W21 2025: Tomato Weekly Update

In W21 in the tomato landscape, some of the most relevant trends included:

- Due to unsustainable containment costs, Australian tomato growers call for the reclassification of ToBRFV from eradication to management.

- US-Mexico tomato trade tensions escalate as new tariffs impact prices and exports.

- Unseasonal weather caused production drops and price surges in Morocco and Spain, while heavy rains and early monsoons in India disrupted supply chains and pushed up vegetable prices, including tomatoes.

- Tomato prices showed wide fluctuations in W21, with sharp rises in Morocco and Spain. However, prices steeply declined in France due to oversupply and declined slightly in Türkiye due to easing demand and increasing supply following peak consumption.

1. Weekly News

Australia

Australian Greenhouse Tomato Growers Demand Shift from Eradication to Management of ToBRFV

Australian greenhouse tomato growers urgently call for a change in the national biosecurity response to the Tomato Brown Rugose Fruit Virus (ToBRFV). They want the virus reclassified from “under eradication” to “present-under management.” The industry argues that Plant Health Australia’s current eradication efforts, led by its incident response group, no longer align with global best practices and have become unsustainable. These efforts cause disproportionate economic losses, pushing tomato prices higher for consumers and delaying effective containment. ToBRFV first appeared in Australian greenhouses in Aug-24, detected on four properties in South Australia. On Jan-25, the virus was confirmed in Victoria. While ToBRFV poses no risk to food safety or public health, containment efforts have prioritized eradication through mandatory destruction of infected plants and surrounding crops, followed by extended testing and quarantine.

India

Heavy Rains in Kolhapur Disrupt Tomato Supply and Triggers Price Surge

Heavy rainfall in Kolhapur and surrounding rural areas has disrupted the vegetable supply chain, leading to significant price hikes in local markets. Tomato prices have doubled to USD 0.70 per kilogram (kg) in W21 due to poor ripening conditions and premature harvesting, resulting in low-quality produce. Surging consumer demand, panic buying, and increased supply of immature produce have further inflated costs. Additionally, persistent rain and traffic congestion on key routes have delayed transportation from Kolhapur and Sangli to cities like Pune and Mumbai, with delays of up to three hours reported.

Early Monsoon Arrival Triggers Vegetable Price Surge in Mumbai

The India Meteorological Department (IMD) reported the early arrival of the southwest monsoon in Kerala on May 24, eight days ahead of schedule. While the reasons remain unclear, scientists cite various factors with no consensus, as El Niño and La Niña offer little predictive value. The early rains have led to a spike in vegetable prices across the Mumbai Metropolitan Region. Tomato retail prices stood at USD 0.59/kg in W21, with other vegetables also seeing notable price increases.

2. Weekly Pricing

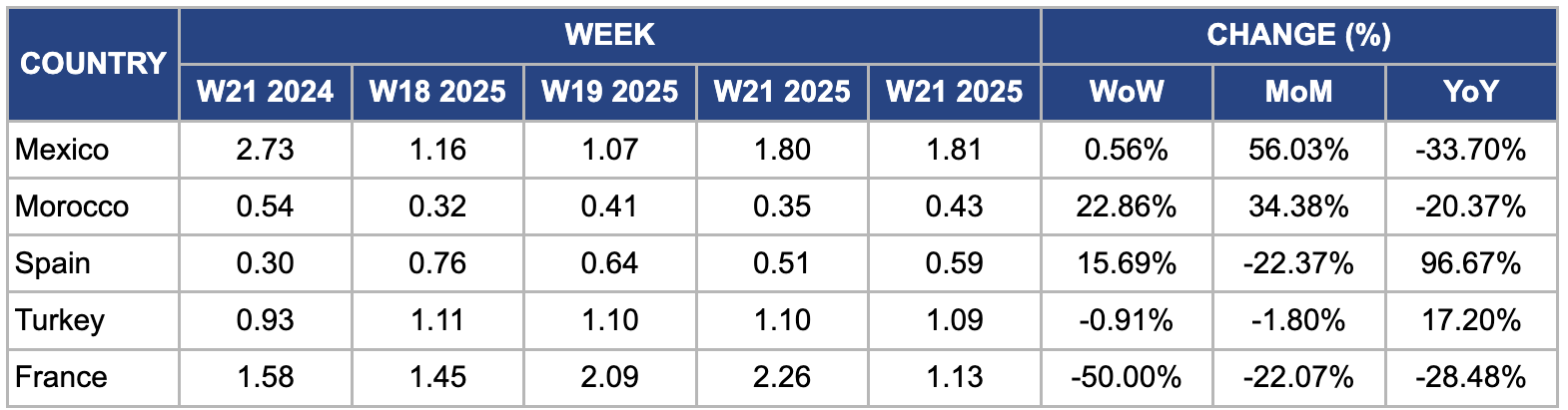

Weekly Tomato Pricing Important Exporters (USD/kg)

Yearly Change in Tomato Pricing Important Exporters (W21 2024 to W21 2025)

Mexico

In W21, Mexican tomato prices rose 0.56% week-on-week (WoW) to USD 1.81/kg and surged 56.03% month-on-month (MoM). However, prices remained 33.70% below last year’s USD 2.73/kg. This price volatility mainly results from ongoing trade uncertainties, especially the United States (US) decision to impose a 17.09% anti-dumping duty on Mexican tomatoes starting July 14, 2025. The tariff dispute has already reduced Mexican agricultural exports by 3.2% overall and caused a 7.8% annual drop in tomato export revenues to USD 859 million in early 2025. Since over half of Mexico’s tomato production exports are primarily to the US, Mexican tomatoes represent nearly 70% of the US fresh tomato supply. These trade barriers threaten market stability and regional economies, particularly in Baja California, which depends heavily on exports.

Morocco

In W21, Morocco’s tomato prices surged 22.86% WoW to USD 0.43/kg from USD 0.35/kg in W20. Prices also rose 34.38% MoM. This sharp price increase was mainly due to reduced supply caused by unseasonal weather conditions, including cold snaps and heavy rains, which affected approximately 15 to 20% of tomato crops in key growing areas such as Souss-Massa and Gharb. These weather disruptions delayed harvests and lowered overall yields, contributing to tighter market availability. According to the Ministry of Agriculture, Morocco’s tomato production for Q1-25 was down about 10% year-on-year (YoY), reaching approximately 320 thousand metric tons (mt) compared to 355 thousand mt in the same period in 2024. Meanwhile, strong domestic consumption and growing export demand, especially from European markets, further tightened supplies. The reduced output and steady demand resulted in upward price pressure, pushing wholesale tomato prices to their highest levels since late 2024.

Spain

In W21, Spain's tomato prices surged 15.69% WoW to USD 0.59/kg, driven primarily by planting delays caused by wet spring conditions. The World Processing Tomato Council (WPTC) has reported significant setbacks in planting schedules, especially in Spain, which may disrupt the total harvest timeline. Spain’s tomato production will decline by 22.5% YoY, falling from 3.1 million metric tons (mmt) in 2024 to an estimated 2.4 mmt in 2025. This production drop is mainly due to adverse weather events, including cold spells and heavy rains in key growing regions such as Andalusia and Extremadura, which impacted yields and delayed planting activities. In addition to these weather challenges, Spain faces increasing competition from lower-cost producers like Morocco and Türkiye, which is eroding its market share. Despite these difficulties, tomato prices in Spain rose substantially by 96.67% YoY, from USD 0.30/kg to USD 0.59/kg, reflecting tight supply conditions and weather-related disruptions pushing prices higher than the previous year.

Türkiye

In W21, Türkiye's tomato prices slightly declined by 0.91% WoW and 1.80% MoM to USD 1.09/kg. This mild price dip was mainly due to an easing of demand after the peak domestic consumption period and the gradual supply increase as the early harvest season progressed. Furthermore, favorable weather conditions in key producing regions such as Antalya and Mersin supported steady crop development and availability, contributing to a more balanced market. Despite the slight decrease, prices remained relatively high compared to W21 2024, reflecting ongoing challenges such as higher input costs and logistical constraints affecting supply chain efficiency.

France

In W21, France’s tomato prices dropped sharply by 50% WoW to USD 1.13/kg, falling 22.07% MoM and 28.48% YoY. Favorable spring weather and advancements in cultivation techniques accelerated crop maturity, producing an early and abundant harvest that flooded the market. Southern European producers like Spain and Italy increased their tomato exports, intensifying competition by offering lower prices due to higher yields and lower production costs. Domestic demand weakened after the peak consumption season, especially in the food service sector recovering from pandemic disruptions, which reduced buying volumes. Moreover, growers expanded greenhouse tomato production, providing year-round availability and consistent quality, further boosting supply. Improvements in cold chain logistics and retail distribution also made fresh tomatoes more accessible and affordable, amplifying the supply glut.

3. Actionable Recommendations

Enhance Supply Chain Resilience in Indian Tomato-Producing Regions Affected by Weather Disruptions

Given the heavy rainfall and transportation delays in Kolhapur and surrounding areas, Indian agricultural authorities and local stakeholders should prioritize building more resilient supply chains to minimize disruptions during adverse weather. One practical measure would be upgrading rural road infrastructure and improving drainage systems to prevent flooding and reduce transit times. For example, establishing decentralized collection and storage hubs closer to production zones could lower the need for long-distance transport during peak monsoon delays. Moreover, promoting weather-tolerant tomato varieties and encouraging staggered planting schedules can help spread harvests over time, easing pressure on the supply chain. These measures would stabilize market supplies, help control prices, and improve product quality despite challenging weather conditions.

Support Mexican Exporters in Navigating US Tariff Challenges Through Diversification and Value-Added Products

With the US Commerce Department re-imposing a tariff on Mexican tomatoes, Mexican producers and exporters should seek to diversify their export markets beyond the US and focus on developing value-added tomato products to buffer against trade disruptions. For instance, exporters can explore expanding into Asian, European, or Latin American markets where demand for fresh and processed tomatoes is growing, mitigating dependence on the US market. Furthermore, investing in processing facilities to produce tomato paste, sauces, and canned products can add value, create new revenue streams, and reduce vulnerability to fresh tomato tariff fluctuations. By broadening market reach and product portfolios, Mexican tomato growers will enhance resilience, protect export revenues, and maintain employment in key growing regions like Baja California.

Reclassify ToBRFV Management Strategy in Australia to Align with Global Best Practices

Australian greenhouse tomato growers should collaborate closely with Plant Health Australia and policymakers to advocate for changing the classification of ToBRFV from “under eradication” to “present-under management.” This shift would enable a more sustainable and economically viable approach by focusing on containment and mitigation rather than costly eradication efforts that have proven unsustainable. For example, the industry can push for integrated management practices, including rigorous hygiene protocols, routine monitoring, and localized quarantine measures instead of whole-crop destruction. This transition would reduce unnecessary losses, stabilize production, and avoid steep price hikes burdening consumers. Investing in grower education and rapid virus detection tools can improve early intervention and reduce spread, creating a long-term, balanced biosecurity response.

Sources: Tridge, Investigate Midwest, Fresh Plaza, Horti Daily, Times Of India, Outlook Business