In W17 in the sugar landscape, some of the most relevant trends included:

- In Brazil's Minas Gerais, sugarcane production for 2025/26 is expected to decline by 7.1% YoY due to prolonged drought and reduced rainfall, which have led to lower productivity and sugar content. This decline comes despite a nearly 10% increase in cultivated area and a production shift favoring sugar over ethanol.

- To strengthen technical training, address labor shortages, and boost long-term industry competitiveness, Tanzania is advancing its sugar sector development through a USD 2.22 million investment to upgrade the NSI.

- Ukraine's sugar sector faces a projected 17% YoY reduction in sugar beet sowing in 2025 due to unfavorable weather and a strategic shift to lower-risk crops, leading to a production drop from 1.8 mmt to 1.5 mmt and a steep decline in exports, particularly to the EU.

1. Weekly News

Brazil

Minas Gerais Sugarcane Harvest Drops 7.1% in 2025/26 Following Drought

The 2025/26 sugarcane harvest in Minas Gerais is projected at 77.2 million metric tons (mmt), down 7.1% from the previous cycle due to prolonged drought and lower-than-expected rainfall in 2024. Productivity is expected to decline by 12.5%, and the raw material quality is expected to decrease. This is indicated by a reduced concentration of total recoverable sugars (ATR) per metric ton (mt), which will drop by 2.3%. Despite this, the cultivated area increased by 9.8%, reaching 1.23 million hectares (ha), reinforcing Minas Gerais' position as Brazil's second-largest producing state. The production mix has shifted in favor of sugar, which now accounts for 52.4% of total output (5.32 mmt), while ethanol's share is expected to decline to 47.6%.

Tanzania

Tanzania Invests Over USD 2.2 Million to Modernize National Sugar Institute and Strengthen Regional Industry Training

The Tanzanian government has invested over USD 2.22 million (TZS 6 billion) to modernize the National Sugar Institute (NSI) in Kilosa, Morogoro Region, aiming to transform it into a leading center for sugar industry training in East and Central Africa. The investment focuses on upgrading infrastructure, learning facilities, and staff capacity, with USD 1.22 million (TZS 3.3 billion) already utilized and an additional USD 1.11 million (TZS 3 billion) planned for the next fiscal year. Supported by the Sugar Industry Development Trust Fund (SIDTF), the initiative includes constructing a new hostel, acquiring modern equipment, and sending tutors abroad for advanced training. These efforts are part of a broader strategy to strengthen the sugar sector by addressing labor shortages and improving technical expertise.

Tanzania’s Sugar Sector Strengthens with Rising Production and Investment

Tanzania's sugar sector has made significant progress. Joint efforts by the government, private investors, and innovators have stabilized supply chains, normalized prices, and boosted consumer confidence. According to the Sugar Board of Tanzania, national sugar production rose from 295,000 mt in 2018 to 460,000 mt in 2023, driven by factory expansion, increased cultivation, and improved support for smallholder farmers. New investments, fertilizer subsidies, low-interest loans, and favorable policies have positioned the country to close the supply gap and potentially generate exportable surpluses. Stakeholders emphasized the need for greater innovation, technology transfer, and affordable mechanization to sustain growth and global competitiveness.

Ukraine

Vinnytsia Farmers Complete 50% of Planned Sugar Beet Sowing Amid Favorable Conditions

In the Vinnytsia region, Ukrainian farmers have completed sowing 50% of the planned sugar beet area as part of the ongoing spring sowing campaign. Favorable weather has supported progress, with early grain crops already fully sown and technical crops now underway. According to the Vinnytsia Regional Agricultural Office, the region plans to sow over 395,000 ha of spring grains and legumes this year, matching last year's levels. The timely sowing of sugar beets is crucial for ensuring a stable supply for Ukraine's sugar industry.

Ukraine Cuts Sugar Beet Area Due to Weather Risks and EU Trade Pressures

Ukraine is set to reduce its sugar beet sowing area by 17% year-on-year (YoY) in 2025, leading to a drop in sugar production from 1.8 mmt in 2024 to 1.5 mmt this year and a sharp decline in exports, particularly to the European Union (EU). The National Association of Sugar Producers of Ukraine (Ukrsugar) attributes the cutback to unfavorable weather and a shift toward less risky crops. Sugar exports are expected to fall to 180,511 mt from 746,000 mt last year, with EU-bound shipments dropping to 27,258 mt. The European Commission (EC) is also moving to restrict Ukrainian sugar imports amid pressure from EU producers over falling domestic prices.

2. Weekly Pricing

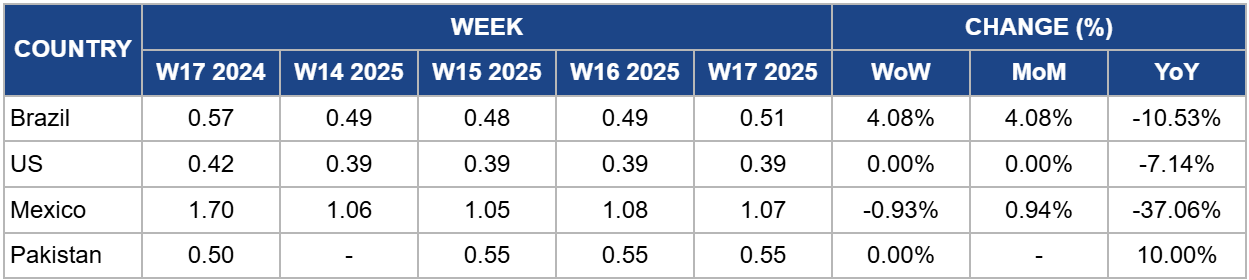

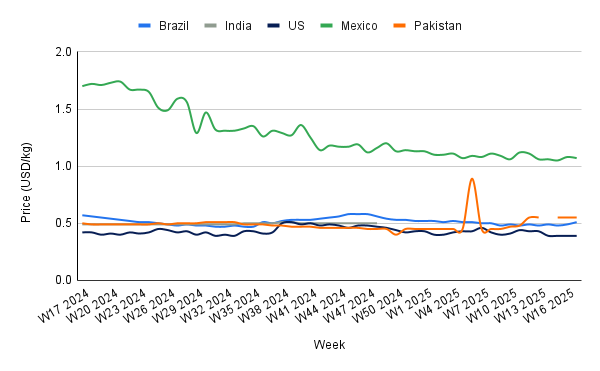

Weekly Sugar Pricing Important Producers (USD/kg)

Yearly Change in Sugar Pricing Important Producers (W17 2024 to W17 2025)

Brazil

Brazil's sugar prices rose to USD 0.51 per kilogram (kg) in W17, an increase of 4.08% both week-on-week (WoW) and month-on-month (MoM), reflecting tightening supply amid challenging production conditions. The country's 2024/25 sugarcane harvest is estimated at 676.96 mmt, a 5.1% decline from the previous season. This drop is driven by drought, excessive heat, and widespread field fires in the key Central-South region, which produces over 90% of the national output. Average productivity dropped to 77,223 kg/ha, with the Southeast, the most affected area, seeing a 12.8% decline in yield. Despite these setbacks, Brazil's sugar output remains robust at 44.1 mmt (down 3.4%), the second-highest on record, owing to strong market incentives favoring sugar over ethanol. These supply constraints are likely to maintain upward pressure on domestic prices in the short term, especially as global demand remains steady and climate-related risks persist.

United States

In W17, the United States (US) sugar prices held steady at USD 0.39/kg, unchanged from the previous week and month, and declined by 7.14% YoY. This reflects reduced price pressure compared to the elevated levels seen in 2024. Despite this stabilization, favorable spring planting conditions for sugar beets across key regions such as Idaho, Oregon, and Washington point to the potential for a strong 2025 crop. With early sowing nearly complete, up to two weeks ahead of average in some areas, and limited need for replanting, early indicators suggest solid yield prospects. A slight 2% reduction in planned acreage reflects a strategic alignment with processing capacity rather than weather-related constraints. If favorable conditions persist and water availability remains sufficient, as current outlooks suggest, strong production could exert downward pressure on domestic prices in the coming months. However, any late frost events or irrigation shortfalls could still pose risks to output and price stability.

Mexico

Mexico’s sugar prices fell to USD 1.07/kg in W17, down 0.93% WoW and marking a 37.06% decline YoY from USD 1.70/kg. The price drop is largely attributed to the opening of sugar imports, which has saturated the domestic market and driven prices down for local producers. This oversupply has undermined the market position of Mexican sugarcane growers, and concerns persist over the final pricing outcome of the ongoing harvest. While US tariffs on certain Mexican agricultural products have not yet affected the local sugar sector, uncertainty remains over potential trade developments.

Pakistan

In W17, Pakistan's sugar prices were at USD 0.55/kg, an increase of 10% YoY from USD 0.50/kg. The price has been stable for several weeks but despite this, domestic markets are under significant pressure due to an ongoing supply halt by sugar mills, triggered by a government-imposed price cap and delayed price revisions. The resulting market shortage has pushed wholesale prices above the official ceiling, with expectations of further increases in the coming days. Tensions between mills, dealers, and the government, exacerbated by tax policy changes, have created uncertainty and constrained supply flows. If the pricing dispute persists without resolution, domestic sugar prices are likely to climb further, amplifying inflationary pressures and eroding consumer access, particularly during peak demand periods.

3. Actionable Recommendations

Enhance Climate Resilience and Agricultural Efficiency

Sugar producers in Minas Gerais should invest in climate-resilient sugarcane varieties and precision irrigation technologies to mitigate the impact of recurring droughts and declining productivity. Partnerships with agricultural research institutions can support the development of drought-tolerant cultivars, while water-efficient systems and soil health monitoring can help stabilize yields and ATR despite weather volatility.

Diversify Export Markets and Strengthen Domestic Supply Strategies

Given the reduced sowing area and expected export shortfalls, Ukrainian producers and policymakers should prioritize strategic domestic allocation and explore alternative markets beyond the EU. Implementing buffer stock mechanisms and engaging in bilateral trade negotiations with new importers in Asia or North Africa could help mitigate revenue loss and support sector stability amid shifting EU trade policies.

Sources: Tridge, Canal Rural, IPP Media, Super Agronom, Agro News Castilla y León, Chini Mandi