In W20 in the orange landscape, some of the most relevant trends included:

- Argentina faces logistical constraints, high production costs, and restrictive tariffs that limit its orange exports, despite rising global demand and favorable growing conditions for varieties such as Salustiana and blood oranges.

- Brazil’s 2025/26 orange harvest is projected to increase by 36.2%, driven by better climate, improved orchard management, and rising productive trees across major varieties.

- Egypt’s 2024/25 orange season ends early with a 15% export volume drop due to lower production, increased local demand, and geopolitical disruptions causing a price surge.

- Morocco’s orange exports remain stable despite a global shortage, but pest and climate issues have halved export volumes and kept prices low amid weak international demand.

1. Weekly News

Argentina

Argentina’s Orange Industry Faces Logistical and Market Challenges Despite Growing Demand

Despite favorable natural conditions and more than 40 years of export experience, Argentina’s citrus industry continues to face significant structural challenges. High internal costs, limited infrastructure, and geographic distance from major global shipping routes contribute to logistical inefficiencies. These factors and low export volumes often result in shipping lines bypassing the country. Additionally, phytosanitary barriers and tariffs restrict access to key markets such as the United States and Europe, limiting Argentina’s competitiveness compared to larger exporters like South Africa and Egypt. While the country will produce its traditional orange varieties in 2025, including Salustiana, Navel, Midknight, and Valencia, it is also trialing blood oranges as part of a longer-term diversification strategy.

In the short term, a global orange shortage caused by reduced production in the US and Brazil has increased demand for early-season fresh fruit, offering a promising, but difficult to fully capitalize on, opportunity for Argentina. In response, the industry prioritizes collective negotiations with shipping companies and targets niche markets where its high-quality, consistent citrus can stand out.

Brazil

Brazil’s 2025/26 Orange Harvest Forecast to Rise in 2025/26

Brazil’s 2025/26 orange harvest in the Citrus Belt, which includes São Paulo and Triângulo/Sudoeste Mineiro, is projected to reach 314.6 million boxes. This represents a 36.2% increase from the previous season’s 230.87 million boxes. This growth is driven by favorable climate conditions that boosted the second flowering and improved orchard management practices. Additionally, there was a 7.5% increase in productive trees, totaling 182.7 million across 362 thousand hectares (ha). Average productivity is expected to rebound to 869 boxes/ha and 1.72 boxes per tree, an improvement from last season’s lower yields.

Egypt

Egypt’s Orange Season Ends Early Due to Supply Challenges and Price Surge

Egypt’s 2024/25 orange season is ending earlier than usual, with most packing stations completing their final shipments. Export volumes this season dropped by 15% year-on-year (YoY) due to lower production, rising local demand due to expanding orange concentrate factories, and ongoing disruptions linked to the Red Sea crisis. Following the Eid al-Fitr holiday in Apr-25, orange prices surged to a record high of USD 800 per ton before stabilizing at elevated levels. In the previous season, Egypt’s citrus exports surpassed 2 million tons, including 1.93 million tons of oranges, despite a slight drop in average export prices from USD 497 to USD 474 per ton.

Morocco

Moroccan Orange Exports Unaffected by Global Shortage Despite Seasonal and Quality Challenges

Morocco’s orange export season is progressing despite a global shortage caused by early season endings in Egypt and Spain, with no notable rise in demand or prices. The Moroccan season is relatively short, peaking mainly in November and briefly again in February. By then, ample and often cheaper supplies from Spain and Egypt remained available. However, pest infestations and climate-related fruit damage have halved exportable volumes. While current demand favors Navel oranges, Morocco’s late-season variety, Maroc Late, sees limited interest outside of some demand in Russia and North America. Although some exporters reported a slight demand increase after Egypt’s early-season closure, importers have pressured prices downward, reducing export appeal. As a result, Moroccan orange prices remain low domestically, showing that the international shortage has not significantly affected Morocco’s supply or market conditions this season.

United States

USDA Forecasts 2024/25 Florida Orange Production With Significant Seasonal Decline

The United States Department of Agriculture (USDA) projects Florida’s 2024/25 orange production at 11.6 million boxes. This represents a less than 1% increase from the previous forecast but a 36% drop compared to last season’s final output. This total includes 4.58 million boxes of non-Valencia oranges, such as early, mid-season, and Navel varieties, with Navel oranges comprising about 2%. It also includes 7.05 million boxes of Valencia oranges, whose estimate was slightly raised based on harvest and processor surveys showing 99% of Valencia rows already harvested. Other citrus categories remain stable, with grapefruit at 1.3 million boxes, lemons at 600 thousand boxes, and tangerines and mandarins at 400 thousand boxes. The USDA notes a forecast reliability margin of approximately 2.2%, consistent with historical accuracy in seasons unaffected by hurricanes.

California’s 2025 Orange Season Boosted by Demand and Supply Strategy

California’s 2025 orange season is seeing strong demand for Navel and Valencia oranges, surpassing early projections. This is due to improved fruit quality and an early start driven by warmer weather that boosted sugar levels and lowered acidity. While growers aim to stretch supplies to meet strong and steady demand, the season is expected to conclude on schedule or slightly early, depending on yield and quality.

California producers supplement the local supply with imports from Morocco, Chile, Peru, and Argentina to ensure year-round availability. However, existing US tariffs, ranging from 10% to 30% depending on origin and product, continue to impact pricing. Orange prices have increased modestly since the start of the season but remain slightly below last year’s levels due to higher yields and active promotions. Valencia's lemons, mandarins, and specialty oranges continue to show strong supply, though Navel and organic orange volumes are expected to decline in the coming months. Despite a seasonal shift toward summer fruits, citrus remains a key staple for US consumers, requiring strategic planning to manage weather variability and maintain consistent quality.

2. Weekly Pricing

Weekly Orange Pricing Important Exporters (USD/kg)

Yearly Change in Orange Pricing Important Exporters (W20 2024 to W20 2025)

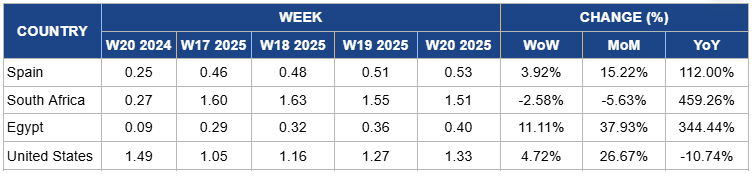

Spain

In Spain, orange prices in W20 rose by 3.92% WoW to USD 0.53 per kilogram (kg), with a 15.22% month-on-month (MoM) increase and a substantial 112.00% YoY surge. This significant price escalation is due to reduced citrus yields because of adverse weather conditions, including extreme heat and drought, particularly in key producing regions such as Andalusia. These climatic challenges have constrained the supply of oranges, thereby exerting upward pressure on prices. Additionally, rising production costs, encompassing energy, labor, and plant protection expenses, have further contributed to the price increase. Despite the high prices, there remains a steady demand for Spanish oranges in both domestic and export markets, which continues to support the elevated price levels.

South Africa

South Africa's orange prices dropped by 2.58% WoW to USD 1.51/kg in W20, reflecting a 5.63% MoM decrease. This decline is due to increased local supply resulting from favorable weather conditions, leading to higher production volumes. Additionally, a shift in consumer preferences and quality concerns has reduced demand, contributing to the price drop. However, YoY prices surged by 459.26%, driven by a significant reduction in global orange production, particularly in major producing countries like Brazil, where HLB disease and adverse weather conditions have severely impacted yields. This global supply shortage has increased demand for South African oranges in international markets, thereby elevating prices compared to the previous year.

Egypt

In Egypt, orange prices increased by 11.11% WoW to USD 0.40/kg in W20, with a 37.93% MoM rise and a substantial 344.44% YoY surge. This sharp escalation is due to a significant reduction in orange production, which declined by 12% in the 2024/25 season because of adverse weather conditions during flowering and fruit set, leading to a 15% decrease in exports. Additionally, heightened demand from the juice processing industry, spurred by global shortages and rising juice prices, has diverted more oranges from the fresh market, tightening supply and elevating prices. Logistical challenges, including disruptions in Red Sea shipping routes, have further constrained exports, intensifying the supply-demand imbalance.

United States

US orange prices increased by 4.72% WoW to USD 1.33/kg in W20, marking a 26.67% MoM rise. This uptick is primarily due to a significant reduction in domestic orange production, particularly in Florida, where output has plummeted by 30% for the 2024/25 season, the lowest level since before World War II. The production decline is due to the devastating impact of hurricanes and the persistent spread of citrus greening disease, which has severely affected the state's citrus groves. Additionally, trade tensions have led to increased tariffs on orange imports, further constraining supply and contributing to higher prices. However, YoY prices have dropped by 10.74%, reflecting a decrease from the record-high prices experienced in late 2024. While this decline is partly influenced by reduced national consumer demand due to high prices and diminished juice quality, it is important to note that demand in California has been on the rise, partly offsetting the overall consumption drop and suggesting regional variation in market dynamics.

3. Actionable Recommendations

Prioritize Grading and Juice Contracts to Maximize Returns

Orange producers in Egypt, Spain, South Africa, and Morocco should actively sort harvests into fresh-market and juice-grade batches early in the season to respond to tight supply and rising juice demand. Growers can secure pre-harvest contracts with juice processors at premium prices, especially in regions like Egypt, where processing demand is surging. At the same time, exporters in Spain and Morocco can focus on top-grade fruit on fresh markets with higher margins, especially amid logistics delays. This dual-channel strategy ensures optimized returns despite lower yields and global supply stress.

Enhance Pest Management and Market Diversification

Moroccan orange producers should strengthen pest control measures and adopt climate-resilient practices to protect yields, as production losses are cutting exportable volumes. For example, integrating biological pest control and improving irrigation can reduce fruit damage. Producers should also diversify export markets beyond traditional destinations like Russia and North America by targeting emerging markets with growing demand for late-season varieties like Maroc Late. Collaborating with exporters to develop marketing campaigns that highlight the unique qualities of Moroccan oranges can help increase appeal and counteract price pressure from importers.

Sources: Tridge, Al Mansi, Cap Growers, Citrus Industry, FAMA, Freshplaza, USDA