In W20 in the maize landscape, some of the most relevant trends included

- Global corn production will rise to 1.264 billion mt in 2025/26, driven by growth in the US, Ukraine, and Argentina. However, due to strong consumption, global ending stocks are projected to decline.

- Indonesia forecasts a 12.9% YoY production increase for early 2025.

- Japan may increase US corn imports amid ongoing trade negotiations.

- Ukraine remains the leading corn supplier to the EU despite growing competition from the US.

- US corn prices rose due to delayed planting caused by excessive rainfall and strong export demand. Meanwhile, prices in Brazil, Argentina, and Ukraine declined, supported by improved weather and increased supply conditions.

1. Weekly News

Global

Global Corn Output to Rise in 2025/26 but Higher Consumption Expected to Drive Stocks Down

In its May-25 report, the United States Department of Agriculture (USDA) forecasts that global corn production will rise to 1.264 billion metric tons (mt) in 2025/26, up from 1.221 billion mt in 2024/25. Despite the increase in output, the USDA projects global ending stocks to fall from 287.29 million metric tons (mmt) in 2024/25 to 277.84 mmt in 2025/26 due to high global consumption. The United States (US), Ukraine, and Argentina will drive this production growth.

Brazil will slightly raise its corn output from 130 mmt in 2024/25 to 131 mmt in 2025/26, while maintaining exports at 43 mmt. However, Brazil will reduce its ending stocks sharply from 5.98 mmt to 2.58 mmt, signaling faster production flow or increased domestic demand. In the US, the USDA anticipates output to grow from 377.63 mmt to 430.55 mmt, with yields rising from 187.56 to 189.35 bushels per acre. It expects ending stocks to climb from 35.95 mmt to 45.72 mmt, keeping ethanol use steady at 139.71 mmt. Exports are forecast to rise from 66.04 mmt in 2024/25 to 72.8 mmt in 2025/26, reflecting improved global competitiveness.

Indonesia

Indonesia Forecasts 12.9% Rise in Maize Output in H1-2025

The Central Statistics Agency (BPS) has forecast that Indonesia will produce 8.07 mmt of dry maize (14% moisture) during the Jan-25 to Jun-25 period, marking a 12.88% year-on-year (YoY) increase compared to the same period in 2024, when output was lower. The BPS Deputy stated that the Apr-25 to Jun-25 period will drive most of this increase, with production expected to reach 3.34 mmt, up from the Mar-25 estimate of 1.63 mmt. Although farmers harvested only 0.29 million hectares (ha) in Mar-25, BPS projects that the harvested area will expand to 0.58 million ha in the coming months. Ten provinces will play a key role in contributing to this output.

Japan

Japan Considers Boosting US Corn Imports Amid Trade Negotiations

The Japanese Prime Minister communicated that Japan might increase US corn imports due to ongoing trade negotiations with Washington. During a parliamentary session, the prime minister emphasized that Japan would not compromise its agricultural sector in exchange for lower US auto tariffs. To ease tensions, Japan considers boosting North American corn imports a more politically acceptable move than increasing rice imports, since the ruling Liberal Democratic Party heavily depends on support from domestic rice farmers. Moreover, Japan may offer the US technical cooperation in shipbuilding. In 2024, the US exported USD 2.8 billion worth of corn to Japan.

Ukraine

Ukraine Leads EU Corn Imports Despite Rising US Competition and Regional Acreage Declines

With a 57% market share, Ukraine remains the leading Eastern European supplier of corn to the European Union (EU), outpacing Poland and Romania. EU corn imports are progressing faster than in the past five seasons. Despite reduced purchases from China this season, Ukraine offset the decline by doubling corn exports to Türkiye. However, competition from the US has intensified, particularly in distant EU markets like Spain and Portugal. Moreover, corn acreage will decline in Romania and Bulgaria in 2025 due to production risks, whereas Ukraine anticipates an increase in corn harvest.

2. Weekly Pricing

Weekly Maize Pricing Important Exporters (USD/kg)

Yearly Change in Maize Pricing Important Exporters (W20 2024 to W20 2025)

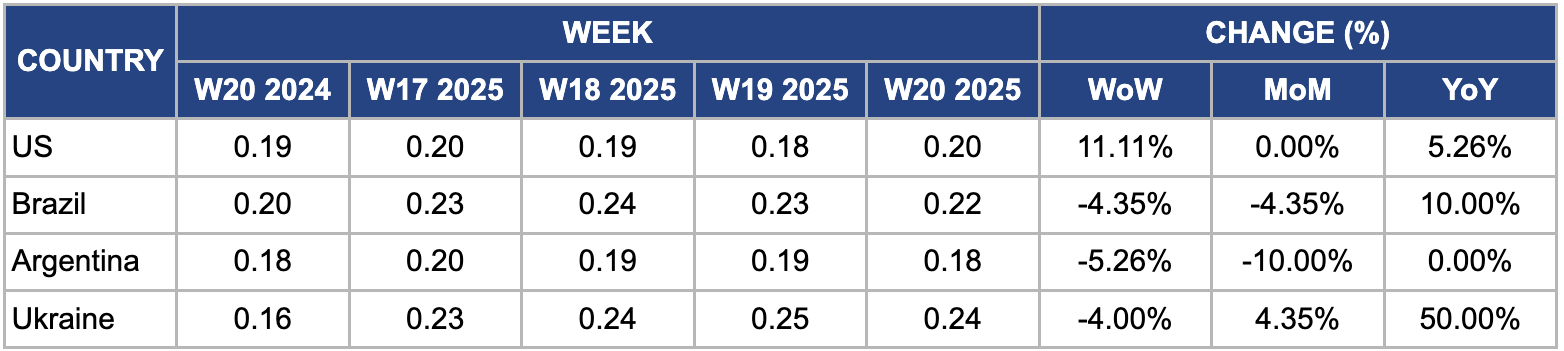

United States

In W20, US corn prices rose to USD 0.20 per kilogram (kg), marking an 11.11% increase week-on-week (WoW) and a 5.26% rise YoY. This price gain was mainly driven by delayed planting caused by excessive rainfall and saturated soil conditions in critical Corn Belt states like Iowa, Illinois, and Nebraska, where planting progress lagged significantly behind the five-year average.. These delays have raised concerns about potential yield reductions and crop quality issues later in the season. Moreover, sustained strong export demand from key markets such as China and Mexico has tightened domestic supplies. These factors, planting delays, weather challenges, and robust export demand have put upward pressure on US corn prices during this period.

Brazil

In W20, Brazil's wholesale maize prices decreased 4.35% WoW and 4.35% month-on-month (MoM) to USD 0.22/kg. The price drop is due to improved weather conditions in key maize-producing regions, such as Mato Grosso and Paraná, which alleviated concerns over potential crop yield losses. The better weather allowed for faster harvesting and an increase in supply. Moreover, there has been a slowdown in demand from the livestock and ethanol sectors, as some industries have adjusted their consumption due to the ongoing economic situation. As the market starts to see more availability of maize from the 2024/25 Safrinha crop, pressure from higher supply has led to a price drop.

Argentina

In W20, Argentine maize prices declined 5.26% WoW and 10% MoM to USD 0.18/kg. This price drop was due to recent weather improvements in key growing areas such as Buenos Aires, Entre Ríos, and Santa Fe, where substantial rainfall eased earlier supply concerns. The favorable weather boosted expectations for better crop yields, reducing drought-related fears and improving the outlook for the upcoming harvest. Furthermore, increased competition from key maize exporters like Brazil and the US, which are projecting larger harvests with competitive pricing, added further downward pressure on Argentine maize prices.

Ukraine

In W20, Ukrainian wholesale maize prices declined 4% WoW, dropping to USD 0.24/kg from USD 0.25/kg in W19. This price decrease was mainly due to improved weather conditions in key growing regions, which have supported crop development and alleviated earlier concerns about potential yield losses. According to recent agricultural reports, Ukraine’s maize harvest area for 2025 will increase slightly by around 2% YoY, contributing to higher production forecasts of approximately 39 mmt. Furthermore, stabilization and increased capacity in export corridors, mainly through Black Sea ports, have increased maize shipments, improving supply availability on the market. The combination of improved supply prospects and steady demand from traditional export markets, such as the EU and Egypt, exerted downward pressure on maize prices, resulting in the observed W20 decline.

3. Actionable Recommendations

Enhance Planting and Crop Resilience Strategies Using Weather-Resilient Corn Hybrids

Due to excessive rainfall and delayed planting in key Corn Belt states such as Iowa, Illinois, and Nebraska, the US should invest more in weather-resilient farming techniques and infrastructure. This includes expanding drainage systems, adopting drought- and flood-tolerant corn hybrids such as DEKALB DKC63-87, Pioneer P1197AM, and Syngenta NK® S44-L5, which have demonstrated strong performance under variable moisture conditions. Moreover, improving real-time weather monitoring and advisory services for farmers will enable timely management decisions. Strengthening these resilience measures will help reduce yield losses and maintain crop quality despite adverse weather conditions, ensuring the US maintains its leading production and export capacity amid climate variability.

Strengthen Export Infrastructure and Market Diversification Amid Growing Competition

As a key corn supplier to the EU and Türkiye, Ukraine should focus on further stabilizing and expanding export corridors, mainly through Black Sea ports, to handle increased production forecasts and growing export volumes. Investing in port capacity, logistics efficiency, and alternative routes will minimize bottlenecks and enhance competitiveness. Simultaneously, Ukraine should explore diversifying its export markets beyond the EU and Türkiye to mitigate risks from competition, especially from the US, and build resilience against geopolitical and trade uncertainties.

Expand Maize Cultivation Areas and Improve Yield in Key Provinces

Indonesia’s forecasted 12.88% YoY production increase presents an opportunity to capitalize on expanding harvested area from 0.29 million ha to 0.58 million ha by mid-2025. To maximize output, Indonesia should prioritize providing technical support, improved seed varieties, and access to fertilizers and machinery in the ten provinces driving this growth. Furthermore, implementing farmer training programs on best agronomic practices and pest management can boost yields and sustain long-term production growth, helping Indonesia meet rising domestic demand and reduce reliance on imports.

Sources: Tridge, AgroLink, Sinor, UkrAgroConsult