W43 2025: Sunflower Oil

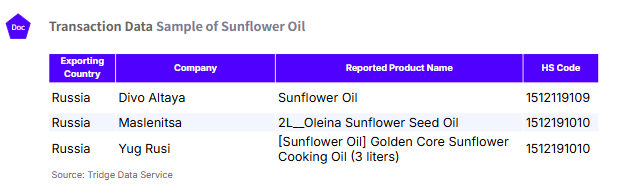

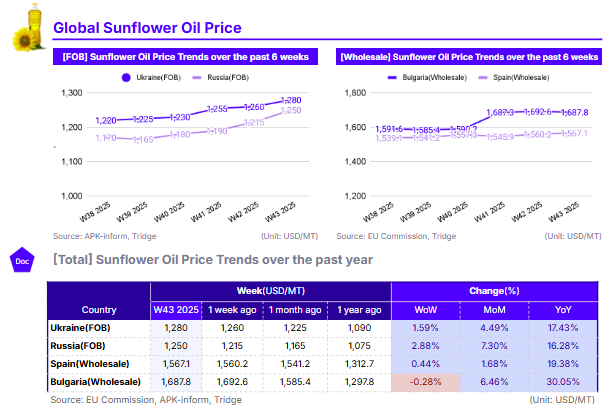

In W43 of 2025, global sunflower oil prices were driven up by supply-side constraints in the Black Sea and Europe. Prices rose WoW in Ukraine to USD 1,280/mt (+1.59%) and Russia to USD 1,250/mt (+2.88%), driven by a significantly delayed Ukrainian harvest that has tightened immediate supply. In the EU, Bulgarian wholesale prices remained high at USD 1,687.8/mt, underpinned by an acute domestic raw material shortage that has driven prices up 6.46% MoM. These short-term shocks are compounding significant YoY gains across all regions, confirming a structurally tight market and a bullish outlook. Russia remains the most price-competitive sourcing option due to its large harvest, but importers must navigate the high geopolitical and logistical risks associated with sourcing from the region. Viable export partners in Russia include Divo Altaya, Maslenitsa, and Yug Rusi.

1. Weekly Price Overview

Black Sea Supply Deficit Drives Short Term Price Increases

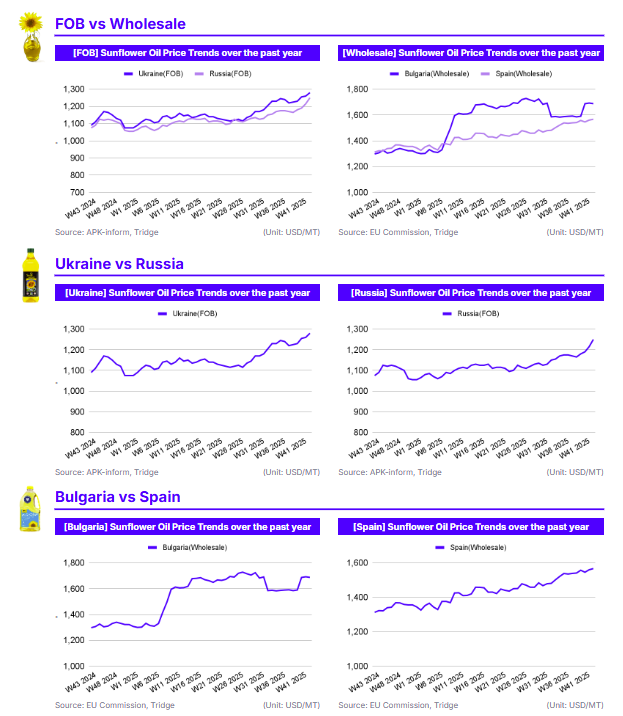

In W43 of 2025, sunflower oil export prices from the Black Sea continued to climb amid growing concerns over a supply deficit. In Ukraine, the Free on Board (FOB) price was USD 1,280 per metric ton (mt), a 1.59% increase week-on-week (WoW). Russia’s FOB price saw a more significant jump of 2.88% WoW to USD 1,250/mt. In the European Union (EU) wholesale market, price movements were mixed. Spain registered a minor 0.44% WoW gain to USD 1,567.1/mt, while Bulgaria saw a slight correction, declining 0.28% WoW to USD 1,687.8/mt.

The upward driver for the Black Sea prices is the slow pace of the Ukrainian harvest, which is projected to be the lowest volume over the past decade, largely due to lower yields. This is creating a significant supply shortage, causing Ukrainian sunseed prices to rise despite farmers increasing sales. This deficit is pulling Russian prices up with it, with traders eyeing higher price targets if the tightness persists. Russia’s price is further supported by the government's decision to extend export duties on sunflower oil, maintaining a high floor for export offers. In contrast, Bulgaria’s slight WoW dip comes despite an acute domestic shortage of raw materials, which has kept its price at a high premium.

2. Price Analysis

Persistent Supply Issues Underpin Broad Monthly and Annual Price Gains

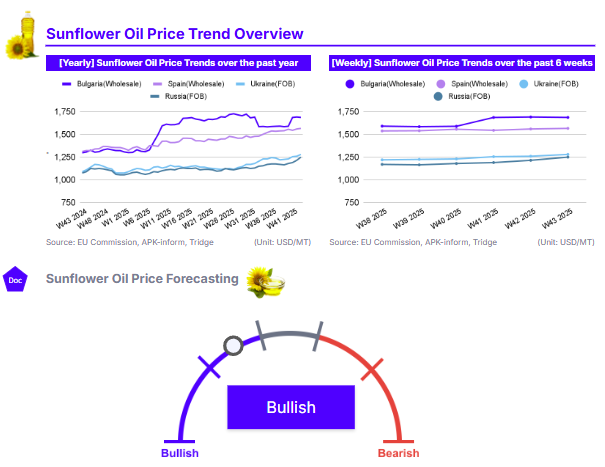

Analyzing the longer-term data, sunflower oil prices in W43 show strong month-on-month (MoM) gains, led by Russia with a 7.30% increase to USD 1,250/mt. Bulgaria and Ukraine also posted significant gains of 6.46% and 4.49% MoM, respectively, while Spain saw a more modest 1.68% rise. This recent upward momentum is driven by immediate supply-side issues. The delayed Ukrainian harvest is creating a significant supply gap, pushing prices for both Ukrainian and Russian oil upward as buyers compete for limited volumes. Russia's 7.30% MoM jump is also reinforced by its export duty policies. In the EU, Bulgaria's strong MoM gain is a direct result of an acute shortage of domestic sunflower seeds, which has prompted discussions of potential export restrictions to protect local crushers.

These strong monthly increases are compounding the already significant year-on-year (YoY) gains, which highlight persistent market tightness. Bulgaria’s wholesale price posted the largest annual increase, rising 30.05% YoY. Spain’s price also climbed 19.38% YoY, while Black Sea export prices showed similar long-term strength, with Ukraine’s FOB price up 17.43% YoY and Russia’s up 16.28% YoY. This demonstrates that the recent supply shocks are exacerbating a market that has been structurally tight for the past twelve months, largely due to the war in Ukraine and challenging weather patterns and structural supply shortages across key European production zones. Given the supply constraints in the 2025/26 production season, the short-term price outlook remains firmly bullish.

3. Strategic Recommendations

Russia's Price-Competitive Sunflower Oil Provides Opportunity But Requires Careful Risk Management

For global buyers seeking to mitigate the high prices seen in the EU and the supply uncertainty in Ukraine, Russia presents a clear sourcing opportunity. In W43, Russia's FOB sunflower oil price of USD 1,250/mt is the most competitive among major exporters, standing significantly below EU wholesale levels in Bulgaria and Spain. This price advantage is supported by strong supply fundamentals. Unlike Ukraine, which is facing a delayed and smaller harvest, and Bulgaria, which has an acute raw material shortage, Russia's 2025 harvest is large and above 2024 levels. This combination of the lowest price and good volume availability makes it an attractive option for importers.

However, buyers must balance this opportunity with the significant geopolitical and logistical risks involved. Sourcing from a nation engaged in an active war carries inherent uncertainties, including potential disruptions to Black Sea port operations, high insurance premiums, and complex payment channels.. Therefore, importers considering Russia should conduct thorough due diligence on their logistics partners and secure comprehensive cargo insurance. This strategy is best suited for buyers who have a high-risk tolerance and can implement robust contingency plans to manage supply chain interruptions. ridge Eyeʼs transaction level data highlights Divo Altaya, Maslenitsa, and Yug Rusi as viable export partners in Russia.