.jpg)

In W20 in the wheat landscape, some of the most relevant trends included:

- Global wheat production is forecasted to reach a record 808.52 mmt in 2025/26, driven mainly by significant increases in the EU and India. Meanwhile, Russia’s outlook has improved slightly, while declines are expected in Ukraine and Kazakhstan.

- Severe drought in Mexico is causing a sharp reduction in wheat planting, with a 76% cut in planted area, forcing farmers to shift to less water-intensive crops.

- Morocco is reducing wheat imports due to better domestic harvests and diversified sourcing.

- Russian wheat prices remained stable WoW due to government price floors, while US prices declined WoW amid favorable crop conditions and French prices dropped WoW due to increased supply and weaker demand.

1. Weekly News

Global

Global Wheat Production to Hit Record 808.52 MMT in 2025/26 MY

The United States Department of Agriculture (USDA) projected a record-high global wheat harvest of 808.52 million metric tons (mmt) for the 2025/26 marketing year (MY), representing an 11% increase from the previous season. This growth is mainly due to the European Union (EU), where wheat production will reach 136 mmt, an 11.4% rise thanks to improved weather, expanded sowing areas, and better yields. With this production boost, EU wheat exports will increase significantly from 26.5 mmt in MY 2024/25 to 34 mmt in MY 2025/26.

Northern France, Germany, and Poland experienced dry conditions, while the Balkans benefited from favorable rainfall during the growing season. Meanwhile, Russia's wheat outlook has slightly improved, but declines are expected in Ukraine and Kazakhstan.

Australia

Australia Wheat Exports in Mar-25 Declined 17% YoY

In Mar-25, Australia exported 2.12 mmt of wheat and durum, a slight increase from Feb-25 but marking a 17% year-on-year (YoY) decline. Containerized exports were primarily directed to Thailand, Malaysia, and Indonesia, while bulk shipments went mainly to Indonesia, Thailand, and China. Moreover, wheat exports in Apr-25 are expected to rise to 2.4 mmt.

India

India Confirms Record Wheat Harvest Forecast at 115.3 MMT for 2024/25

The Indian agriculture ministry has reaffirmed its forecast of a record wheat harvest for the 2024/25 crop year, maintaining its Mar-25 estimate of 115.3 mmt, 2% higher than the 113.3 mmt harvested in 2023/24. The Agriculture Minister announced on May 12 that favorable weather conditions across most wheat-growing regions supported the smooth progress of the harvest. While harvesting is complete in Madhya Pradesh, Haryana, Rajasthan, and Gujarat, it continues in Punjab, Uttar Pradesh, and Bihar. As of April 1, government wheat stocks reached 11.8 mmt, well above the target of 7.46 mmt and over 4 mmt higher than in 2024, indicating high domestic availability.

Mexico

Mexico’s Wheat Production Plummets for 2025/26 Due to Severe Drought and Irrigation Cuts

According to the USDA’s May-25 report, Mexico’s wheat production for the 2025/26 season will decline sharply due to severe drought, particularly in Sonora, the country’s key wheat-producing state. The persistent water shortages have led to a dramatic 76% reduction in planted wheat areas, severely limiting cultivation. In response, authorities encouraged farmers to switch to less water-dependent crops such as barley and safflower. While some agricultural land remains unused, drought has severely constrained productive activity across most regions, significantly reducing vegetation in wheat-growing zones. Consequently, 92% of Mexico’s cereal output will be winter wheat, highlighting the strain on national grain production.

Morocco

Morocco Cuts Wheat Imports Amid Improved Harvests, Boosts Maize Imports to Support Poultry Sector

Morocco will reduce its wheat imports to 6.7 mmt for the 2025/26 season, down 200 thousand metric tons (mt) from the previous year, reflecting improved domestic harvests and strategic stock management despite persistent climate challenges. In contrast to more import-dependent regional peers like Egypt, Morocco is moving toward greater grain self-sufficiency while maintaining balanced sourcing from major exporters such as France, Russia, and Kazakhstan. This diversification enhances Morocco’s procurement resilience amid intensifying global competition, with world wheat output forecast to hit a record 808.52 mmt. As Russia pushes to expand its presence in North Africa and France seeks to maintain its foothold, Morocco skillfully leverages bilateral negotiations, tenders, and partnerships to safeguard its interests.

2. Weekly Pricing

Weekly Wheat Pricing Important Exporters (USD/kg)

Yearly Change in Wheat Pricing Important Exporters (W20 2024 to W20 2025)

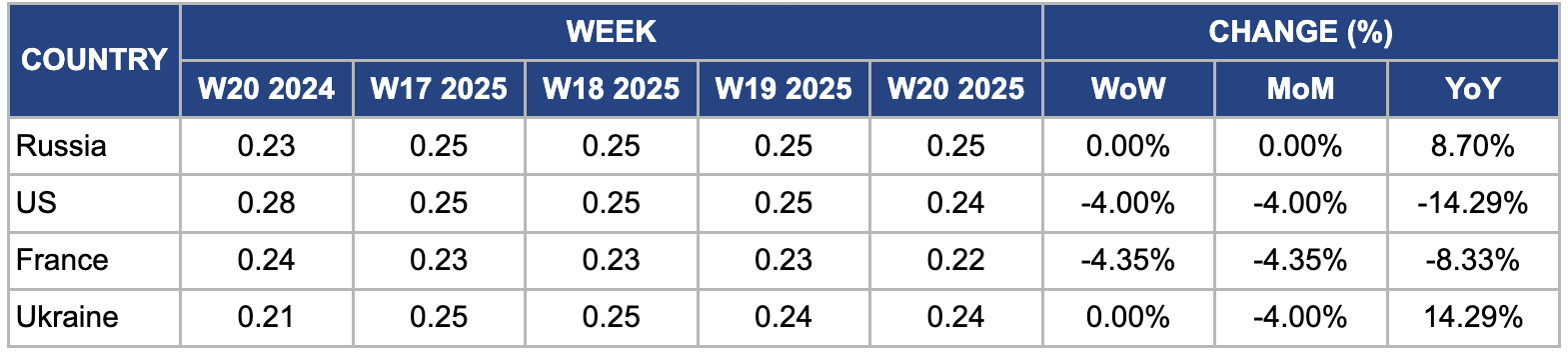

Russia

In W20, Russian FOB wheat prices held steady at USD 0.25 per kilogram (kg) for the fourth consecutive week. This stability is mainly due to the Russian government's minimum export price floor set at USD 250/mt, aimed at limiting excessive exports and managing domestic inflation. The positive outlook for the 2024/25 Russian wheat harvest, supported by favorable weather and improved yields in key regions like Krasnodar and Rostov, has further reinforced price resilience. Despite global market fluctuations, regulatory measures and export quotas continued stabilizing Russia’s wheat export market.

United States

In W20, United States (US) FOB wheat prices fell 4% both week-on-week (WoW) and month-on-month (MoM), reaching USD 0.24/kg, marking a 14.29% decline YoY. The 2025 US winter wheat crop has made steady progress under generally favorable weather conditions, supporting expectations of higher supply and contributing to bearish market sentiment. According to the National Agricultural Statistical Service (NASS), the condition of US winter wheat improved notably by May 11, with 9% rated as excellent (up from 7% a week earlier and 8% last year) and 46% as good (up from 44% and 42%, respectively). Moreover, the USDA forecasts a 2.4% YoY increase in US 2025 winter wheat production, reaching 1.382 billion bushels despite a slight reduction in harvested area. This production rise is due to an expected average yield improvement to 53.7 bushels per acre, up from 51.7 bushels per acre in 2024, reflecting better-growing conditions and improved crop management practices. This higher yield will offset the smaller acreage, supporting overall production growth.

France

In W20, wholesale wheat prices in France decreased by 4.35% WoW and MoM to USD 0.22/kg. This price decline is primarily due to increased supply amid the ongoing harvest, with France’s wheat production forecast at approximately 36 mmt in 2025, contributing to abundant market availability. The higher supply eased previous tightness in the market, putting downward pressure on prices. Moreover, weaker demand from domestic mills and export markets, especially as global buyers showed caution amid competitive offers from Russia and Ukraine, further limited price gains. According to FranceAgriMer’s Apr-25 trade data, French wheat exports slowed slightly by around 5% MoM, reflecting softer international demand that compounded the price decline.

Ukraine

In W20, Ukrainian wheat prices remained unchanged WoW but declined 4% MoM to USD 0.24/kg. The new harvest increased supply, causing the monthly price drop. Better weather conditions in key growing regions improved crop development, which raised availability. At the same time, traditional buyers reduced their export demand due to global market uncertainties and competition from other wheat exporters, putting downward pressure on prices. Rising supply combined with cautious demand led to a moderate monthly price decline.

3. Actionable Recommendations

Enhance Regional Trade Diversification and Procurement Resilience

Major wheat exporters such as the EU, Russia, and the US should proactively pursue market diversification by forging strategic trade partnerships and promoting value-added wheat products. With record-high global wheat production expected in 2025/26, competition will intensify. Countries like Morocco are already securing procurement through diversified import sources and bilateral agreements. Exporters can build on this model by expanding into underserved markets in Africa and Southeast Asia, where demand is growing. Moreover, focusing on higher-quality or specialty wheat varieties (e.g., high-protein or organic wheat) can differentiate products and maintain price competitiveness in a market facing downward pressure due to abundant global supply.

Strengthen Domestic Support Systems in Drought-Affected Regions

Countries experiencing production declines, such as Mexico, must enhance support mechanisms for farmers facing climate stress, particularly in key regions like Sonora. The 76% reduction in wheat-planted areas due to severe drought highlights the urgent need for adaptive strategies. Governments should scale up incentives for crop diversification, invest in drought-resilient wheat research, and provide financial assistance for farmers transitioning away from water-intensive crops. Infrastructure investments like efficient irrigation and water storage systems can further mitigate future production risks and sustain rural economies vulnerable to climate extremes.

Implement Stock Management Reforms and Buffer Strategies

India and Morocco should optimize their stock management and distribution systems to balance local supply with global price dynamics. India’s above-target wheat stock levels, which are 11.8 mmt as of April 1, present an opportunity to improve buffer stock management and avoid market gluts that can suppress farmgate prices. Authorities should periodically release surplus stock to stabilize market prices, prevent spoilage, and ensure food security. Furthermore, building flexible export policies can help absorb domestic surpluses when international prices are favorable, strengthening the country’s role in global markets while protecting farmer interests.

Sources: Tridge, Agro Link, Sinor, UkrAgroConsult