In W17 in the potato landscape, some of the most relevant trends included:

- Dry and sunny weather in the EU-4 has facilitated planting, with acreage expected to increase by 5%. Despite the dry conditions posing potential long-term drought risks, farmers are shifting to potato cultivation, particularly in regions like Northern France and Wallonia.

- Potato prices in Russia have soared to USD 1.80/kg in W17, with neighboring countries like Belarus, Kazakhstan, and Georgia adjusting their import/export strategies. In contrast, prices in Lithuania and Poland remain much lower, showcasing stark price disparities in the region.

- France saw a weekly increase in potato prices due to tighter domestic supply, while prices in Pakistan dropped due to increased production. In Egypt, prices rose MoM, driven by strong export demand, particularly from new markets.

1. Weekly News

Europe

EU-4 Spring Potato Planting Surged Despite Historic Drought

In spring 2025, Northwestern Europe (EU-4: Netherlands, Belgium, France, and Germany) is experiencing rapid potato planting progress, driven by dry and sunny weather, the driest in over a century for the Netherlands and Belgium. Around 65% of planting is complete in the Netherlands and France, and 50% in Belgium and Germany. Total EU-4 acreage is expected to increase by 5%, surpassing 600 thousand hectares (ha). Farmers are shifting from dairy to potato cultivation due to limited profitable alternatives, particularly in Northern France and Wallonia, where processing potato acreage is expanding. While current dry conditions pose long-term drought risks, they are favorable for planting and soil structure, especially on lighter soils. Market dynamics remain mixed, with processors relying on pre-contracted volumes, though some growers are speculating on non-contracted crops amid strong demand for varieties like Innovator. Historical data suggests that dry springs do not necessarily reduce yields, and with sufficient rainfall during tuber formation, the region could see strong production outcomes.

Russia

Potato Prices Surged in Russia as Belarus and Kazakhstan Tightened Exports

Russia is facing a notable potato shortage, driving prices above USD 1.27 per kilogram (kg) in many regions, with prices reaching up to USD 1.80/kg in Kaliningrad for imported or new-season potatoes. In response, neighboring countries are reacting differently. Belarus is slowing down imports to avoid domestic price hikes, while Kazakhstan has imposed an export ban. Meanwhile, Georgian suppliers capitalized on the situation, profiting from Russia’s increased demand. In contrast, potato prices in Lithuania and Poland are significantly lower, at roughly half the Russian rate, highlighting a stark price disparity between Russia and its Western neighbors.

United States

Idaho Leads 2025 US Potato Acreage Decline Amid Contract Reductions

Idaho’s potato acreage will decline 5% year-on-year (YoY) in 2025, dropping from 315 thousand acres in 2024 to 300 thousand acres. Total United States (US) potato acreage is expected to fall 4%, from 930 thousand to 891 thousand acres. The steepest cuts will be in Idaho, Washington, Oregon, and Maine. All three major frozen potato processors have significantly reduced contract volumes for the 2025 crop by 5% to 15%, with some growers losing contracts entirely. Hydrator contracts are down by 30% or more. A surplus of raw potatoes has led to some supplies being diverted to feedlots, while demand for early-harvested potatoes remains weak.

2. Weekly Pricing

Weekly Potato Pricing Important Exporters (USD/kg)

Yearly Change in Potato Pricing Important Exporters (W17 2024 to W17 2025)

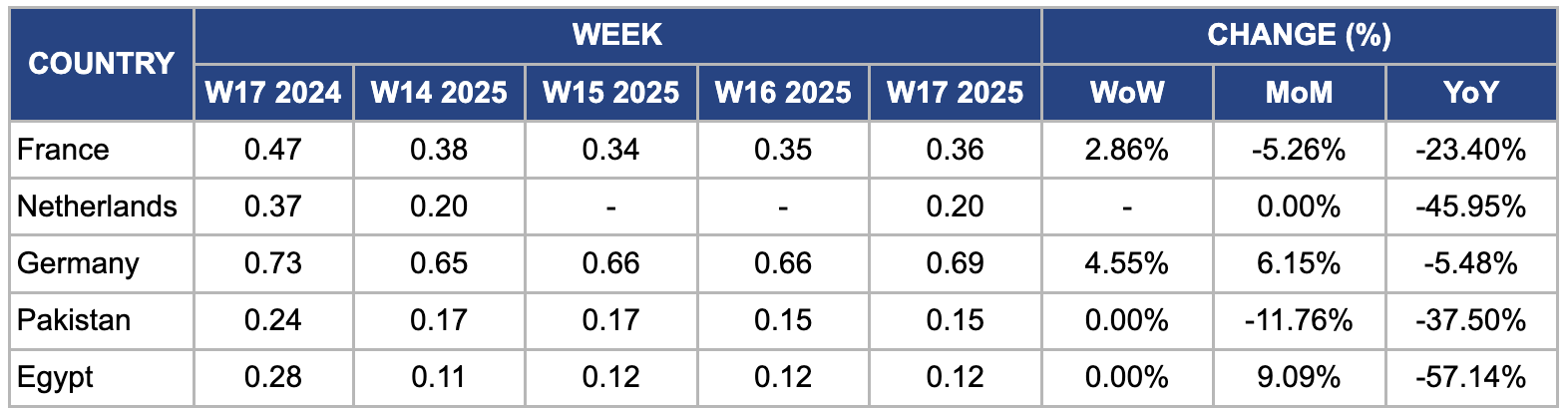

France

In W17, France's potato prices rose to USD 0.36/kg, marking a 2.86% week-on-week (WoW) increase, driven primarily by tightening domestic supply. The 2024/25 harvest was impacted by excessive rainfall in key regions such as Brittany and the Loire Valley, which has reduced yield and quality, leading to lower-than-expected marketable stocks. Steady demand, especially from processors securing potatoes for fresh consumption and products like fries, has further supported the price increase. Moreover, rising energy and transportation costs have contributed to higher prices throughout the supply chain, affecting both retail and wholesale levels.

Netherlands

In W17, Dutch potato prices remained steady month-on-month (MoM) at USD 0.20/kg, although they experienced a sharp 45.95% decline YoY. In 2025, the Dutch potato market saw significant changes driven by production dynamics, market demand, and pricing trends. The Netherlands' potato harvest will reach 3.598 million metric tons (mmt), a 6.5% increase from the previous year, due to higher yields and expanded cultivation areas. Despite this production boost, the market remained unpredictable, with producer prices jumping from USD 14.14 per 100 kg in Oct-24 to USD 33.93 in Feb-25, reflecting concerns about tight supply and market volatility.

Germany

In W17, Germany's wholesale potato prices rose by 4.55% WoW and 6.15% MoM, reaching USD 0.69/kg. Germany's potato market will experience a slight decline in production and yields. The Federal Ministry of Food and Agriculture (BMEL) forecasts a total potato crop of approximately 10.9 mmt for 2025, slightly above the multi-year average but a decrease from the previous year's bumper harvest of 12.67 mmt. This decline is due to climate change, which has resulted in consistently lower average yields over the past five years.

Pakistan

In W17, Pakistan’s potato prices dropped significantly by 11.76% MoM to USD 0.15/kg, reflecting a 37.50% YoY decline. Farmers in Punjab, the country’s key potato-producing region, actively harvested crops, flooding the market with fresh potatoes. Encouraged by favorable returns from the previous season, many farmers expanded their planting areas, while supportive weather conditions contributed to higher yields and increased overall supply. Stable input costs, particularly for fertilizers and fuel, eased the financial burden on producers, allowing them to remain profitable despite lower prices. On the demand side, reduced export interest helped lower external pressure, keeping more supply within domestic channels. Moreover, improvements in the internal distribution system facilitated the efficient movement of produce to key consumption hubs, contributing to balanced market conditions.

Egypt

In W17, Egypt's potato prices remained stable WoW but saw a 9.09% MoM increase, reaching USD 0.12/kg. This price rise is due to strong export demand, driven by expanded access to new markets such as Tajikistan and the Balkans and renewed demand in traditional markets like Spain and the Gulf. Moreover, exports to Russia have increased, supported by reduced customs duties to curb food inflation. Egypt's potato exports will grow by 10 to 15% YoY in 2025.

3. Actionable Recommendations

Develop Risk-Management Strategies for Weather Variability and Market Volatility

European farmers should focus on implementing water-efficient irrigation systems, particularly on lighter soils, to protect against potential drought stress during tuber formation. Moreover, potato growers should explore crop insurance or hedging options to manage the financial risks due to unpredictable weather patterns, such as extreme rainfall or droughts. These measures will help ensure a more stable income, even if weather conditions disrupt the growing season. Given the rising demand for processing potatoes, especially in regions like Northern France and Wallonia, farmers should assess opportunities to increase their planted areas with processing varieties, ensuring they are well-positioned to meet demand while mitigating the risks of market volatility due to weather or price fluctuations.

Strengthen Domestic Supply Chains and Explore Regional Export Opportunities

Russia is facing a significant potato shortage. To address this issue, Russian potato producers should invest in improving domestic production efficiency and expanding regional supply chains. Collaborating with local agricultural technology firms to enhance potato yields through modern farming practices or adopting drought-resistant varieties could mitigate the country's reliance on imports. Furthermore, Russia’s potato producers should explore regional export opportunities, especially to markets less affected by domestic price increases, such as Central Asia or other Eastern European countries. This would help alleviate internal shortages while capitalizing on higher demand in these regions. Strengthening storage and logistics infrastructure would also help smooth out supply fluctuations caused by seasonal variations in production.

Monitor Shifts in Contract Volumes and Domestic Market Adjustments

US farmers should explore alternative markets for their crops, mainly fresh potato varieties, and consider diversifying into non-frozen potato products to compensate for the decline in processing contracts. Engaging in direct sales to retailers or leveraging consumer trends for specialty potato products (e.g., organic or heritage varieties) could provide additional revenue streams. Furthermore, with the surplus of raw potatoes being diverted to feedlots, it may be advantageous for US farmers to explore opportunities in animal feed markets or invest in value-added products like dehydrated potatoes. On a global scale, monitoring export trends and securing international contracts will be crucial, as shifts in processing demand in countries like the US and changes in international potato prices can provide growth opportunities for growers in countries like Egypt, which are seeing rising export demand due to favorable market conditions.

Sources: Tridge, Fox 46, Liga.Net