.jpg)

In W21 in the olive oil landscape, some of the major trends include:

- Global olive oil output will reach 3.38 mmt in 2024/25, a 32% increase YoY, driven by record rebounds in Türkiye, Spain, and Tunisia. Favorable weather conditions boosted yields.

- European exporters face challenges from potential higher US tariffs, pushing efforts to expand into Asia despite cultural barriers limiting demand there.

- Andalusia leads global table olive exports but suffers from US tariffs on black olives, prompting calls for diplomatic action.

- Meanwhile, Pakistan is implementing a National Olive Value Chain Policy to boost production, reduce edible oil imports, and become an export player by 2030 through expanded planting and value chain improvements.

- Prices declined sharply WoW in Spain due to abundant supply and competition, while Italy’s prices rose WoW amid a drought-affected smaller harvest and persistent strong demand. Greece saw price declines WoW following production recovery, whereas Tunisia’s prices edged up due to tighter supply and strong exports.

1. Weekly News

Global

Global Olive Oil Output to Jump 32% in 2024/25 on Strong Recovery in Spain, Türkiye, and Tunisia

Global olive oil production is expected to reach 3.38 million metric tons (mmt) in the 2024/25 crop year. According to the International Olive Council, this marks a 32% year-on-year (YoY) increase from 2023/24 and 13% above the five-year average. This rise is due to strong production rebounds in Spain, Tunisia, and Türkiye, where output will grow by 51%, 55%, and 109%, respectively, with Türkiye set to hit a record-high 450 thousand metric tons (mt). Spain’s improved yield is mainly due to favorable growing conditions, including a wet winter and mild spring that helped restore water supplies.

Europe

European Olive Oil Exporters Face Uphill Battle in Asia Amid Looming US Tariffs

European olive oil exporters actively seek new markets amid the threat of higher United States (US) tariffs that could erode their competitiveness against Türkiye and Tunisia. While efforts are underway to expand exports to Asia, especially India and China, experts caution that the region’s cultural food preferences pose a hurdle to boosting demand. In 2023, the US imported USD 1.5 billion worth of olive oil from Italy, Spain, and Greece, compared to just USD 477 million in combined imports by India, China, Japan, and South Korea. Asian markets offer limited potential, with consumers favoring local oils like peanuts, or soybean oil and viewing olive oil as a niche or luxury product. Even in Japan and South Korea, where European cuisines have some presence, traditional eating habits and market perceptions constrain growth. Although reduced prices might open opportunities in regions like Africa or Australia, their smaller markets and similar cultural barriers limit the ability to compensate for lost US sales.

Spain

Andalusia Leads Global Table Olive Exports Despite US Tariff Challenges

Andalusia reinforced its position as the global leader in table olive exports, generating USD 795.85 million in sales between Jan-24 and Nov-24, according to Andalucía TRADE. Agrosevilla, the world’s largest producer and exporter of table olives, drove this success with its strong commitment to sustainability and innovation. However, the sector faces main challenges, mainly due to the US tariffs on Andalusian black olives, which caused losses of over USD 135.91 million since 2018. In response, the Agriculture Minister and the president of Agrosevilla urged Spanish and European Union (EU) authorities to intensify diplomatic efforts to eliminate these unfair trade barriers.

Pakistan

Pakistan Targets Global Olive Market with New National Value Chain Policy

Pakistan submitted its “National Olive Value Chain Policy” to the federal cabinet, aiming to transform the country into a key global olive market player by leveraging its favorable climate and rising demand for olive oil. Developed by the Ministry of National Food Security and Research, the policy outlines a roadmap through 2030 that builds on past initiatives and emphasizes boosting olive production, enhancing processing and training, engaging the private sector, and strengthening value chain management. It also recommends extending the Olive Development Project for another year (2025/26) with a USD 2.23 million budget to support continued planting, wild olive grafting, and institutional development. With 5.5 million trees already planted, mainly in Balochistan, Punjab, and Khyber Pakhtunkhwa, Pakistan aims to reduce its USD 3.33 billion edible oil import bill and position the olive sector as a strategic export driver under the 13th Five Year Plan (2024-29), including the formation of export-oriented clusters.

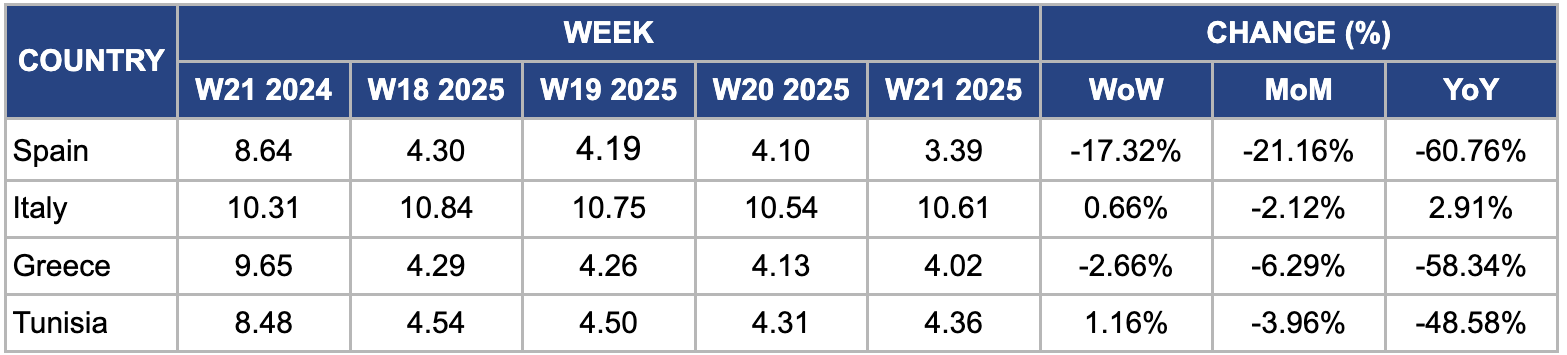

2. Weekly Pricing

Weekly Olive Oil Pricing Important Exporters (USD/kg)

Yearly Change in Olive Oil Pricing Important Exporters (W21 2024 to W21 2025)

Spain

In W21, Spanish extra virgin olive oil prices declined significantly by 17.32% week-on-week (WoW) to USD 3.39 per kilogram (kg). Prices dropped 21.16% month-on-month (MoM) and 60.76% year-on-year (YoY). Following the record-breaking 2024 harvest, Spain’s olive oil production remained high but began to stabilize, leading to abundant supply in the market. Increased competition from other Mediterranean producers like Italy and Greece, who raised their output and offered competitive prices, further pressured Spanish prices. Moreover, global demand softened due to economic uncertainties and inflationary pressures in main markets such as the EU and the US. Logistical challenges and rising transportation costs also disrupted export operations.

Italy

Italy’s wholesale extra virgin olive oil price reached USD 10.61/kg in W21, rising 0.66% WoW. Prices remain supported by a 32% drop in the 2024/25 harvest caused by drought, extreme temperatures, and pest infestations such as the olive fruit fly and Xylella fastidiosa. Strong international demand continues to underpin prices despite recent declines. However, a new 20% US tariff on EU olive oil imports raises uncertainty by increasing export costs and threatening market access. A temporary 90-day tariff pause provides some relief, but ongoing trade tensions may drive prices higher in non-EU markets and increase reliance on intra-EU trade to maintain stable demand.

Greece

Greece’s wholesale extra virgin olive oil price fell to USD 4.02/kg in W21, dropping 2.66% WoW and 6.29% MoM, with a sharp 58.34% decline YoY. This significant annual decrease reflects a strong production recovery following previous shortages that had driven prices to record highs. Production remains stable at around 250 thousand mt for the 2024/25 season, but limited stock levels restricted supply flexibility. As mid-2025 approaches, tightening availability and steady demand may slow the price decline and potentially trigger a rebound. However, the Greek olive oil market remains vulnerable to climatic changes, which could quickly impact future prices and market stability.

Tunisia

In W21, Tunisia’s wholesale extra virgin olive oil price rose slightly by 1.16% WoW to USD 4.36/kg, up from USD 4.31/kg in W20. This modest price increase reflects tightening supply conditions following a lower-than-expected 2025 harvest due to adverse weather impacts, such as drought and irregular rainfall during the flowering and fruit-setting stages. Moreover, strong export demand from key markets in Europe and North America helped support prices. However, ongoing logistical challenges and increased production costs also contributed to maintaining upward price pressure in Tunisia’s olive oil market during this period.

3. Actionable Recommendations

Expand and Adapt Export Markets Beyond the US and Traditional Regions

European olive oil exporters should actively target emerging markets such as Africa, Australia, and the Middle East, with growing interest in healthy oils. To overcome cultural barriers like preferences for local oils in Asia, exporters should develop region-specific marketing campaigns highlighting olive oil’s health benefits, culinary versatility, and premium quality. Collaborations with local chefs, influencers, and retailers can help raise awareness and create demand.

Invest in Supply Chain Improvements and Quality Control

Producers, especially in Italy and Spain, should enhance pest and disease management practices and invest in post-harvest handling, cold storage, and logistics infrastructure to reduce losses and maintain product quality. This will help stabilize supply, support premium pricing, and mitigate disruptions caused by weather or trade uncertainties. Strengthening coordination between producers and exporters can optimize inventory management to respond flexibly to market shifts.

Support Emerging Olive Oil Producers with Integrated Development Policies

Governments and industry bodies in countries like Pakistan should implement comprehensive olive sector development plans that expand planting areas, improve cultivation techniques, and build processing and export capacity. They should offer training programs, subsidize inputs, and provide technical assistance to improve productivity and quality. By establishing export clusters and encouraging private sector involvement, they can accelerate market entry and boost competitiveness on the global stage.

Sources: Tridge, Oleo Revista, Olive Oil Times, UkrAgroConsult