In W21 in the orange landscape, some of the most relevant trends included:

- Brazil is expected to produce 314.6 million boxes of oranges in 2025/26, a 36.2% YoY increase due to favorable weather and a 7.5% rise in productive trees.

- Brazil has gained market access to export sweet oranges to India, strengthening bilateral trade and expanding its agricultural export portfolio.

- The US faces record-high production costs for California navel oranges in 2025, with total costs projected at USD 10.41 thousand/ha due to rising labor and input expenses.

- The US orange growers in California are under pressure as picking, hauling, packing, and marketing costs have significantly increased. Despite stable yields, these rising costs are threatening profitability.

1. Weekly News

Brazil

Brazil’s Orange Production Expected to Rise Sharply in 2025/26

Orange production in Brazil’s main citrus regions, São Paulo, Triângulo Mineiro, and southwest Minas Gerais, is projected to reach 314.6 million 40.8-kilogram (kg) boxes for the 2025/26 season, marking a 36.2% year-on-year (YoY) increase. This surge is driven by a 7.5% expansion in the number of productive trees and favorable climatic conditions. The anticipated output is expected to help rebuild depleted orange juice inventories, which remain below strategic levels and may stay tight until mid-2025. If processing capacity can keep pace with harvests, juice stocks could stabilize by mid-2026. Although grower prices may ease from their Oct-24 peak, they are projected to remain above historical averages.

Brazil Gains Market Access to Export Oranges to India

Brazil has secured market access to export five citrus fruits, including sweet oranges (Citrus sinensis), to India, marking a major milestone for its orange industry. This development is part of a broader trade initiative that has enabled six other Brazilian products, such as avocados, to enter the Indian market since 2023. India imported over USD 3 billion in Brazilian agricultural goods last year, and this new agreement is expected to enhance trade by introducing higher value-added citrus products. Achieved through joint efforts by Brazil’s Ministry of Agriculture and Livestock (MAPA) and the Ministry of Foreign Affairs, the deal is one of 55 international market openings finalized in 2024, contributing to 355 new access agreements since early 2023.

United States

California Navel Orange Production Costs Reach Unprecedented Levels Amid Rising Input Expenses

California’s navel orange production costs are projected to rise to approximately USD 10.41 thousand per hectare (ha) by 2025, continuing a long-term upward trend from USD 3.3 thousand in 2020 and USD 2.7 thousand in 2015. This increase is mainly driven by rising labor costs, including minimum wages that have more than doubled since 2005, and higher fuel, fertilizer, and pesticide expenses. Picking and hauling costs are expected to reach USD 2.9 thousand/ha, a 110% rise over two decades. Packing and marketing costs have also increased 33% since 2005, averaging USD 6.7 thousand/ha as of W21. With growers producing about 700 field cartons per acre and an 80% utilization rate, managing input costs is critical to maintaining profitability amid mounting economic pressures.

Donaldson Orange Under Evaluation as Juice Industry Alternative in the US

The United States Department of Agriculture (USDA) Agricultural Research Service is actively assessing the Donaldson sweet orange as a potential alternative to the Hamlin variety, which has been severely impacted by Huanglongbing (HLB) disease. At the United States (US) Horticultural Research Laboratory in Florida, Donaldson trees continue to exhibit strong health and vigor despite testing positive for HLB. In contrast, Hamlin trees show signs of decline. Although Donaldson has not yet been commercially adopted, it has grown at the Groveland research farm for over three decades and demonstrates promising juice characteristics. Ongoing trials aim to confirm its disease tolerance and suitability for large-scale juice production, potentially offering a more resilient option for the US citrus industry.

2. Weekly Pricing

Weekly Orange Pricing Important Exporters (USD/kg)

Yearly Change in Orange Pricing Important Exporters (W21 2024 to W21 2025)

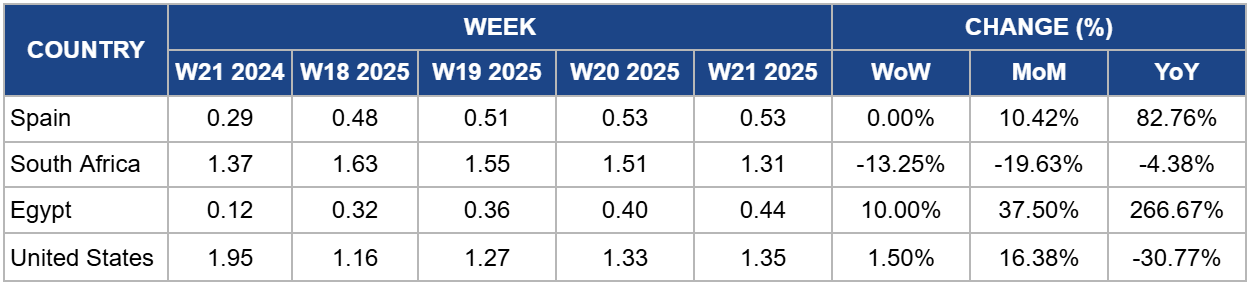

Spain

In W21, orange prices in Spain remained stable week-on-week (WoW) at USD 0.53/kg, reflecting a 10.42% month-on-month (MoM) increase and a significant 82.76% YoY surge. This price rise is mainly attributed to a tight supply situation resulting from continued lower yields in the 2024/25 season due to drought stress and erratic weather conditions. Reduced harvest volumes and smaller fruit sizes have limited market availability, especially for export-quality oranges. In addition, rising input and transport costs, and strong demand from local and European buyers, have supported higher pricing levels.

South Africa

South Africa's orange prices declined by 13.25% WoW to USD 1.31/kg in W21, with a 19.63% MoM and a 4.38% YoY decrease. This downward trend is due to several converging factors. Firstly, adverse weather conditions, including frost and hailstorms in key growing regions like Limpopo and the Western Cape, have impacted fruit quality and reduced export volumes. Secondly, a significant portion of the orange harvest has been diverted to juice processing due to surging global demand and higher prices for orange juice, leading to an oversupply in the fresh fruit market. Additionally, logistical challenges, particularly inefficiencies at South African ports, have disrupted export schedules, causing delays and increased costs. These combined factors have exerted downward pressure on fresh orange prices in the local market.

Egypt

In W21, Egypt's orange prices increased by 10% WoW to USD 0.44/kg, with a 37.50% MoM rise and a significant 266.67% YoY surge. This sharp increase is primarily driven by a 12% drop in national orange production for the 2024/25 season, due to higher temperatures during the fruit set period, which reduced yields. Additionally, there has been a notable 50% rise in the volume of oranges being diverted to processing for juice, further tightening the availability of fresh oranges in the domestic market. Export logistics have also been disrupted due to the ongoing Red Sea crisis, limiting access to Asian markets and contributing to oversupply in others. Compounding this, the devaluation of the Egyptian pound has made exports more attractive but increased local production costs, pushing prices higher across domestic channels. These combined factors have led to constrained supply and heightened demand, resulting in a steep YoY price surge.

United States

In W21, US orange prices increased by 1.50% WoW to USD 1.35/kg, with a 16.38% MoM rise. This uptick is due to reduced domestic production, particularly in Florida, where hurricanes and citrus greening disease have significantly impacted yields. The USDA reports a projected 30% drop in Florida's orange production for the 2024/25 season, reaching levels not seen since before World War II. Additionally, the diversion of oranges to juice processing, driven by strong global demand and higher juice prices, has tightened the supply of fresh oranges, further elevating prices. However, YoY prices have declined by 30.77%, due to a significant drop in consumer demand for orange juice. High retail prices, concerns over juice quality stemming from disease-affected crops, and changing consumer preferences have led to a more than 16% decrease in US retail demand for orange juice. This reduced demand has exerted downward pressure on prices compared to the previous year.

3. Actionable Recommendations

Cut Costs by Shifting to Precision Input Use

Orange producers in California, Spain, South Africa, and Brazil should adopt precision agriculture tools to reduce input costs without compromising yield. For example, growers can use soil moisture sensors and drip irrigation systems to cut water and fuel usage during irrigation. Insect monitoring traps and targeted pesticide applications can lower chemical costs while improving pest control. Spanish and South African producers can integrate nutrient mapping to optimize fertilizer distribution, while Brazilian growers can adopt GPS-guided equipment to reduce labor hours and fuel during spraying and harvesting.

Prioritize Pre-Harvest Agreements with Juice Processors

Orange producers should secure pre-harvest agreements with juice processors to ensure processing slots during peak harvest weeks. With rising production in regions like Brazil, Spain, and the US, early coordination prevents delays and reduces the risk of fruit spoilage. Producers can lock in delivery schedules and volume commitments, which supports smoother operations and help maintain juice quality. For example, Brazilian growers can coordinate staggered deliveries by region, while Spanish and US producers can negotiate flexible processing timelines to match local harvest peaks.

Segment Fruit for Diversified Market Channels

Orange producers should sort fruit early in the supply chain to match quality with the most suitable market, fresh, juice, or local processing, to reduce price pressure. For example, growers in South Africa, Spain, and the US can allocate cosmetically blemished or undersized fruit to juice processors, while reserving premium-grade oranges for high-value fresh export markets. This targeted sorting approach helps manage surplus, improves pack-out rates, and minimizes losses from export delays or weather-damaged fruit.

Sources: Tridge, Brazilian Ministry of Agriculture and Livestock, Cepea, Citrus Industry, Food Business Africa, MAPA, New York Post