W17 2025: Palm Oil Weekly Update

.jpg)

In W17 in the palm oil landscape, some of the most relevant trends included:

- Global palm oil exports are forecast to reach 25 mmt by Sep-25, driven by increased output from Indonesia and Central American exporters. However, Malaysia and Thailand's exports are expected to decline slightly.

- Palm oil is becoming more price-competitive than soybean oil, particularly in India, which has resumed significant palm oil purchases after a five-month slowdown. This is expected to support Malaysian palm oil futures.

- The US has imposed a 24% tariff on Malaysian palm oil, potentially affecting exports. Malaysia is exploring new markets and working with ASEAN partners to mitigate the impact. Additionally, Malaysia is expanding its research to improve yields and address quality control issues.

- Malaysia is launching the MSPO Impact Alliance by Q3-2025 to enhance EUDR compliance. This initiative will focus on green financing, traceability, deforestation monitoring, and smallholder support.

1. Weekly News

Global

Palm Oil Export Volumes Set to Rise as Price Competitiveness Strengthens

Global palm oil exports are showing signs of recovery amid increased supply and improved price competitiveness, according to analysts at the Oil World. By Sep-25, global exports are forecast to reach 25 million metric tons (mmt), reflecting an output rise from major producing countries. Indonesia’s shipments are expected to grow to 12.43 mmt, up from 11.59 mmt a year earlier, alongside an increase from Central American exporters. In contrast, exports from Malaysia and Thailand are projected to decline slightly to 8.5 mmt and 0.67 mmt, respectively. The Malaysian Palm Oil Board (MPOB) also forecasts rising demand from China and India, as palm oil has become more price-competitive than soybean oil, reinforcing its attractiveness in key import markets.

India

India’s Palm Oil Imports Rebound on Price Correction, Supporting Market Recovery

India has resumed significant palm oil purchases after a five-month slowdown since Dec-24, driven by a correction in prices that made palm oil cheaper than soybean oil. As of W17, crude palm oil (CPO) is offered at around USD 1,050 per metric ton (mt) Cost, Insurance, and Freight (CIF) for May-25 delivery, compared to USD 1,100/mt for soybean oil. As a result, India’s palm oil imports are expected to rise from an average of 384,712 mt per month from December to April to over 500,000 mt in May and exceed 600,000 mt in June. The renewed buying by the world’s largest palm oil importer is expected to support Malaysian palm oil futures, which have fallen nearly 10% in 2025. Stock depletion and competitive pricing are prompting refiners to replenish inventories, with imports forecast to remain strong through Sep-25.

Malaysia

Malaysia Responds to US Tariffs with Export Diversification, Research Expansion, and Quality Initiatives

According to MPOB’s chairman, Malaysia is seeking to diversify its palm oil export markets following the imposition of a 24% tariff by the United States (US), which threatens to reduce export volumes. While the tariff is expected to impact Malaysian exports, the MPOB notes that US industries could also face higher costs due to limited alternatives to palm oil. Malaysia is working with the Association of Southeast Asian Nations (ASEAN) partners on a coordinated regional response. Furthermore, the MPOB has expanded its research focus to include technology and socio-economic issues, aiming to boost stagnant yields through advanced biotechnology and breeding initiatives. Concerns over mineral oil hydrocarbons in food products persist, with Malaysia reporting shipment rejections from European markets, highlighting the need for stricter quality controls.

Malaysia to Launch MSPO Impact Alliance to Boost EUDR Compliance

Malaysia is preparing to launch the Malaysian Sustainable Palm Oil (MSPO) Impact Alliance by Q3-2025 to strengthen compliance with the European Union Deforestation Regulation (EUDR). Led by the MSPO certification body, the initiative will focus on green financing, digital traceability, deforestation monitoring, and smallholder support. As of Dec-24, 86.47% of Malaysia’s oil palm area had been MSPO-certified. The alliance seeks to enhance sustainable sourcing standards through collaboration with non-governmental organizations (NGO), financial institutions, and major consumer goods companies, including Nestlé Malaysia, which is deepening its commitment to certified sustainable sourcing.

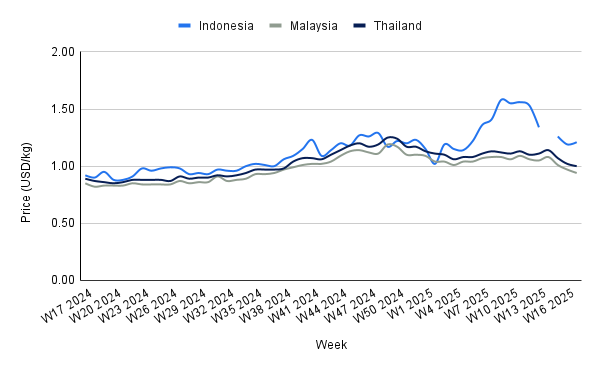

2. Weekly Pricing

Weekly Palm Oil Pricing Important Exporters (USD/kg)

Yearly Change in Palm Oil Pricing Important Exporters (W17 2024 to W17 2025)

Indonesia

In W17, Indonesia's palm oil prices rose to USD 1.21 per kilogram (kg), marking a 1.68% week-on-week (WoW) increase and a 31.52% year-on-year (YoY) surge. This upward movement reflects tightening domestic supply amid higher consumption during Ramadan and resilient export performance. Indonesia's palm oil exports dipped by nearly 2% in Mar-25 compared to Feb-25, reaching 2.02 mmt. However, shipments were 13% higher YoY, marking the strongest Mar-25 exports in four years. Despite a seasonal consumption rise, the strong export base indicates robust underlying demand, as Indonesian palm oil regained price competitiveness against Malaysian offerings and began trading at a discount to soybean oil.

Indonesia's palm oil prices are expected to remain supported through mid-2025, driven by stronger exports to India and other Asian markets and tighter domestic inventories following Ramadan and the B40 biodiesel mandate. While seasonal production increases may moderate gains, firm external demand, and limited supply growth should underpin prices.

Malaysia

Malaysia's palm oil prices declined to USD 0.94/kg in W17, representing a 3.09% WoW drop and a 12.96% month-on-month (MoM) decline from USD 1.08/kg. This recent price correction is attributed to sluggish global sentiment and rising stockpiles. However, demand fundamentals appear poised to strengthen, potentially stabilizing prices in the near term.

The MPOC forecasts that restocking by China and India, Malaysia’s two largest palm oil buyers, ahead of the summer season will support demand. India, which imported 3.03 mmt in 2024, and China, with 1.39 mmt, are both expected to replenish inventories, incentivized by palm oil's price discount against soybean oil. This price advantage, combined with recovering soybean oil prices amid US biofuel policy adjustments, may help cap further declines in palm oil prices.

Thailand

In W17, Thailand’s palm oil prices declined to USD 1.00/kg, down 1.96% WoW and 12.28% MoM decrease from USD 1.14/kg. The continued price weakness reflects broader agricultural pressures, as Thai farmers face rising cultivation costs alongside falling commodity prices. Calls for government intervention to stabilize farm incomes highlight the risk of further supply disruptions if producer margins continue to erode. Unless domestic support measures are introduced or regional demand strengthens, palm oil prices in Thailand may remain under downward pressure, particularly as global production seasonally increases and competition from lower-priced alternatives persists.

3. Actionable Recommendations

Diversify Export Markets to Offset US Tariffs

Given the 24% tariff on Malaysian palm oil exports to the US, Malaysia should focus on diversifying its export markets to reduce dependence on the US. This can be achieved by strengthening trade relations with emerging markets in Africa, the Middle East, and Asia, including countries like China and India, where demand for palm oil is rising. Additionally, Malaysia can explore opportunities in regions with less regulatory pressure, such as Eastern Europe, to safeguard revenue streams and reduce the impact of tariff impositions.

Leverage Price Competitiveness to Drive Demand

Palm oil producers, especially in Malaysia and Indonesia, should capitalize on the growing price competitiveness of palm oil compared to soybean oil. By emphasizing the cost-effectiveness of palm oil in key markets like India and China, producers can stimulate restocking and increase market share. Targeted marketing campaigns and strategic pricing models could be used to encourage bulk purchases and long-term contracts, ensuring sustained demand despite fluctuations in global prices.

Invest in Sustainability and Certification to Meet European Union Demands

To comply with the EUDR and address growing sustainability concerns, Malaysian producers should accelerate their efforts to expand the MSPO certification. Engaging in green financing, digital traceability, and deforestation monitoring will help secure access to European markets and strengthen the credibility of Malaysian palm oil in the global market. By aligning with international sustainability standards, Malaysia can increase exports to environmentally conscious consumers and corporations, enhancing long-term market resilience.

Sources: Tridge, Ukr AgroConsult