W21 2025: Banana Weekly Update

In W21 in the banana landscape, some of the most relevant trends included:

- Colombia aimed to reach USD 1 billion in banana export revenue in 2024, shipping around 106 million boxes primarily to the EU, UK, and US, while monitoring tariff risks and regional competition.

- Costa Rica maintains a positive banana export outlook to the US despite concerns over a potential 10% tariff, citing inelastic demand and stable consumer consumption patterns.

- The Dominican Republic is experiencing a banana industry crisis, with a 40% drop in export revenue in 2023 due to climate issues, labor shortages, and the loss of undocumented Haitian workers.

- South Africa clarified that it never banned banana imports from Tanzania and is conducting a pest risk analysis to determine conditions for future market access.

1. Weekly News

Colombia

Colombia’s Banana Industry Targets USD 1 Billion in 2024

Colombia’s banana industry is the country's third-largest agricultural export industry after coffee and flowers. It is targeting USD 1 billion in export revenue in 2024 by shipping approximately 106 million boxes. About 85% of exports are headed to the European Union (EU) and the United Kingdom (UK), and 15% to the United States (US). However, the industry remains exposed to tariff changes in key markets, especially as countries like Ecuador, Costa Rica, and Guatemala may gain pricing advantages. With 80% of exports coming from the Magdalena region, industry stakeholders closely monitor trade developments. Colombia's banana sector is characterized by high labor formality, supporting over 19 thousand formal jobs and involving 600 small producers. Efficient logistics, including dedicated fleets from the port of Santa Marta, help sustain reliable export flows to the US.

Costa Rica

Costa Rica Defends Banana Export Outlook Despite US Tariff Concerns

Costa Rica’s National Banana Corporation (CORBANA) has contested forecasts suggesting a new 10% reciprocal US tariff would reduce banana exports to the US by 18% in 2025. CORBANA argues that the analysis lacks detailed data and overstates the impact, given bananas’ relatively inelastic demand. Other major suppliers like Ecuador face the same tariff, and US consumers maintain strong demand, with per capita consumption at 12.1 kilograms (kg) in 2023. Although recent export volumes have declined due to adverse weather, CORBANA believes Costa Rican bananas remain competitive. Importers are absorbing the additional cost, and the fruit continues to hold a stable position in the US market.

Dominican Republic

Dominican Republic’s Banana Industry in Crisis Due to Labor Shortages and Climate Challenges

The Dominican Republic’s banana industry is facing a severe crisis, with export revenues falling 40% from USD 323 million in 2022 to USD 202 million in 2023. Contributing factors include climate impacts, pest outbreaks, and a sharp decline in labor availability. The deportation of undocumented Haitian immigrants, who made up a significant portion of the labor force, has intensified the challenge. Although global demand for organic bananas remains strong, local producers report being unable to meet it under current conditions. Responsible for 90% of national production, the Valverde province is the epicenter of the crisis, which affects approximately 30 thousand producers and their families and threatens the long-term viability of the industry.

South Africa

South Africa Clarifies Status of Banana Imports from Tanzania

South Africa has clarified that it never banned banana imports from Tanzania, correcting recent misreports of a trade suspension. According to the Department of Agriculture, Land Reform, and Rural Development, Tanzanian bananas have never had formal market access, so claims of a ban are incorrect. The two countries maintain active agricultural trade relations, and Tanzania officially requested banana export access on Feb-25. South Africa is currently conducting a pest risk analysis to determine phytosanitary requirements. Imports will begin once both governments finalize the regulatory framework by international biosecurity standards.

2. Weekly Pricing

Weekly Banana Pricing Important Exporters (USD/kg)

Yearly Change in Banana Pricing Important Exporters (W21 2024 to W21 2025)

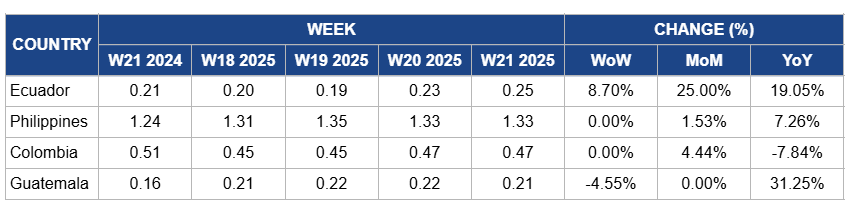

Ecuador

In W21, Ecuador's banana prices rose by 8.70% week-on-week (WoW) to USD 0.25/kg, with a 25% month-on-month (MoM) and 19.05% year-on-year (YoY) increase. The price rise is driven by reduced production due to adverse weather, high global demand from Europe and Asia, and logistical challenges, including container shortages. Additionally, Ecuador’s higher minimum support price for bananas in the 2024/25 season has pushed prices upward.

Philippines

In W21, banana prices in the Philippines remained stable WoW at USD 1.33/kg, with a 1.53% MoM and a 7.26% YoY increase. This upward trend is due to reduced domestic supply caused by the persistent spread of Fusarium Wilt Tropical Race 4 (Foc TR4), which has significantly affected banana plantations, particularly in Mindanao. Additionally, rising production costs, including higher expenses for disease management, labor, and inputs, have contributed to the price increase. Despite these challenges, demand from key export markets such as Japan and South Korea remains steady, supporting price stability. However, the Philippines faces growing competition from countries like Vietnam, which benefit from lower tariffs and expanding production, potentially impacting future market share.

Colombia

In W21, Colombia's banana prices held steady WoW at USD 0.47/kg, marking a 4.44% MoM increase driven by sustained export demand from key markets like the US and Europe, particularly as seasonal consumption patterns supported higher volumes. However, prices declined by 7.84% YoY due to ongoing logistical challenges, including infrastructure inefficiencies and elevated phytosanitary costs associated with managing Foc Tr4. These factors have increased production expenses, while international market prices have remained relatively flat, squeezing margins for Colombian producers. Despite these pressures, the sector advocates for fairer pricing structures to reflect rising operational costs and ensure long-term sustainability.

Guatemala

In W21, banana prices in Guatemala decreased by 4.55% WoW to USD 0.21/kg, with no MoM change. This decline is attributed to increased domestic supply as the 2024/25 harvest season progresses, alleviating short-term supply constraints. However, prices surged by 31.25% YoY due to the lingering effects of adverse weather conditions in the previous year, which had reduced crop yields, combined with heightened global demand and inflation-driven cost increases throughout the supply chain.

3. Actionable Recommendations

Adopt Labor-Saving Practices to Sustain Yields

Banana producers should invest in labor-saving cultivation techniques and tools to offset workforce shortages and maintain export volumes. For example, switching to high-density planting systems, using mulch to suppress weeds, and applying drip irrigation can reduce manual labor needs. Producers in the Dominican Republic, Ecuador, and the Philippines can also deploy mechanized tools for tasks like bunch covering and weed control. These steps help stabilize production and reduce dependence on a volatile labor supply.

Strengthen Buyer Relationships to Retain Market Share

Banana producers should reinforce direct relationships with key importers and retailers in core markets like the US to stay competitive despite tariff pressures. By offering consistent supply schedules, premium quality assurance, and joint promotions, producers in Costa Rica, Ecuador, Colombia, and beyond can strengthen loyalty and reduce the risk of volume cuts. For example, securing long-term contracts with supermarket chains or collaborating on co-branded packaging can help absorb cost increases and maintain shelf space.

Sources: Tridge, Elnacional, Freshfruitportal, Hfbrasil, Hoy, LAFM, Philstar, The Mercury