In W21 in the maize landscape, some of the most relevant trends included:

- Global corn output will rise by 3.6% to 1.265 billion mmt in 2025/26, driven by a production increase in the US . This boost will lift global and US-ending stocks, putting downward pressure on international corn prices.

- Bangladesh expects a record maize harvest due to expanded planting, while Brazil’s larger second crop will support increased exports. In contrast, Ukraine’s corn exports dropped by 27.5% YoY despite improved weather and logistics.

- US corn prices rose due to planting delays and strong export demand. Argentina’s prices increased, supported by delayed harvests and tight domestic availability, In contrast, Brazil’s prices declined amid ample supply and weaker feed demand while Ukraine’s prices edged lower as improved weather conditions and stable export activity helped ease supply concerns.

1. Weekly News

Global

Global Production Surge Pressures Prices

Citing the latest United States Department of Agriculture (USDA) supply and demand report, the International Center for Economic Analysis and Agricultural Market Studies (CEEMA) reports that projected growth in global corn production for the 2025/26 marketing year (MY) is driving international cereal prices down. The United States (US) plans to expand its corn planting area by 5.2%, boosting production by 6.4% year-on-year (YoY) to 401.8 million metric tons (mmt). This increase will raise the US ending stocks to 45.7 mmt, up from 36 mmt the previous year. It will also push the average farmgate price down to USD 4.20 per bushel from USD 4.35 in the 2024/25 season. Globally, producers will raise corn output by 3.6% to 1.265 billion metric tons (mt), while global endingl stocks will rise to 277.8 mmt from 251.3 mmt in 2024/25.

Bangladesh

Bangladesh Projects Record 6 MMT Harvest as Acreage Climbs

Bangladesh is on track for a record maize harvest this year, driven by a shift from traditional crops like wheat and rice to maize, especially in the northern regions. According to the Bangladesh Bureau of Statistics (BBS), the country produced a record 4.87 mmt of maize from 0.514 million hectares (ha) in the 2023/24 fiscal year, with contributions from both winter and summer. In 2025, the Department of Agricultural Development (DAE) reports that maize cultivation has expanded to over 0.55 million ha, continuing a decade-long upward trend. The Ministry of Agriculture projects a record production of 6 mmt, which would nearly fulfill national demand, highlighting maize’s rising importance in Bangladesh’s agricultural landscape. In Nilphamari district alone, maize cultivation rose to 33,200 ha from 28 thousand ha in 2024, as more farmers converted wheat and some rice fields to maize for better yields. Similarly, in the Rangpur region, the maize area increased by 10 thousand ha to 127 thousand ha, while wheat cultivation halved to just 14 thousand ha.

Impact of Brazil’s HPAI Outbreak on Corn Demand Amid Growing Global Supply and Complex Trade Dynamics

A Highly Pathogenic Avian Influenza (HPAI) outbreak in Brazil’s commercial poultry sector will reduce short-term corn demand as several countries, including China, impose temporary bans on chicken meat exports. Because the poultry industry consumes large amounts of corn for feed, these export restrictions have lowered demand. However, the impact should remain limited if authorities control bird flu and keep embargoes temporary. Meanwhile, despite drought in some regions, US farmers advanced corn planting. The USDA reported sales of 2.75 mmt of corn from the 2025/26 harvest, but China has not yet made significant purchases. Brazil expects to grow its second corn harvest by 11%, mainly for export, which will boost global supply and likely put downward pressure on corn prices.

Ukraine

Ukraine Faces Significant Decline in 2024/25

As of May 19, Ukraine exported 37.15 mmt of grain and leguminous crops from the 2024/25 crop, reflecting a 21.1% YoY decline compared to MY 2023/24, according to the Ministry of Agrarian Policy and Food of Ukraine. Corn exports sharply declined by 27.5% YoY or 5.45 mmt to 19.81 mmt.

2. Weekly Pricing

Weekly Maize Pricing Important Exporters (USD/kg)

Yearly Change in Maize Pricing Important Exporters (W21 2024 to W21 2025)

United States

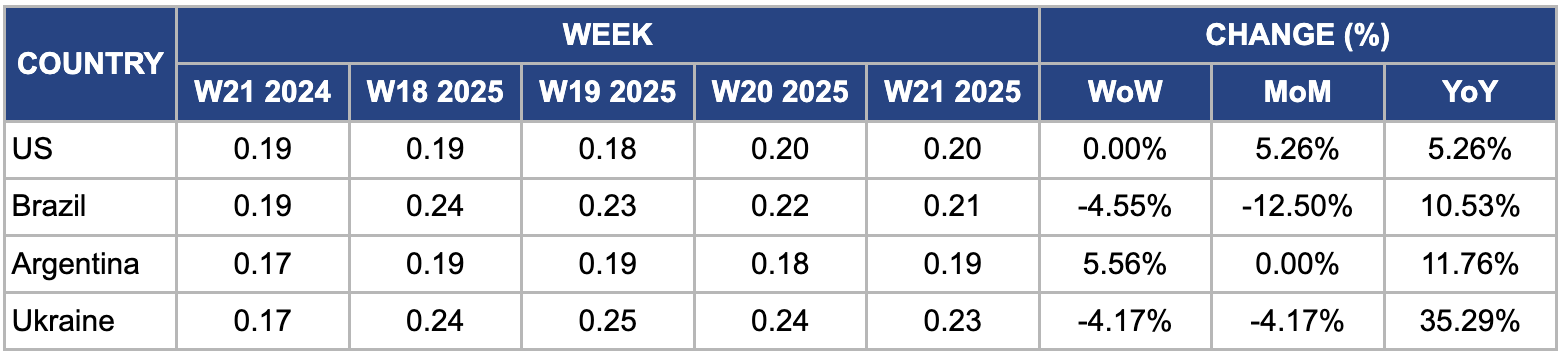

In W21, US corn prices held steady week-on-week (WoW) but climbed 5.26% month-on-month (MoM) and 5.26% YoY to USD 0.20 per kilogram. This upward trend stemmed primarily from planting delays due to excessive rainfall and saturated soils in key Corn Belt states like Iowa, Illinois, and Nebraska, where progress fell well behind the five-year average. These delays sparked concerns over potential yield losses and crop quality issues later in the season. Moreover, strong export demand from major buyers such as China and Mexico further tightened domestic supply. The combined impact of adverse weather conditions, planting lags, and firm export activity has continued to apply upward pressure on US corn prices.

Brazil

In W21, Brazil’s wholesale maize prices fell 4.55% WoW and 12.50% MoM to USD 0.21/kg. The decline was due to favorable weather conditions in key maize-producing states like Mato Grosso and Paraná, which eased previous concerns over yield losses. Improved weather facilitated faster harvesting and boosted the 2024/25 Safrinha crop supply. At the same time, demand weakened from the livestock and ethanol sectors as economic challenges prompted these industries to adjust their consumption. The combined effect of increased supply and slower demand has exerted significant downward pressure on Brazilian maize prices.

Argentina

In W21, Argentine maize prices increased 5.56% WoW to USD 0.19/kg. The price rise was due to tight domestic supply caused by delayed harvesting and reduced availability in local markets. Unfavorable weather earlier in the season, particularly excessive rainfall in key producing provinces such as Buenos Aires, Córdoba, and Santa Fe, slowed harvest progress, limiting short-term maize stocks. As of mid-May-25, only about 25 to 30% of the maize area had been harvested, compared to over 40% during the same period last year. This delay constrained immediate availability and tightened domestic supply. Furthermore, steady export demand from key buyers, including Vietnam and Algeria, helped support prices, even as broader regional markets saw downward pressure due to ample supplies in Brazil.

Ukraine

In W21, Ukrainian wholesale maize prices declined by 4.17% WoW and MoM, falling to USD 0.23/kg from USD 0.24/kg. This price decrease was due to improved weather conditions in key producing regions, which have enhanced crop development and reduced earlier fears of potential yield losses. According to recent agricultural reports, Ukraine’s 2025 maize harvest area will rise by approximately 2% YoY, boosting production forecasts to around 39 mmt. Furthermore, the stabilization of export logistics and increased throughput at Black Sea ports have facilitated higher shipment volumes, improving domestic supply availability. Combined with consistent demand from major export destinations such as the European Union (EU) and Egypt, these factors have exerted downward pressure on prices, leading to the observed market decline.

3. Actionable Recommendations

Optimize Planting and Harvesting Schedules to Mitigate Weather Risks

Farmers in major maize-producing regions like the US (especially Iowa, Illinois, and Nebraska) and Argentina should implement more flexible and adaptive planting and harvesting schedules by integrating advanced weather forecasting tools and real-time soil moisture monitoring technologies. Extension services and agricultural advisors can provide tailored guidance on optimal planting windows and contingency plans for weather extremes such as excessive rainfall or drought conditions. Moreover, adopting precision agriculture techniques such as variable rate irrigation and planting can help optimize input use and reduce vulnerability to unpredictable weather. These measures will help minimize the adverse effects of weather delays that have previously caused planting lags and potential yield losses.

Diversify Export Markets and Strengthen Logistics Infrastructure

Ukraine and Brazil should actively seek to broaden their portfolio of international buyers beyond traditional markets like the EU and China. This diversification could involve identifying emerging markets in Africa, Southeast Asia, and the Middle East through trade missions, marketing campaigns, and bilateral agreements. At the same time, investing in logistics infrastructure, such as upgrading Black Sea port facilities in Ukraine, improving rail and road connections from production zones to export terminals, and modernizing storage capacities, will enhance the efficiency and volume of maize shipments. Diversifying export destinations reduces reliance on a few buyers, lowering the risk of geopolitical tensions or sudden trade restrictions. Improved logistics infrastructure decreases shipment delays and bottlenecks that previously constrained exports, allowing countries to better capitalize on global demand peaks. This expanded and more reliable market access helps stabilize domestic maize prices, increases farmer revenues, and strengthens Brazil and Ukraine’s position in the global maize trade.

Promote Value-Added Maize Products and Alternative Uses

Governments, agricultural cooperatives, and private sector actors should promote the development of maize processing industries to produce higher-value products such as animal feed, ethanol, starch, and packaged food items. This includes facilitating investments in processing facilities and offering technical training for farmers to shift some acreage from lower-value crops (like wheat or rice) to maize varieties suited for processing. For example, Bangladesh’s shift from wheat and rice to maize cultivation demonstrates the potential of this strategy to meet rising domestic demand. Encouraging research and adoption of improved maize varieties for food and industrial uses can also support this transition. Developing a robust value-added maize sector diversifies revenue streams for farmers and processors, reducing vulnerability to raw commodity price volatility, especially when export markets face temporary disruptions (e.g., poultry sector bans in Brazil). Expanding domestic consumption through processed products enhances demand stability and can improve rural livelihoods by creating jobs along the maize value chain. This approach builds a more resilient agricultural economy with sustainable growth potential.

Sources: Tridge, Agrolink, CanalRural, UkrAgroConsult