In W21 in the sugar landscape, some of the most relevant trends included:

- Brazil's 2024/25 sugar production dropped 5% YoY due to drought but is expected to rise 2.7% in 2025/26 despite lower milling volumes, contributing to global oversupply concerns and sustained price pressure.

- The US and Mexico experienced price declines in W21, with Mexico facing a sharp 34.48% YoY drop due to falling sugarcane payments, weakened harvests, and reduced planting incentives.

- Kazakhstan achieved a record sugar beet harvest in 2024 but processed only half due to aging infrastructure, leading to a 25% YoY drop in sugar output and prompting planned cultivation cuts that may threaten long-term industry viability.

- Nigeria advanced legislative reforms to strengthen its sugar industry and support export development as part of broader national economic goals, with a renewed focus on sustainability and regulatory efficiency.

- Under its Sugarcane Value-Chain Master Plan, South Africa proposed regulatory exemptions to support local sugar procurement, rural employment, and diversification. Aiming to reduce dependence on imports and mitigate the effects of the sugar tax.

1. Weekly News

Global

Global Sugar Prices Decline with Macroeconomic Pressures

Global sugar prices fell by 3.3% year-on-year (YoY) in Mar-25 and another 7.1% YoY in the first half of Apr-25, reaching USD 0.1752 per pound (lb) on April 15. The decline is attributed to macroeconomic instability, a weaker Brazilian real (BRL), and increased sales from Thailand. In Brazil, the Brazilian Sugarcane Industry Association (UNICA) reported that the 2024/25 Center-South harvest showed resilience despite drought impacts, with 622 million metric tons (mmt) milled and 40.2 mmt of sugar produced, both down 5% YoY. The ethanol output also fell by 2% to 26.8 billion liters (L). For 2025/26, forecast revisions lowered milling expectations to 590 mmt due to dry conditions, though sugar output is projected to rise 2.7% to 41.2 mmt. Despite market and climate pressures, the sector remains competitive through strategic adaptation.

Bangladesh

Bangladesh Raises Sugar Prices Ahead of Subsidized Sales Program

The Trading Corporation of Bangladesh (TCB) has raised the price of sugar to USD 0.70 per kilogram (BDT 85/kg), an increase of USD 0.12/kg (BDT 15/kg), ahead of its nationwide truck-based subsidized commodity sales. Running until June 3, the initiative targets low-income consumers in major cities and divisions, allowing TCB smart card holders to purchase limited quantities of essential items, including sugar. The price hike, announced just before Eid-ul-Azha, has drawn public attention despite the program's intent to provide economic relief through subsidized food distribution.

Kazakhstan

Kazakhstan's Record 2024 Sugar Beet Harvest Highlights Processing Challenges and Risks to Industry Growth

Kazakhstan's sugar industry experienced a record sugar beet harvest in 2024, with cultivation increasing 34% to 25,000 hectares (ha), resulting in nearly 1.3 mmt of beets. However, processing capacity remains insufficient, with only about half of the crop processed due to aging infrastructure and limited factory upgrades. Sugar production fell 25% YoY to 164,400 metric tons (mt), despite a surge in exports. The Ministry of Agriculture of Kazakhstan plans to reduce beet cultivation by 25% in 2025, prompting concerns from farmers over financial risks and potential bankruptcies. Without significant investment in processing facilities, Kazakhstan risks missing its strategic goals for sugar self-sufficiency and industry growth.

Nigeria

Nigeria Pursues Sugar Sector Reforms to Boost Exports

Nigeria's Federal Government has reaffirmed its commitment to developing sugar exports as part of broader efforts to strengthen the national economy. At a public hearing on proposed amendments to the National Sugar Development Council Act, the Minister of State for Industry emphasized sugar's role in achieving the administration's USD 1 trillion economic vision. The amendments aim to revitalize the sugar sector following the underperformance of the Nigerian Sugar Master Plan (NSMP), a government-backed initiative aimed at revitalizing the Nigerian sugar industry approved in 2012. Lawmakers and stakeholders expressed support for regulatory reforms to enhance the council's effectiveness, with a focus on improving sustainability, industry regulation, and export potential.

South Africa

South Africa Proposes Sugar Sector Exemption to Strengthen Local Supply and Industry Sustainability

South Africa's Department of Trade, Industry, and Competition (DTIC) has proposed draft regulations for a block exemption in the sugar sector, allowing producers, retailers, and manufacturers to coordinate on local sugar procurement and pricing. This measure aims to reduce import dependence, protect rural jobs, and enhance industry sustainability under the Sugarcane Value-Chain Master Plan 2030. Supported by the South African Cane Growers Association, the exemption would facilitate fairer pricing and promote collaboration, including diversification into biofuels. The proposal addresses challenges from cheap imports and the sugar tax, but its implementation date remains pending as it undergoes public consultation.

2. Weekly Pricing

Weekly Sugar Pricing Important Producers (USD/kg)

Yearly Change in Sugar Pricing Important Producers (W21 2024 to W21 2025)

.png)

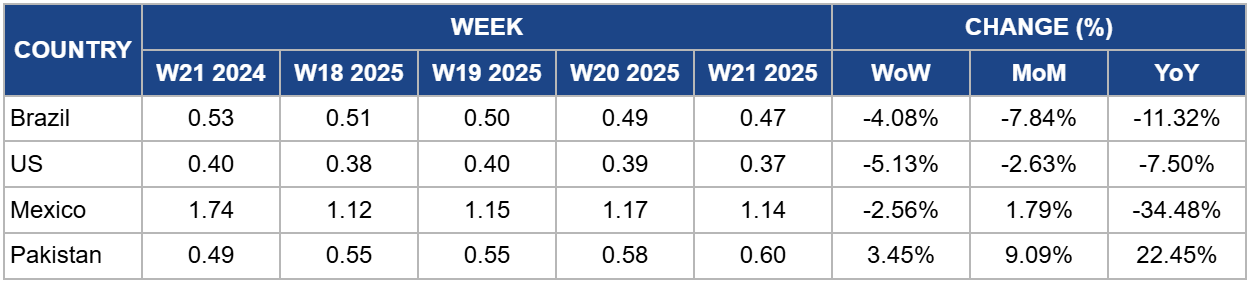

Brazil

Brazil's sugar prices declined to USD 0.47/kg in W21, down 4.08% week-on-week (Wow) and a decrease of 11.32% YoY from USD 0.53/kg. The price drop reflects bearish market sentiment driven by expectations of rising global supply. The United Department of Agriculture's (USDA) Foreign Agricultural Service (FAS) projects Brazil's output to grow by 2.3% YoY to 44.7 mmt, while the National Supply Company (CONAB) anticipates a 4.0% increase to 45.875 mmt. These upward revisions in production have heightened expectations of market oversupply, weighing on current prices.

United States

In W21, the United States (US) sugar prices declined to USD 0.37/kg, reflecting a 5.13% WoW and 7.50% YoY decrease. This price movement aligns with broader macroeconomic pressures, notably the weakening of the US dollar (USD) amid trade tensions with China and investor caution regarding the US economic outlook. Reduced demand for US assets has contributed to softer commodity prices, including sugar. On the supply side, favorable spring planting conditions in key sugar beet-producing states such as Idaho, Oregon, and Washington have enabled early sowing and bolstered yield prospects for the 2025 crop, despite a modest 2% YoY decrease in planted acreage. This improved production outlook is likely to cap near-term price gains.

Mexico

In W21, Mexico's sugar prices declined by 2.56% WoW to USD 1.14/kg, reflecting a sharp 34.48% YoY decrease from USD 1.74/kg in 2024. This price drop confirms a broader collapse in domestic sugarcane pricing, significantly affecting producer revenues. For the 2024/25 harvest, the reference sugar price was set at USD 840.69/mt (MXN 16,300/mt), down from USD 1036.68/mt (MXN 20,100/mt) the previous year, a 19% YoY reduction. As a result, the sugarcane payment fell to approximately USD 59.31/mt (MXN 1,150/mt) in regions like El Mante, causing a financial shortfall estimated at over USD 20.63 million (MXN 400 million). This decline followed several years of elevated prices, which had encouraged expansion in cane cultivation. The current downturn, compounded by weaker harvests, raises concerns over the economic viability of cane farming, particularly in Tamaulipas. If low prices persist, they could discourage future planting, potentially tightening supply and creating upward price pressure in subsequent seasons. However, ample availability and reduced demand are expected to cap prices in the near term.

Pakistan

Pakistan's sugar prices rose to USD 0.60/kg in W21, reflecting a 3.45% increase in WoW and a 22.45% YoY surge from USD 0.49/kg in 2024. Domestically, average retail prices climbed to USD 0.62/kg (PKR 175.19/kg), with Peshawar reporting peaks of USD 0.65/kg (PKR 185/kg), a weekly increase of USD 0.018/kg (PKR 5/kg) and a YoY gain of over USD 0.11/kg (PKR 31/kg). This weekly price escalation reflects persistent cost-push inflation in essential commodities, placing increased financial pressure on consumers already burdened by high living costs. The steep rise raises concerns over supply chain inefficiencies, potential speculative hoarding, or inadequate regulatory oversight.

3. Actionable Recommendations

Hedge Against Depressed Prices Through Strategic Storage and Flexible Contracts

With global sugar prices declining sharply, importers and traders should adopt flexible procurement strategies that leverage current lows. Where storage capacity and shelf-life allow, buyers should consider stockpiling at reduced rates, particularly from Brazil and Thailand, the primary contributors to the current oversupply. Flexible contracts with volume-adjustment clauses will allow for agility amid potential rebound risks from tightening in Mexico or reduced Brazilian output in 2025/26.

Target Demand-Driven Growth via Subsidized and Strategic Sales Initiatives

Amid volatile global prices, rising domestic prices in countries like Pakistan and Bangladesh indicate room for targeted market penetration. Exporters from oversupplied regions (e.g., Brazil, Thailand) should collaborate with governments and retailers to expand subsidized sugar programs in developing markets. Smart card distribution systems, like those in Bangladesh, offer a structured channel for bulk sales at moderate margins while supporting food security goals and maintaining throughput during periods of weak international demand.

Sources: Tridge, Agrolink, The Times of Central Asia, ZAWYA, ChiniMandi, Expreso