In W21 in the grape landscape, some of the most relevant trends included:

- Argentina’s grape harvest has reached 1.98 thousand mt this season, and Mendoza remains the country’s top grape-producing region. Meanwhile, the wine industry continues to show growth and diversification.

- Brazilian exporter Santa Felicidade increased its shipment capacity to over 120 containers this season, targeting markets in Europe, the US, and the UK. The company is also preparing to enter the Chinese market with grape exports, pending the finalization of necessary trade agreements.

- India’s Nashik district maintained grape exports at 157 thousand mt for 2024/25 despite unseasonal rains. Europe received 110 thousand mt of India’s grape exports, and farmers in India benefited from higher prices.

- Italy’s Sicily region started the 2025 table grape season strongly, especially in Mazzarrone, which produces high-quality seedless varieties under greenhouse conditions and is gaining global market traction.

1. Weekly News

Argentina

Argentina’s Grape Harvest Hits Four-Year High

According to the National Institute of Viticulture (INV), Argentina’s grape harvest has reached 1.98 million metric tons (mt) this season, the highest in four years. Mendoza continues to maintain its role as the country’s leading grape-producing region. With rising production volumes, an increasing number of active wineries, and a sector that is adapting to evolving market demands, the industry is signaling a more resilient and dynamic production landscape.

Brazil

Brazil Expands Grape Exports Due to Favorable Weather and Global Demand

Favorable weather and a 16-hectare (ha) vineyard expansion in Brazil have enabled grape exporter Santa Felicidade to increase its shipment capacity to over 120 containers this season. Santa Felicidade primarily targets markets in Europe, the United States (US), and the United Kingdom (UK), while sustaining strong local sales in São Paulo and Minas Gerais. Cultivating premium varieties such as Cherry Crush, Autumn Crisp, and Cotton Candy, the company remains competitive despite high sea freight costs, due to varietal innovation and proactive market engagement. Brazil’s strategic export window, positioned between Peru and Chile’s seasons, offers a market advantage. With all the required certifications in place, the company is preparing to access the Chinese market once trade agreements are finalized.

India

Nashik Maintains Grape Export Levels Despite Weather Challenges

India’s Nashik district has maintained grape exports at 157 thousand metric tons (mt) for the 2024/25 season. This matches last year’s volume despite unseasonal rains in October and April that threatened yields. A strong second harvest phase from mid-February to early May helped stabilize supply, enabling exports of 110 thousand mt to Europe and 47 thousand mt to other regions. Farmers also benefited from higher seasonal prices, ranging from USD 0.88 to 1.29 per kilogram (INR 75 to 110 per kg) in Feb-25 to Mar-25, compared to USD 0.64 to 1 per kg (INR 55 to 85 per kg) the previous year. Major grape-growing areas like Niphad, Dindori, and Nashik talukas contributed significantly to the district’s resilience.

Italy

Sicilian Grape Season Begins with Strong Yields and Global Demand

Sicily’s 2025 table grape season is off to a promising start, especially in the Mazzarrone area. Favorable weather and early maturity have led to strong yields of traditional varieties like Victoria and Black Magic, followed by the seedless ARRA30. These grapes are grown under greenhouse protection and optimal Mediterranean conditions and are gaining traction globally for their quality and lower environmental impact. At Macfrut 2025, producers showcased their offerings and highlighted Sicily and Apulia’s competitiveness in supplying high-demand seedless grapes early in the market cycle. Macfrut 2025 is a key platform for Sicily’s grape producers to highlight their high-quality, sustainably grown varieties. The event underscored the region’s role in meeting early market demand with competitive seedless grape varieties, strengthening its position in the global table grape trade.

United States

California Expects Strong Table Grape Season With Favorable Growing Conditions

California grape growers are entering the 2025 table grape season with high expectations. This is supported by excellent winter moisture from rainfall and snowpack, which has sustained healthy vine growth for a third straight year. With strong bunch counts and minimal disease concerns, the industry anticipates a high-quality and abundant crop, assuming favorable conditions persist. The season is projected to mirror 2024’s timeline, with harvests beginning around July 1 and early varieties like Candy Snaps expected to enter the market between July 15 and 20.

2. Weekly Pricing

Weekly Grape Pricing Important Exporters (USD/kg)

Yearly Change in Grape Pricing Important Exporters (W21 2024 to W21 2025)

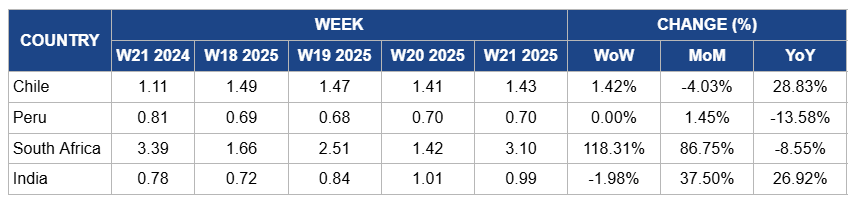

Chile

Chilean grape prices increased by 1.42% week-on-week (WoW) to USD 1.43/kg in W21, with a 28.83% year-on-year (YoY) increase due to improved fruit quality and stronger international demand, particularly from the US and Asian markets. The higher prices also reflect the effects of reduced global supply from competing producers earlier in the season. However, month-on-month (MoM) prices dropped by 4.03% due to the winding down of the 2024/25 harvest season, which led to less uniform fruit sizes and quality, impacting market value.

Peru

In W21, Peru's grape prices remained stable WoW at USD 0.70/kg, with a modest 1.45% MoM increase due to the conclusion of the 2024/25 export season. This stability reflects the market's adjustment to the end of the harvest period, during which supply levels normalized. However, YoY prices dropped by 13.58%, due to a significant increase in production and export volumes. Peru's grape production for the 2024/25 is forecasted to reach 790 thousand mt, a 2% YoY increase, driven by improved climatic conditions in northern coastal regions. Additionally, grape exports are projected to hit a record 620 thousand mt, marking a 17% YoY rise. The increased supply has exerted downward pressure on prices, leading to the observed YoY decline.

South Africa

Grape prices in South Africa surged by 118.31% WoW to USD 3.10/kg in W21, with an 86.75% MoM increase, primarily due to the culmination of the 2024/25 harvest season, which led to reduced domestic availability and heightened demand in local markets. Despite a record-breaking export season with 77.4 million cartons exported, a 5% YoY increase, the conclusion of the harvest resulted in tighter local supplies, thereby driving up prices. However, prices experienced an 8.55% YoY decrease, attributed to the overall increase in production volumes and intensified competition in international markets. Notably, the US imposed a temporary 10% tariff on South African grape imports in Apr-25, with the potential for a 31% tariff after July, which could affect export dynamics and pricing structures.

India

In India, grape prices decreased slightly by 1.98% WoW to USD 0.99/kg. However, prices increased by 37.50% MoM and 26.92% YoY, due to a significant reduction in grape production, particularly in major growing regions like Nashik, where yields declined by approximately 40% owing to unseasonal rainfall and adverse weather conditions. The decreased supply coincided with strong local demand and a shortened export season, leading to heightened competition among buyers and driving prices upward.

3. Actionable Recommendations

Stagger Harvest and Strengthen Cold Chain to Maximize Returns

Grape producers in countries like the US, India, and Chile should stagger harvest schedules and invest in cold chain upgrades to avoid market saturation and maintain quality. By spreading out harvests of early, mid, and late-season varieties, producers can reduce price pressure during peak weeks. For example, California growers can prioritize early Candy Snap harvests while Indian producers delay shipments of Thompson Seedless to align with market gaps. Simultaneously, investing in reliable pre-cooling and refrigerated transport helps preserve fruit quality, allowing exporters to target distant markets without compromising shelf life.

Diversify Export Destinations to Mitigate Climate Risk

Grape producers in India, South Africa, and Peru should expand into non-traditional markets to reduce dependence on a single region and manage weather-related disruptions. For example, Indian growers in Nashik can explore Southeast Asian or Middle Eastern markets beyond the EU, while South African producers can increase shipments to Eastern Europe or West Africa. This strategy spreads logistical risks and supports price stability, especially when adverse weather affects supply timing or volume.

Sources: Tridge, FreshFruitPortal, Freshplaza, Fructidor, Timesofindia, TN