.jpg)

1. Weekly News

Global

World Sugar Prices Rise 2.6% MoM in Oct-24 Amid Brazil Production Concerns and Higher Oil Prices

According to the Food and Agriculture Organization of the United Nations (FAO) Food Price Index (FFPI), world sugar prices increased by 2.6% in Oct-24, marking the second consecutive monthly rise, but remained 18.6% lower than the previous year. The price increase was driven by concerns over Brazil's 2024/25 sugar production, impacted by dry weather conditions and higher international crude oil prices, which boosted sugar cane use for ethanol. However, the strengthening US dollar and improved rainfall in Brazil's southern regions limited the overall rise in sugar prices. FAO's broader food price index rose 2% in Oct-24, with price increases across all commodities except meat.

India

India's Sugar Production Decreases in Early 2024/25 Season Due to Fewer Operational Mills

According to the National Federation of Cooperative Sugar Factories Ltd (NFCSFL), India's sugar production fell by 44% to 710,000 metric tons (mt) in the first six weeks of the 2024/25 season, down from 1.27 million metric tons (mmt) the previous year. This was due to fewer operational mills. As of November 15, only 144 mills were active, compared to 264 last year, and Maharashtra has yet to commence operations.

Karnataka's output dropped sharply to 2.625 mmt from 5.375 mmt, while Uttar Pradesh had 85 mills in operation. Total sugar production for the season is forecasted to decline to 28 mmt, down from 31.90 mmt in 2023/24, though sugar recovery rates remained stable at 7.82%.

Netherlands

Netherlands Sugar Beet Harvest Faces 10% Yield Decline Due to Cercospora Pressure

As of W46, 42,000 hectares (ha) of sugar beets remain to be harvested in the Netherlands, with a sugar content of 16.7%, slightly higher than the seasonal average. However, the yield is forecasted to be 10% lower than the multi-year average due to limited crop regrowth and increased Cercospora pressure. The fungus, which has spread across the country, has been exacerbated by favorable weather conditions and weakened plant vitality. While sugar content is rising, it is doing so slower due to the impact of the disease on chlorophyll levels. Harvesting conditions are currently favorable, with advice to complete harvesting before expected rain and frost in the coming weeks to avoid risks and storage losses.

South Korea

South Korea Transfers Advanced Sugarcane Forecasting Technology to Boost Indonesia's Agricultural Data Systems

The Rural Development Administration (RDA) of South Korea has developed and transferred a sugarcane production forecasting model to Indonesia as part of the "Indonesian Strategic Crop Food Security Forecast Pilot Project." The project aims to enhance sugarcane production prediction and agricultural data systems using advanced remote sensing technology, including satellite and drone imagery. Information and Communication Technology (ICT) equipment, such as drones, was also provided, along with local training, to improve utilization.

Supported by the Ministry of Agriculture, Food and Rural Affairs through Official Development Assistance (ODA), the initiative seeks to strengthen Indonesia's agricultural policies and food security capabilities. Indonesian officials emphasized the project's significant role in advancing agricultural data and production forecasting systems.

Spain

EU-Mercosur Agreement Threatens Spain's Sugar Beet Industry as Competition from Brazilian Imports Rises

The proposed European Union-Mercosur (Southern Common Market) agreement poses significant challenges to Spain's sugar beet industry, particularly in Castilla y León. Historically a regional agricultural cornerstone, this sector faces heightened competition from low-cost Brazilian sugar cane, potentially displacing beet sugar from the European market. The disparity in production conditions is a major concern, as Mercosur countries employ practices prohibited in the EU, including banned pesticides and transgenic crops, leading to significantly lower production costs.

In 2023, Castilla y León's sugar beet harvest dropped to 1.3 mmt, exacerbating the crisis. The potential influx of cheaper, less regulated Brazilian sugar threatens the viability of regional farms and undermines European standards for food safety, sustainability, and fair labor practices. Stakeholders like the Committee of Professional Agricultural Organizations of the European Union and the General Confederation of Agricultural Cooperatives of the European Union (COPA-COGECA), and the Union of Small Farmers and Ranchers and the Coordinator of Farmers and Ranchers Organizations (UPA-COAG) have called for revisions to the agreement to protect local producers and ensure equitable competition. Without safeguards, the treaty risks further destabilizing this vital agricultural sector.

2. Weekly Pricing

Weekly Sugar Pricing Important Producers (USD/kg)

Yearly Change in Sugar Pricing Important Producers (W46 2023 to W46 2024)

.png)

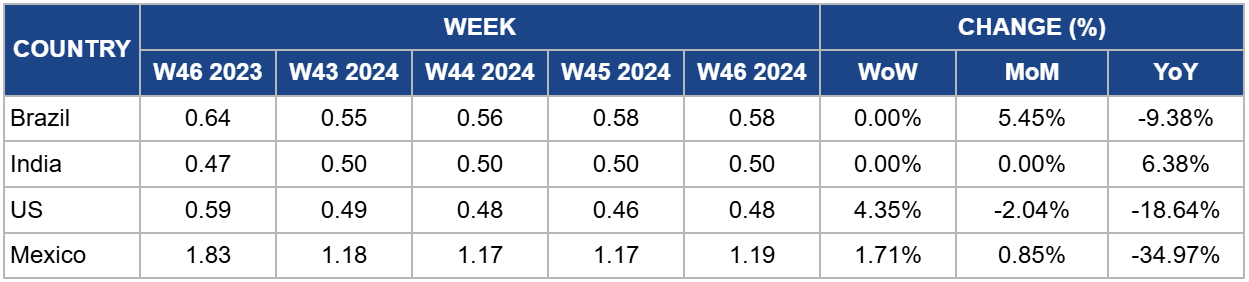

Brazil

Brazil's sugar prices remained stable at USD 0.58 per kilogram (kg) in W46, reflecting a 5.45% month-on-month (MoM) increase from USD 0.55/kg. Despite a significant 21.62% drop in sugarcane milling in the second half of Oct-24, the cumulative milling for the 2024/25 season showed a slight increase of 0.88%. This indicates that while weather conditions have impacted immediate production, the long-term outlook may remain stable. Reducing sugar production by 24.3% and ethanol output by 8.22% could tighten supply, leading to price increases in the medium term, especially if weather-related challenges persist or worsen.

India

In W46, India's sugar prices remained steady at USD 0.50/kg but rose by 6.38% year-on-year (YoY). However, sugar production in India has significantly decreased, falling by 44% to 710,000 mt in the first six weeks of the 2024/25 season compared to the previous year. This decline is due to fewer operational mills, with only 144 mills running as of November 15, down from 264 in the prior season. Key sugar-producing states such as Karnataka and Maharashtra have faced notable drops in output, with Karnataka's production halving. With total production expected to decrease to 28 mmt for the season, the lower output may lead to upward pressure on prices in the coming months.

United States

In W46, United States (US) sugar prices increased to USD 0.48/kg, rising 4.35% week-on-week (WoW) but falling 18.64% YoY. The price increase was driven by a weaker dollar and reduced sugar output in Brazil due to droughts and fires. However, the global outlook remains pressured by increased sugar production in Thailand and India and a stronger dollar, which may limit further price gains in the US. The market’s balance will depend on the impact of global supply disruptions, mainly from Brazil and India's export policies.

Mexico

Mexico's sugar prices increased to USD 1.19/kg in W46, reflecting a 1.71% WoW rise. Veracruz remains the country's primary sugar supplier, accounting for 40% of national production, with 18 active mills. Despite recent challenges, including a five-year decline in sugar production and the impact of climate change, Veracruz's sugar mills remain resilient, producing clean energy and maintaining a balance between local demand and export needs, particularly to the US. The 2023/24 harvest saw decreased cane acreage and sugar production, with totals falling to 743,119 ha and 4.7 mmt of sugar. This drop was due to drought and higher-than-usual temperatures. However, the cyclical nature of the industry's downturn suggests potential recovery for the 2024/25 season, especially with the adaptation of more drought-resistant cane varieties.

3. Actionable Recommendations

Encourage Sugar Production Efficiency Improvements in India and Brazil

India and Brazil, two major sugar producers, should improve efficiency to mitigate current output declines. In India, the reduction in active sugar mills and the expected lower production for the 2024/25 season highlight the need for investment in modern milling technology and increased operational efficiency. Similarly, as it faces drought and higher ethanol demand disruptions, Brazil should prioritize optimizing sugarcane yields through better water management practices and improved crop resilience. By enhancing production capabilities in these key regions, both countries can stabilize their sugar supply and mitigate upward price pressures in the global market.

Adapt Agricultural Practices in the Netherlands to Combat Disease Impact

Given the forecasted lower sugar beet yield in the Netherlands due to increased Cercospora pressure, it is essential to adopt stronger crop protection measures. Farmers should implement integrated pest management strategies to control fungal outbreaks, invest in disease-resistant beet varieties, and improve crop rotation practices to prevent fungus spread. Additionally, enhancing harvesting technologies to minimize post-harvest losses and better manage sugar content during the harvest season will help mitigate production shortfalls. These actions will support a more stable sugar beet supply and reduce the risk of yield reductions in future seasons.

Strengthen Export Market Diversification for Mexican Sugar

Mexico should work to diversify its sugar export markets to reduce reliance on the US and safeguard against market disruptions. By targeting emerging markets in Asia and other regions, Mexico can capitalize on global sugar demand and reduce vulnerabilities from domestic challenges like climate change and drought. Strengthening trade agreements, improving logistical capabilities, and aligning production with market needs will provide Mexico with more stable export opportunities. Expanding into new markets will ensure a more resilient sugar industry and protect against price volatility driven by regional demand fluctuations.

Sources: Agro Meat, Agri Net, Economic Times, Agro Popular, Nieuweoogst, Unica, Barchart