In W19 in the apple landscape, some of the most relevant trends included:

- Apple production and export volumes show resilience and growth across key producing countries, with Chile and New Zealand projecting increases and Mexico maintaining stable output despite weather challenges.

- Improved apple quality and variety performance, particularly among red and premium types like Pink Lady and Fuji, supports stronger market positioning and competitiveness.

- Favorable weather recovery, better farming practices, and expanded planting in countries like New Zealand enable rebound efforts even in the face of past climate events and new trade barriers.

- Trade dynamics are shifting, with Peru heavily relying on imports from the US and Argentina, while export players like New Zealand navigate tariffs and phytosanitary rules to maintain market access.

1. Weekly News

Chile

Chile’s Apple Industry Forecasts 4.4% Growth in Volume and Improved Quality for 2025

Chile’s apple industry is expected to increase by 4.4% in overall shipments for the 2025 season, reaching an estimated 573.65 thousand tons, with growth largely driven by red varieties. Pink Lady apples are expected to rise by 5% in volume and improve by over 8% in quality, strengthening their market position, while Fuji apples may increase by 6%. In contrast, Cripps Pink apples are projected to decline by 3% due to weaker color development. Export forecasts include 114.51 thousand tons for Pink Lady, a slight 2% dip to 243.8 thousand tons for Gala, and a nearly 50% surge to 62.89 thousand tons for other red varieties. Green apple exports are also set to grow by 6%, with Club Verde volumes holding steady. Based on input from leading producers and exporters representing most of Chile’s fresh apple trade, these figures are subject to an updated forecast expected in late May-25 or early Jun-25.

Mexico

Chihuahua Expects Stable Apple Harvest in 2025 Despite Weather Challenges

Apple growers in Chihuahua, Mexico's leading production state, expect the 2025 harvest to match last year’s output of 25 million boxes, valued at around USD 256 million (MXN 5 billion). Although a cooler-than-normal season has delayed flowering and impacted fruit set, producers remain cautiously optimistic. Chihuahua contributes about 85% of Mexico’s total apple production, estimated at 815 thousand tons, with 31 thousand of its 35 thousand hectares (ha) of orchards currently in active use. Major producing areas include Cuauhtémoc, Guerrero, and Namiquipa. As growers carry out thinning and tilling to enhance fruit size and quality, a more precise forecast will be available in the coming weeks. With national apple consumption averaging 8.2 kilograms (kg) per person annually, efforts to promote domestic demand are underway, including the launch of the first National Mexican Apple Day on September 20.

New Zealand

New Zealand Apple Exports Rebound Strongly Despite Cyclone and Tariffs

New Zealand’s apple industry is rebounding strongly in the 2024/25 marketing year, with exports projected to reach 560 thousand metric tons (mt) despite challenges from Cyclone Gabrielle. Favorable weather, better farming practices, increased seasonal labor, and maturing orchards have all contributed to the recovery, prompting growers to expand planting. Apple exports to key markets such as East Asia and the United States (US) are forecasted at 360 thousand mt. While new US tariffs introduced on Apr-25 pose challenges, New Zealand apples continue to command premium prices that help offset these costs. The country’s small trade deficit with the US and proactive phytosanitary efforts, highlighted by a Nov-24 exemption from additional moth-related documentation, have further boosted export momentum, positioning New Zealand as a resilient player in navigating global trade pressures.

Peru

Peru’s Apple Imports Reach Nearly 6 Million Kg in Early 2025

Between Jan-25 and Mar-25, Peru imported around 5.94 million kg of apples valued at USD 9.1 million, with the US accounting for 79% of the volume and Argentina 18%. Imports from Chile were minimal during this period due to a health-related suspension that was only lifted at the end of Apr-25. Major retail and fruit companies led the import activity, building on the country’s total apple imports in 2024, which reached 39.3 million kilos worth USD 47 million.

2. Weekly Pricing

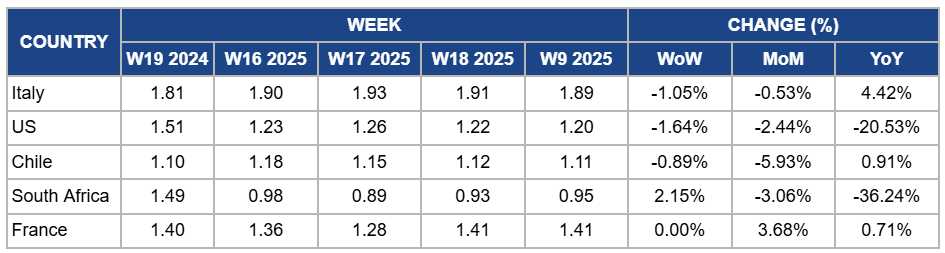

Weekly Apple Pricing Important Exporters (USD/kg)

Yearly Change in Apple Pricing Important Exporters (W19 2024 to W19 2025)

Italy

In Italy, apple prices dropped by 1.05% week-on-week (WoW) to USD 1.89/kg in W19, with a 0.53% month-on-month (MoM) decrease due to sluggish local demand and increased availability of late-season varieties, which exerted downward pressure on prices. However, YoY prices increased by 4.42% due to a 16% reduction in national apple supply compared to the previous year, particularly affecting varieties like Fuji and Golden Delicious. Additionally, steady demand for premium and organic apples in local and export markets has contributed to maintaining higher price levels compared to 2024.

United States

Apple prices in the US dropped by 1.64% WoW to USD 1.20/kg in W19, reflecting a 2.44% MoM decrease and a 20.53% YoY decline due to persistent oversupply from the 2023/24 season, particularly in major producing regions like Washington, and subdued local demand. The oversupply has led to unprofitable prices for growers, as the abundant supply has outpaced market absorption capacity. Additionally, high production costs have further strained profitability. The YoY price decline is also influenced by the lingering effects of trade imbalances and tariff uncertainties, which have disrupted export markets and contributed to excess local supply.

Chile

Chilean apple prices decreased by 0.89% WoW to USD 1.11/kg in W19, marking a 5.93% MoM decline due to increased export volumes, particularly of red varieties, which expanded by over 49% compared to the previous season, leading to greater availability and price pressure in key markets. However, YoY prices increased slightly by 0.91% due to improved fruit quality, especially among Pink Lady and Fuji varieties, which have seen higher demand in premium markets like Brazil and the US.

South Africa

Apple prices in South Africa increased by 2.15% WoW to USD 0.95/kg in W19 due to reduced availability in local markets as the harvest season neared its end, limiting fresh apple supplies. However, MoM and YoY prices dropped by 3.06% and 36.24%, respectively, due to a significant increase in overall production volumes. This surge in supply was driven by favorable weather conditions, the maturation of young orchards, and the adoption of high-yielding apple varieties, leading to a 5% rise in apple exports compared to the previous year.

France

Apple prices in France held steady at USD 1.41/kg in W19, with a 3.68% MoM increase and a 0.71% YoY rise. This stability is attributed to consistent domestic demand and a balanced supply, as production levels have remained steady without significant disruptions. The slight YoY increase reflects moderate inflation and sustained consumer interest in apples, maintaining price levels above the five-year average.

3. Actionable Recommendations

Diversify Export Strategies to Offset Trade Barriers

Apple producers in New Zealand, Chile, Poland, and South Africa should diversify their export destinations and product offerings to reduce exposure to tariffs and trade disruptions. Growers can strengthen resilience by targeting emerging markets in Southeast Asia and the Middle East, offering tailored apple varieties like sweeter Gala for Asia or firmer Fuji for the Gulf. Exporters should also explore value-added products such as sliced, dried, or juiced apples to capture niche demand and maintain revenue despite shifting trade dynamics.

Strengthen Import Readiness for Market Re-Entry

Apple exporters in Chile, the US, and Argentina should proactively re-engage with Peruvian buyers by prioritizing consistent quality, meeting phytosanitary standards, and coordinating with large importers. Chilean producers, in particular, should rebuild trust after the recent suspension by offering competitive pricing and highlighting improvements in food safety. US and Argentine growers can secure market share by timing shipments around seasonal gaps and offering varieties suited to Peruvian consumer preferences, such as Gala and Red Delicious.

Sources: Tridge, Agraria, Eastfruit, Eldiariodechihuahua, Freshfruitportal, Freshplaza, Masp, Namc, Rttnews