, making imported corn more affordable. This tariff reduction primarily benefits the livestock and poultry sectors, which are significant consumers of corn feed. However, domestic production remains limited due to pest infestations and typhoon damage. Demand still exceeds supply despite a slight increase in domestic output, prompting increased imports from global suppliers such as Brazil, Argentina, and Southeast Asian countries.

United States

US Reports New Corn Sales of 692,177 MT

On November 13, the USDA reported that the US sold 692,177 mt of corn. Mexico purchased 401,357 mt, while 290,820 mt went to undisclosed destinations. Both volumes came from the 2024/25 harvest. USDA regulations require reporting sales to the same destination of 100,000 tons or more.

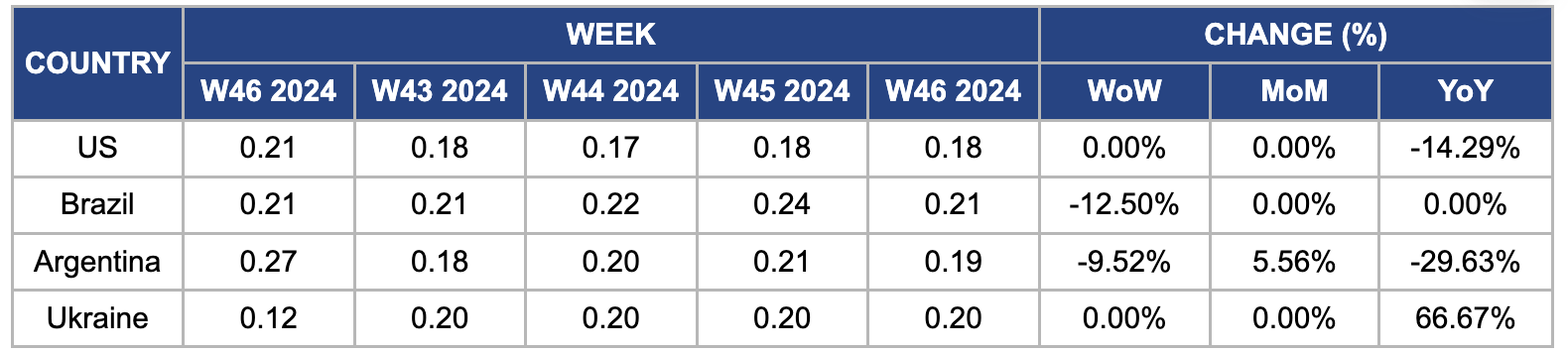

2. Weekly Pricing

Weekly Maize Pricing Important Exporters (USD/kg)

Yearly Change in Maize Pricing Important Exporters (W46 2023 to W46 2024)

United States

In W46, wholesale maize prices in the US remained unchanged week-on-week (WoW) at USD 0.18 per kilogram (kg) but declined 14.29% year-on-year (YoY) from USD 0.21/kg in W46 2023. The USDA reduced its 2024/25 corn production estimate, revising the forecast from 386.16 mmt to 385.55 mmt, slightly decreasing productivity from 11.54 to 11.53 mt per hectare (ha). Despite this, corn farmers are on track to harvest record yields, which, if realized, would make it the second-largest corn crop in history, according to the USDA's Chief Economist.

Brazil

In W46, wholesale maize prices in Brazil declined by 12.50% WoW, reaching USD 0.21/kg from USD 0.24/kg in W45 due to improved weather conditions and rainfall in Brazil. Despite this price drop, Brazil's first corn crop is 72% planted, slightly behind last year's pace of 76%, with farmers in Parana leading at 98% planting completion. The crop is in good condition, although some areas have switched to grain sorghum due to lower costs. The safrinha corn acreage in Mato Grosso is forecasted to decrease slightly due to delayed soybean planting. The planting concentration in central Brazil may be delayed by wet weather, potentially missing the ideal planting window.

Argentina

In W46, the wholesale price of Argentine corn decreased by 9.52% WoW and 29.63% YoY, reaching USD 0.19/kg. This price decline is due to recent rainfall, which improved crop conditions. Moreover, the recovery of water levels in the Pampas region has led to increased planting. Moreover, the 2024/25 campaign is expected to be the fourth most productive in the last 15 years.

Ukraine

In W46, Ukrainian wholesale maize prices held steady WoW at USD 0.20/kg, reflecting a 66.67% YoY increase from USD 0.12/kg in 2023. Due to the price surge, the Ukrainian Agrarian Council (UAC) revised the USDA's forecast for Ukraine's corn harvest downward by 1 mmt to 26.2 mmt due to dry weather conditions. Challenges persist as the country's reliance on deep-sea ports has resulted in a 13% YoY decline in exports through the Constanta port. Moreover, in the Lviv region, autumn fieldwork continues, with 96.5% of winter crops sown, while nearly 60% of the corn planted remains to be harvested. This update comes from the Institute of Agriculture of the Carpathian Region of the National Academy of Sciences.

3. Actionable Recommendations

Strengthen Export Infrastructure in Brazil

Brazil should focus on enhancing its export infrastructure by investing in the modernization of loading terminals, expanding storage capacities, and optimizing transportation links from farms to ports. This includes automating port operations to reduce loading times, building more silos and storage facilities near production areas, and improving road, rail, and river transport systems to ensure smooth and timely delivery of corn to export hubs. These improvements will help streamline the supply chain, reduce delays, lower costs, and maintain Brazil's competitiveness in the global market, particularly as forecasts predict a vital crop for the 2024/25 season.

Diversify Export Markets

Ukraine should diversify its export markets by strengthening trade relationships with emerging regions such as Southeast Asia (e.g., Indonesia, Vietnam, and the Philippines), Africa (e.g., Egypt, Kenya, and Nigeria), and Eastern Europe (e.g., Poland, Romania, and Türkiye). By exploring new trade routes through neighboring countries and leveraging rail and river transport, Ukraine can mitigate the risks posed by disruptions at deep-sea ports. This strategy will reduce its reliance on congested or vulnerable routes, potentially stabilizing its corn export revenue stream and compensating for the reduced harvest forecasts caused by adverse weather and geopolitical challenges.

Implement Smart Irrigation Systems

The US and Ukraine should prioritize investments in advanced irrigation systems like drip and precision irrigation to counter the negative impacts of increasingly frequent and severe dry weather conditions. Drip irrigation delivers water directly to the plant roots, reducing water waste and promoting efficient use. In contrast, precision irrigation uses technology to monitor soil moisture levels and weather patterns to apply water in precise amounts only when necessary. These systems are precious during drought-prone periods, as they ensure crops receive consistent and optimized hydration, improving resilience against water scarcity. By implementing these advanced irrigation technologies, the US and Ukraine can enhance their ability to manage water resources efficiently, stabilize corn yields during dry spells, and even boost productivity despite challenging weather conditions. In the long run, this will mitigate the risk of yield losses due to drought and promote more sustainable and predictable corn production, making these countries more resilient to climate variability and ensuring stable supplies for domestic markets and export needs.

Sources: NoticiasAgricolas, Vinanet, Zol, UkrAgroConsult, NoticiasAgricolas