In W20 in the tomato landscape, some of the most relevant trends included:

- Weather-related planting delays in Europe are disrupting tomato production timelines in key countries like France, Spain, and Italy. Spain faces the most severe impact, with a 22.5% YoY production drop forecast for 2025 due to prolonged rainfall and cold weather, while other producers like Portugal and Greece report delays without adjusting forecasts.

- Tomato prices are under pressure in multiple regions due to supply imbalances. Prices dropped in W20, with Spain experiencing delays in planting and Morocco facing government imposed restrictions. In contrast, France and Türkiye experienced strong YoY price growth driven by supply constraints and input cost inflation.

- Trade tensions between the US and Mexico are destabilizing the North American tomato market. The US will impose a 17.09% anti-dumping duty on Mexican tomatoes in Jul-25. These measures threaten supply chains, raise US consumer prices, and have already triggered a 7.8% YoY drop in Mexico’s tomato export revenues.

- Structural challenges in US agriculture are prompting crop destruction. Rising labor costs, immigration constraints, and market disruptions are forcing South Florida growers to leave tomatoes unharvested, exacerbating regional supply instability.

1. Weekly News

European Union

Wet Spring Delays Tomato Planting Across Europe, Impacting Harvest Forecasts

According to the World Processing Tomato Council (WPTC), tomato planting across Europe has been delayed by wet spring conditions, particularly in France, Italy, and Spain, potentially affecting harvest timelines. While France's 2025 processing forecast remains at 173,000 metric tons (mt), Spain anticipates lower output than its earlier 2.6 million metric tons (mmt) projection. Italy's forecast stands at 5.6 mmt, despite rain-related setbacks. Other countries, including Portugal, Hungary, and Greece, also report delays but have not revised their forecasts.

Belgium

Belgian Tomato Prices Remain Below Five-Year Average Following Continued Decline

Tomato prices in Belgium remain weak, staying below the five-year average, according to data from the Belgian Federation of Horticultural Cooperatives (VBT). As of W19, vine tomatoes averaged USD 0.79 per kilogram (EUR 0.696/kg), while bulk tomatoes fell to USD 0.65/kg (EUR 0.579/kg), marking a further decline of over USD 0.11/kg (EUR 0.10/kg).

Iran

Tomatoes Rank Second in Iran's Agricultural Exports with USD 233 Million in Revenue

In the Iranian calendar year 1403 (ending March 20), Iran exported tomatoes worth USD 233 million, making them the country's second most valuable agricultural export after pistachios, according to the Islamic Republic of Iran Customs Administration (IRICA). Tomatoes were among the key drivers of the 29% annual growth in agricultural export value, which totaled USD 5.2 billion.

Mexico

US Tariff on Mexican Tomatoes Sparks Trade Tensions and Economic Fears

The United States (US) will impose a 17.09% anti-dumping duty on imported Mexican tomatoes starting July 14, following its withdrawal from the 1996 Tomato Suspension Agreement. This decision has prompted strong opposition from Mexican growers and US trade partners, citing risks to cross-border agricultural trade, supply chain stability, and consumer prices.

Mexico exports over half of its tomato production, worth more than USD 3 billion annually, to the US, supplying nearly 70% of its fresh tomato market. Producers warn the tariff will reduce tomato variety and raise costs for US consumers, while threatening jobs and regional economies reliant on exports, particularly in Baja California, where 80% of tomatoes are shipped to the US. Despite diplomatic efforts led by Mexican officials and industry representatives in Washington, no resolution has been reached. Mexico has signaled potential retaliatory tariffs on US poultry and pork, further escalating trade tensions.

Russia

Tomato Prices Fall 4.6% WoW in Novgorod Region

In Russia's Novgorod Region, the average retail price of tomatoes declined by 4.6% week-on-week (WoW) in W18, reaching USD 3.89/kg (RUB 309.87/kg), according to Novgorodstat. This marks the most notable drop among key vegetable items during Apr-25, indicating downward pressure in the fresh produce segment.

United States

Florida Tomato Industry Suffers as Tariff Threats and Labor Shortages Force Crop Destruction

Thousands of acres of tomatoes in South Florida are being destroyed due to rising labor costs, market disruptions from US tariff threats, and immigration policies. Farmers report it is now more cost-effective to plow under-ripe tomatoes than to harvest them, with current market prices falling far below the breakeven point.

Despite no formal tariff on Mexican tomatoes under the United States–Mexico–Canada Agreement (USMCA), the threat of import duties led to a surge in Mexican exports earlier in the year, flooding the US market and decreasing prices. To protect domestic growers, the US plans to impose a 20.91% duty on Mexican tomatoes beginning in Jul-25, replacing a 2019 agreement on minimum pricing. The move is expected to increase costs for US consumers. Labor shortages, driven by stricter immigration policies, have further hampered harvesting efforts. The instability has had broader effects on Florida agriculture and may require federal intervention.

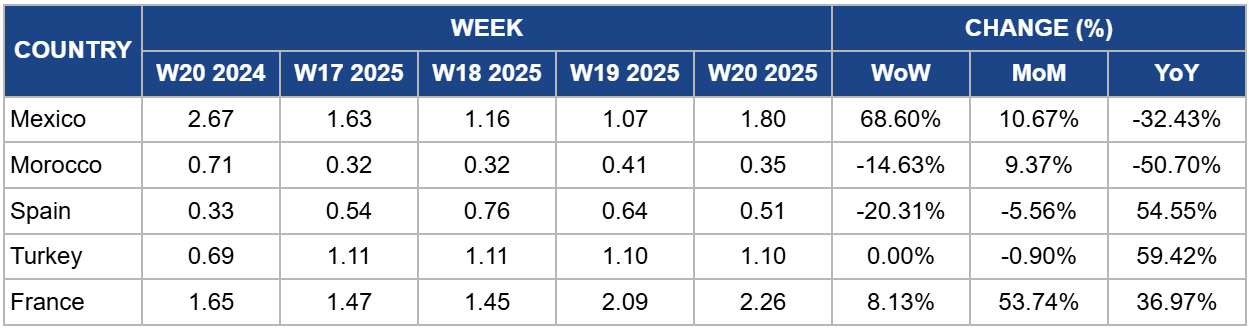

2. Weekly Pricing

Weekly Tomato Pricing Important Exporters (USD/kg)

Yearly Change in Tomato Pricing Important Exporters (W20 2024 to W20 2025)

.png)

Mexico

Mexico's tomato prices surged to USD 1.80/kg in W20, experiencing a sharp 68.60% WoW increase, yet remain 32.43% below last year's USD 2.67/kg. This volatility stems largely from ongoing trade uncertainties, notably the US decision to impose a 17.09% anti-dumping duty on Mexican tomatoes starting July 14, 2025.

The tariff dispute has already impacted Mexican agricultural exports, causing a 3.2% decline overall and a notable 7.8% annual drop in tomato export revenues to USD 859 million in early 2025. Given that over half of Mexico's tomato production is exported primarily to the US, where Mexican tomatoes account for nearly 70% of fresh tomato supply, these trade barriers threaten both market stability and regional economies, especially in Baja California, which relies heavily on exports.

Morocco

In W20, Morocco’s tomato prices fell to USD 0.35/kg, marking a 14.63% WoW decline and a steep 50.70% drop year-on-year (YoY) from USD 0.71/kg. This significant decrease is primarily due to government-imposed export quotas that cut daily shipments to Europe by 90% for round and grape tomatoes. The policy aims to boost domestic supply and curb inflation ahead of peak holiday demand. The resulting oversupply has driven prices down sharply, highlighting how regulatory measures can rapidly influence market conditions. Continued export restrictions may keep prices subdued locally but could tighten supply in European markets, potentially leading to price adjustments.

Spain

In W20, Spain's tomato prices declined 20.31% WoW to USD 0.51/kg, reflecting pressure from delayed planting caused by wet spring conditions. The WPTC reports significant planting delays, particularly in Spain, which may disrupt harvest schedules. Furthermore, Spain's tomato production is projected to fall sharply by 22.5% YoY, from 3.1 mmt in 2024 to 2.4 mmt in 2025. This decline results from adverse weather, including cold and heavy rains in key growing regions like Andalusia and Extremadura, impacting yields and delaying planting. Additionally, growing competition from lower-cost producers such as Morocco and Türkiye is eroding Spain’s market share. Despite these challenges, Spain’s tomato prices increased by 54.55% YoY from USD 0.33/kg, indicating that supply constraints and weather-related disruptions have contributed to higher prices compared to the previous year.

Türkiye

In W20, Türkiye's tomato prices held steady at USD 1.10/kg, showing no weekly change but marking a significant 59.42% YoY increase from USD 0.69/kg. This rise reflects sustained cost pressures, including elevated input costs for fertilizers, labor, and energy. The seasonal harvest from key regions like Antalya and Mersin temporarily eased supply constraints, supporting short-term price stability. However, strong domestic consumption and steady export demand, especially from nearby markets, continue to support elevated price levels.

France

In W20, France's tomato prices rose to USD 2.26/kg, marking an 8.13% WoW and a 53.74% month-on-month (MoM) increase from USD 1.47/kg. The surge is primarily attributed to delayed spring harvests caused by cooler-than-average temperatures and intermittent rainfall, which constrained domestic supply. Rising input costs and strong demand from local consumers and neighboring countries further exacerbated the upward pressure. With weather-related planting delays continuing to limit short-term availability, prices may remain elevated in the near term, particularly if external demand persists and domestic output remains subdued.

3. Actionable Recommendations

Diversify Export Destinations Amid US–Mexico Trade Tensions

Given the increasing uncertainty surrounding US tariffs on Mexican tomatoes and the resulting price volatility, Mexican producers and exporters should prioritize diversifying export destinations beyond the US. Strategic expansion into markets in Canada, the EU, and the Middle East can help stabilize revenue streams and reduce exposure to single-market risks. Investment in cold chain logistics and compliance with international phytosanitary standards will be critical to accessing premium segments in these regions.

Leverage Delayed European Harvests to Boost Export Competitiveness

With weather-induced planting delays in major European producers like Spain, France, and Italy potentially tightening European Union (EU) supply, countries such as Morocco, Türkiye, and Iran should capitalize on this window by increasing short-term exports to Europe. Enhancing coordination with EU importers, accelerating quality certification processes, and aligning export volumes with demand surges can strengthen market position and offset domestic price declines.

Invest in Value-Added Processing and Market Segmentation

Producers facing price pressures, such as those in Belgium and Florida, should invest in value-added processing (e.g., tomato paste, sauces, or organic certified products) to enhance profitability and reduce waste from surplus or unharvested crops. Additionally, segmenting markets based on consumer preferences (e.g., vine-ripened, heirloom, or sustainably grown varieties) can help tap into higher-value channels and buffer against commodity price swings.

Sources: Tridge, SPECAGRO, HortiDaily, Tehran Times, Fresh Plaza, Reason, Publimetro