1. Weekly News

Global

Contrasting Corn Outlooks for Brazil and Argentina in 2024/25

Brazil and Argentina, critical players in the global corn trade, are entering the 2024/25 season under contrasting conditions. Brazil is projected to produce 120 million metric tons (mmt) of corn, a 3.6% increase year-on-year (YoY). This is driven by a robust safrinha crop, which is expected to reach 94 mmt, a 5% rise, contingent on favorable weather. However, despite robust production, Brazil's corn exports are forecast to decline significantly, from 56 mmt in 2023 to 41 mmt in 2024, due to rising supply in the United States (US), Europe, and Ukraine, coupled with a sharp drop in Chinese demand.

Conversely, Argentina faces challenges, with corn production expected to drop by 11% YoY to 51 mmt in the 2024/25 season, the lowest in 17 years. This is due to a 25% reduction in planted area to 7.2 million hectares (ha) caused by the corn stunt disease. Many Argentine farmers are shifting to soybeans due to lower input costs. Despite lower production, Argentina's corn exports are set to rise 9% YoY to 36 mmt. Driven by strategic market positioning, this figure is the highest in recent years.

Brazil

Brazil’s Reduced Nov-24 Corn Export Forecast

Brazil's Nov-24 corn exports reached 3.46 mmt as of November 25, representing only 46.75% of the volume exported in the same period in 2023 at 7.41 mmt. The daily export average has dropped by 33.2% YoY, from 370,295 metric tons (mt) per day in Nov-23 to 247,347 mt/day this year, reflecting a significant decline in export pace. Nov-24's total exports are expected to surpass 5 mmt, driven by residual demand from traders. However, the outlook for Dec-24 could be more optimistic, with slowing new business posing concerns about reaching export targets. In financial terms, Brazil has generated USD 728.36 million from corn exports this month, a sharp drop from USD 1.68 billion in Nov-23. The daily revenue has also declined by 38%, from USD 83.92 million last year to USD 52.03 million in 2024, highlighting the combined impact of reduced export volumes and lower prices.

Bulgaria

Bulgaria's Maize Exports Plummet Amid Poor Harvest

Since the start of the new season, Bulgarian maize exports have plummeted to a record low, with only 38 thousand mt exported as of September 1, marking an 86% decline YoY compared to 275 thousand mt last year and a staggering 92% below the six-year average of 467 thousand mt. This drastic reduction stems from the worst corn crop in a decade, with production estimated at 1.47 mmt, a significant drop from 2.27 mmt last season. The summer drought and heatwave severely reduced yields, and high levels of aflatoxins have further hindered exports as traders hesitate to offer contaminated corn to traditional buyers. On the import side, Bulgaria brought in 45 thousand mt of maize by November 15, a sharp increase from just 1,500 mt the previous year. Local starch producers have resorted to importing maize to meet demand, underscoring the severe domestic supply constraints.

United States

GM Seeds and Technological Advancements Drive US Record Corn Yield in 2024

The US is poised for a record corn grain yield in 2024 exceeding 12 mt/ha. Corn yields have surged sixfold since the 1940s due to advances in hybrid seed genetics, biotechnology, and precision farming. The introduction of genetically modified (GM) corn in 1996 has been pivotal, with over 90% of US corn acreage now planted with pest- and herbicide-resistant GM varieties. Corn remains the most widely grown crop in the US, with producers harvesting around 200 mmt from 36 million ha, contributing USD 60 billion annually to the economy, potentially rising to USD 75 billion during high-demand periods. While agriculture accounts for only 5% of the US economy, corn is crucial in rural communities across Iowa, Nebraska, and Illinois. Historically, wheat was the dominant grain, but shifts in agricultural policy and trade dynamics in the late 20th century cemented corn's dominance alongside soybeans.

2. Weekly Pricing

Weekly Maize Pricing Important Exporters (USD/kg)

Yearly Change in Maize Pricing Important Exporters (W48 2023 to W48 2024)

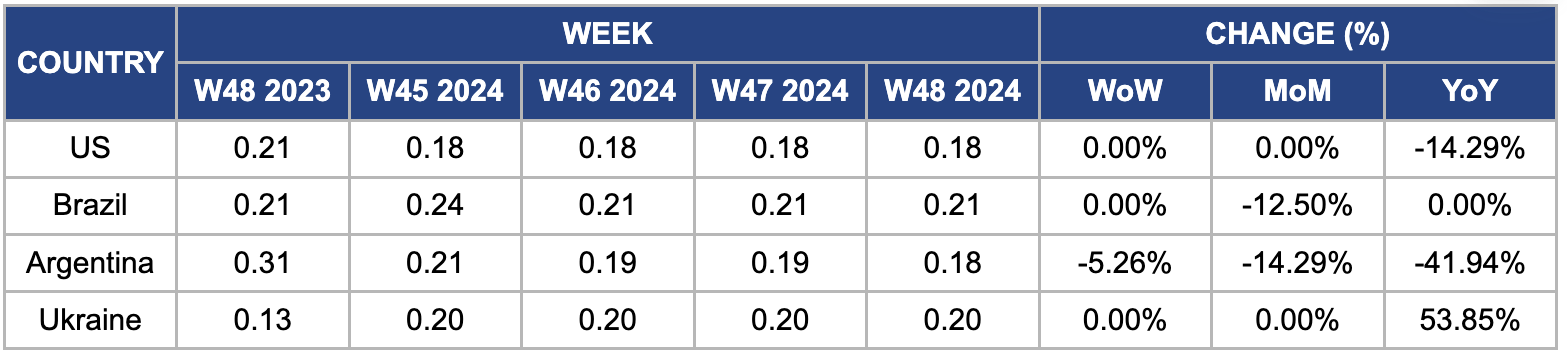

US

In W48, wholesale maize prices in the US remained stable week-on-week (WoW) at USD 0.18 per kilogram (kg) but decreased by 14.29% YoY. This price stability follows a forecast for a record corn yield in 2024, surpassing 12 mt/ha. The US corn sector has experienced significant productivity gains, with yields increasing sixfold since the 1940s, mainly due to advances in hybrid seed genetics, biotechnology, and precision farming. Moreover, corn remains the most widely grown crop in the US in terms of acreage and output.

Brazil

In W48, wholesale maize prices in Brazil remained stable WoW but dropped 12.50% month-on-month (MoM), reaching USD 0.21/kg. This decline was due to improved weather conditions and rainfall. On the seller's side, Center for Advanced Studies in Applied Economics (CEPEA) researchers report that many corn producers, mainly from São Paulo, are refraining from negotiations and are focusing on the development of the upcoming summer harvest, which has been influenced positively by favorable weather in most regions. The 2024/25 summer harvest sowing is nearing its final stages in southern Brazil.

Argentina

In W48, the wholesale price of Argentine corn declined 5.26% WoW, 14.29% MoM, and 41.94% YoY, reaching USD 0.18/kg. This price drop is due to recent rainfall, which has improved crop conditions. Argentina's corn sowing plans for the 2024/25 campaign are optimistic, with reduced leafhopper and disease pressure, as the Dalbulus Maidis National Monitoring Network reported. The Association of Argentine Cooperatives (ACA) expects an increase in the planting of late corn varieties. While these varieties yield less than early corn, they can still be profitable with proper management. The Rosario Stock Exchange projects that nearly 8 million ha will be planted, with potential production estimated at 51 to 52 mmt.

Ukraine

In W48, Ukrainian wholesale maize prices remained steady WoW at USD 0.20/kg, reflecting a 53.85% YoY increase from USD 0.13/kg in 2023. The price surge is due to the United States Department of Agriculture's (USDA) corn harvest forecast being revised downward by 1 mmt to 26.2 mmt due to dry weather conditions. Challenges persist as Ukraine's reliance on deep-sea ports has led to a 13% YoY decline in exports through the Constanta Port. Moreover, the Ministry of Agrarian Policy and Food has announced the completion of the harvest season, reporting a total collection of 53.9 mmt of grain.

3. Actionable Recommendations

Optimize Crop Protection and Disease Management

Argentina and Ukraine should prioritize investment in disease-resistant seed varieties and integrated pest management (IPM) techniques. Utilizing GM corn with better pest resistance, as seen in the US, could improve disease and environmental stress resilience. In addition, adopting weather forecasting technologies and precautionary soil treatments will help manage risks tied to extreme climate conditions. Training farmers on these practices and facilitating access to the latest technologies could significantly improve productivity and mitigate the risks of reduced crop yields in future seasons.

Expand into Emerging Markets and Strengthen Trade Partnerships

To counter the impact of declining demand in traditional markets, exporters from Brazil and Argentina should focus on diversifying into emerging regions such as Southeast Asia, sub-Saharan Africa, and South America, where corn demand is increasing due to population growth, urbanization and changing dietary habits. Strengthening trade relationships with key countries like Mexico, Egypt, and the Middle East is crucial, as these regions remain significant importers of corn. Additionally, exporters should explore opportunities within regional trade agreements like Mercosur and work with multilateral organizations such as the WTO to reduce trade barriers, secure preferential tariffs, and improve market access. These strategies can help mitigate the risks of shrinking demand from significant buyers and ensure long-term export growth.

Enhance Export Offerings with Value-Added Products

To address declining raw corn exports and increasing competition, exporters in Brazil and Argentina should focus on enhancing their offerings with value-added products such as corn syrup, bioethanol, corn flour, and corn starch. These products generally yield higher profit margins and are less vulnerable to the volatility of global grain markets. Widely used in the food and beverage industry, corn syrup offers a stable revenue stream. At the same time, bioethanol production, driven by the worldwide push for renewable energy, can cater to growing demand in key markets like the European Union (EU) and Japan. Moreover, with the rising popularity of gluten-free diets, corn flour, and starch are in demand for food and industrial applications. By investing in these sectors, along with promoting sustainable production practices and product quality, Brazil and Argentina can diversify their export portfolios, capture higher-value markets, and reduce their reliance on traditional bulk grain exports, ensuring more consistent profitability in the long term.

Sources: Agroportal, NoticiasAgricolas, Zol, Agro Digital