In W16 in the peanut landscape, some of the most relevant trends included:

- Peru exported 2,538 mt of conventional shelled peanuts in 2024, valued at USD 2.2 million, with key markets including Ecuador, France, and the Netherlands.

- Responsible for 42% of national output, Georgia began peanut planting earlier than usual in 2025. The expansion to approximately 950,000 acres is driven by low corn and cotton prices, alongside favorable weather conditions supporting a strong crop outlook.

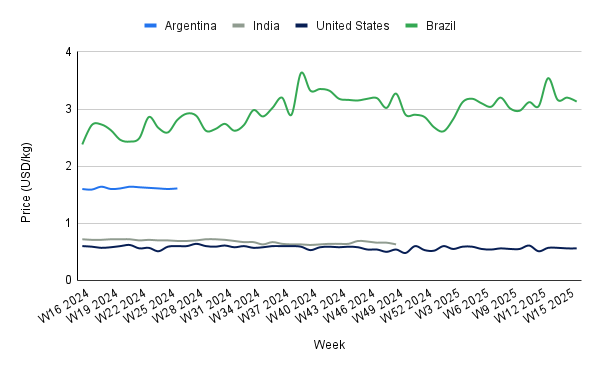

- Brazil's peanut prices decreased by 2.19% WoW in W16, as exporters aggressively lowered prices to regain market share lost during the weak 2024 crop. This move could pressure prices in competing regions like the US and Nicaragua.

1. Weekly News

Peru

Peru's 2024 Peanut Exports Reach 2,538 MT

According to the Ministry of Agrarian Development and Irrigation (MIDAGRI), Peru exported 2,538 metric tons (mt) of conventional shelled peanuts valued at USD 2.2 million in 2024. Key export destinations included Ecuador, France, and the Netherlands. Peanut cultivation in Peru spans approximately 4,000 hectares (ha), primarily concentrated in the coastal valleys of Lima and Piura, with smaller production areas in Ayacucho, San Martín, and Loreto.

United States

Georgia Begins Early Peanut Planting as Acreage Expands to 950,000 Acres in 2025

Peanut planting started in South Georgia in W16, with growers beginning earlier than usual due to an anticipated expansion to approximately 950,000 acres, driven by persistently low corn and cotton prices. Apr-25 marks a key planting period across Georgia, as favorable weather and soil conditions create ideal circumstances for establishing a strong peanut crop.

Georgia remains the leading peanut-producing state in the United States (US), accounting for 42% of national output. While the state cultivates a wide range of crops, peanuts are a cornerstone of Georgia's agricultural identity. With 9.9 million acres of farmland and more than 39,000 farms, the state’s agricultural legacy continues to thrive, securing its reputation as the nation’s ‘Peanut State.’

2. Weekly Pricing

Weekly Peanut Pricing Important Exporters (USD/kg)

Yearly Change in Peanut Pricing Important Exporters (W16 2024 to W16 2025)

United States

In W16, US peanut prices held steady at USD 0.56/kg, unchanged from the previous week but down 6.67% year-on-year (YoY). The decline reflects favorable production expectations, as planting commenced early in South Georgia, driven by low corn and cotton prices and optimal weather conditions. With acreage projected to expand to 950,000 acres, a potential increase in supply could exert further downward pressure on prices later in the 2025 season. However, future price trends will depend on weather developments and yield outcomes during the growing period.

Brazil

In W16, Brazil's peanut prices fell to USD 3.13/kg, reflecting a 2.19% week-on-week (WoW) decline despite a 31.51% YoY increase from USD 2.38/kg. The mid-harvest phase is yielding strong quality and volumes, but persistent rainfall poses risks of delays and potential output reductions. The recent price drop is largely driven by Brazil's strategic push to regain market share following a weak 2024 crop. Exporters are employing aggressive pricing, particularly in non-European markets, to reassert their presence, potentially placing downward pressure on prices from key competitors such as the US and Nicaragua. However, if adverse weather continues to hinder harvest completion, a tighter supply outlook could emerge, applying upward pressure on prices in the medium term.

3. Actionable Recommendations

Enhance Market Differentiation Through Value-Added Peanut Products

In light of Brazil's aggressive pricing strategy and increasing competition in non-European markets, exporters in Peru and the US should prioritize investments in value-added peanut processing. Developing products such as roasted or flavored peanuts, peanut butter, and snack formulations can improve price resilience, diversify revenue streams, and appeal to health-conscious and convenience-driven consumers. Public-private partnerships and targeted branding efforts can further boost global market positioning.

Strengthen Regional Market Integration and Trade Diversification

Given Peru's growing peanut exports to Ecuador, France, and the Netherlands, stakeholders should explore trade expansion within Latin America and emerging Asian markets. By aligning with regional food safety and quality standards, participating in trade expos, and negotiating preferential trade agreements, exporters can reduce overreliance on a few destinations and enhance market access amid global price volatility.

Sources: Tridge, Agraria, Southeast AgNet, The Citizen